The South Asian scrap markets remained subdued today, with sluggish demand and minimal activity seen in India, Pakistan, and Bangladesh.

Indian buyers were cautious, opting for cheaper domestic scrap as steel demand remained weak. In Pakistan, slow trading continued post-monsoon, with mills reporting low rebar sales and production cuts.

Bangladesh’s market faced a bid-offer disparity, with little buying interest despite stable domestic scrap prices. Meanwhile, in Turkiye, the scrap market held steady as recyclers and mills grappled with tight profit margins.

Participants at the International Rebar Producers and Exporters Association (IREPAS) conference apprehend flat near-term pricing, with sellers firm on offers despite challenges in steel markets across geographies.

Overview

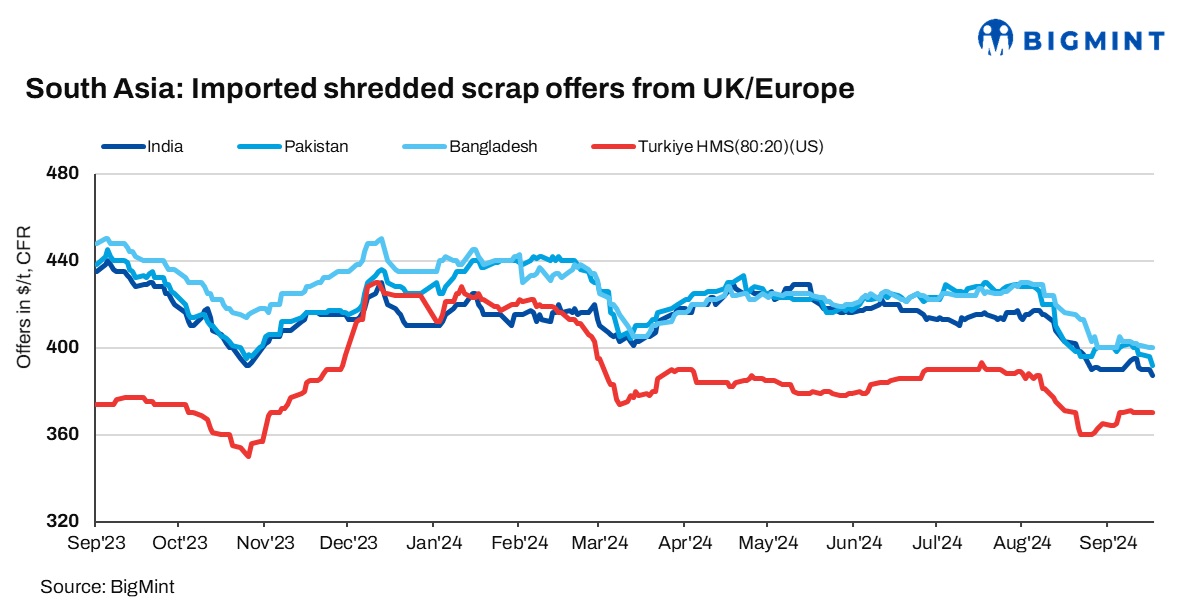

Low spirits prevail in India: In India, demand for imported scrap remained subdued as buyers exercised caution, preferring more cost-effective domestic alternatives. With the steel market sluggish, there was no urgency to purchase imported scrap. Indicative offers for shredded scrap from the US and the UK/Europe hovered at $385-390/tonne (t) CFR Nhava Sheva, while HMS (80:20) from the UK/Europe and West Africa was priced at $365-370/t CFR.

A buyer from southern India shared, “The domestic market is quiet, and demand is extremely weak. Even though there is a slight shortage of scrap locally, prices are not rising because steel demand continues to be poor.”

Other market participants echoed these concerns, stating, “Sentiments are negative, with many diverting their funds to the stock market. It is an unusual scenario – if the stock market crashes, the Indian economy could face an even greater risk than China today. There is little hope for improvement in the iron and steel sector for at least the next three months unless something miraculous happens. Globally, the outlook remains grim.”

Pakistani market fails to pick up post-monsoon: Pakistan’s imported scrap market remained sluggish today, with low demand and minimal trading activity. Steel mills reported weak rebar sales, and the market showed little signs of recovery post-monsoon. Production cuts have persisted due to poor finished product sales, with inventories remaining moderate as most transactions are on credit.

UK-origin shredded scrap held steady at $390-395/t CFR Qasim, while UAE-origin shredded scrap was slightly higher at $405/t CFR.

In the local market, activity was quieter due to holidays and festivals. Prices of domestic scrap were stable at PKR 145,000-150,000/t and of billets at PKR 215,000-220,000/t. Rebar prices were range-bound at PKR 240,000-250,000/t.

Bangladesh sees sluggish demand: Bangladesh’s imported scrap market remained slow today, with a noticeable bid-offer disparity. Offers for UAE-origin shredded scrap stood at $385/t, with counterbids around $370/t CFR Chattogram.

Australian- and New Zealand-origin shredded scrap offers were higher at $398/t CFR.

In the domestic market, prices held steady. Local HMS scrap was priced at BDT 50,500-51,000/t, while ship-breaking scrap was slightly higher at BDT 51,500/t. Local rebar prices remained stable at BDT 83,000/t ex-Dhaka and BDT 88,000-89,000/t ex-Chittagong.

Turkiye holds firm amid tightening profit margins: The Turkish imported scrap market saw no change, with HMS (80:20) offers from the US remaining stable at $370/t CFR. Both recyclers and mills reported slim profit margins at these levels, with sellers targeting $373/t CFR or higher due to elevated HMS collection costs, especially in the Benelux region, where prices touched EUR 295-300/t delivered.

Despite these costs, Turkish mills found higher offers unworkable due to tight rebar margins, with exports assessed at $578/t FOB. Domestic rebar prices were quoted at $595-600/t exw, which contributed to a stand-off between buyers and sellers.

Market participants at the IREPAS conference in Paris expect prices to remain flat in the near term, although some anticipate that mills will need to restock for October shipments soon. There was talk of an EU-origin deal involving 32,000 t of bushelling at $410/t CFR, but this remained unconfirmed.

Price assessments

India: UK-origin shredded scrap indicatives edged down by $3/t d-o-d to $387/t CFR Nhava Sheva.

Pakistan: UK-origin shredded indicatives edged down by $4/t d-o-d to $392/t CFR Qasim.

Bangladesh: UK-origin shredded prices were reported stable d-o-d at $400/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk prices remained stable d-o-d at $370/t CFR Turkiye.

Leave a Reply