- India shows strong recovery during 90-day tariff pause

- Pakistan struggles with no new arrivals and a weak PKR

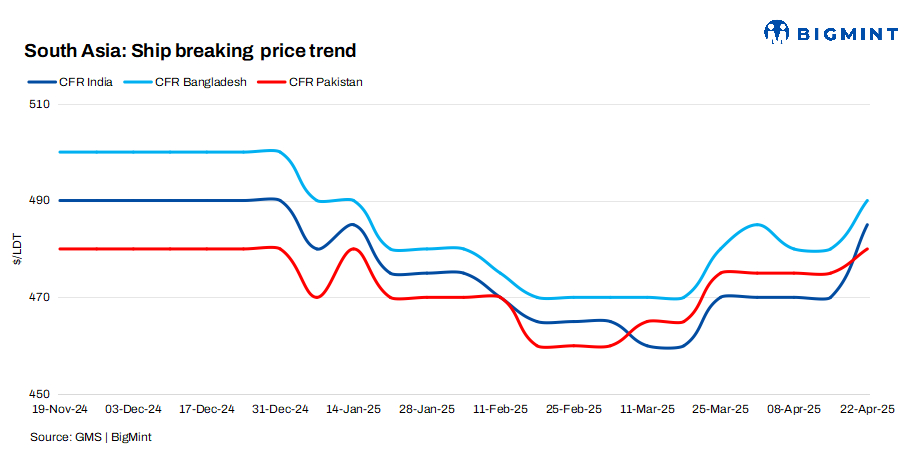

South Asia’s ship-breaking markets remained under pressure this week, as India rebounded strongly but Bangladesh faced delays in HKC approvals, and Pakistan slipped due to weak fundamentals and currency depreciation.

Alang reclaims momentum with strong vessel arrivals

The domestic market has regained momentum after the global 90-day tariff pause, with improved sentiment and rising demand. The INR strengthened against the USD, though local steel plate prices dipped by $5/t.

Alang bounced back from last week’s uncertainty, reclaiming second place in subcontinental rankings with the highest vessel arrivals and idle tonnage. Backed by strong reserves and growing global trade, Indian recyclers remain financially sound.

However, competition from Bangladesh is rising as it upgrades yards to HKC standards. Still, Alang holds an edge in specialised vessels like SS, non-ferrous, and cruise ships, where local demand remains high, maintaining India’s position as a leading destination for ship recycling.

Alang Port received 29,395 light displacement tonnage (LDT) last week, up from 1,178 LDT in the previous week.

Gadani recyclers brace for tough quarter ahead

Pakistan’s ship recycling market has slipped to the bottom of the rankings, with no new arrivals and only two older deliveries reaching Gadani. Steel plate prices stabilised at $624/t, while the PKR weakened against the US dollar, and stronger buying from India and Bangladesh pushed Pakistan further behind.

Rising Chinese steel prices and the threat of cheaper imports may pressure local prices. Ongoing currency volatility and global uncertainty continue to keep recyclers cautious.

Looking ahead, Gadani recyclers face a challenging period with the FY 2025-26 budget due in June, HKC implementation in July, and the monsoon season approaching. The ability to secure tonnage during the 90-day tariff pause remains uncertain, leaving the market in a precarious position for the coming quarter.

According to a market participant, “Despite ongoing activity, there was no sign of improvement in market sentiment; instead, selling pressure persisted.”

Current offers are as follows:

Tanker: heard at $465-470/t.

Containerised: reported at $480-485/t.

Last week, Gadani Port received 13,533 LDT, stagnant compared to the previous week.

HKC extension delays strain Chattogram yards

Bangladesh’s ship recycling market is facing delays as NOC approvals are held up. Several vessels remain stranded, raising costs and putting pressure on Chattogram recyclers, even as the BSBA seeks an HKC upgrade extension.

Post-Eid activity remains slow, with stagnant prices at $523/t and continued Taka volatility. Despite challenges, Bangladesh holds the top position this week, though uncertainty lingers over pricing and demand.

However, strong remittances have helped reduce national loans, keeping the economy stable. The 90-day tariff pause has offered temporary relief, but low vessel availability fuels competition.

Last week, Chattogram Port received 7,484 LDT, up from 2,933 LDT in the previous week.

Leave a Reply