- Indian market steady, Pakistan slow amid Eid holidays

- Bangladeshi buyers cautious, Turkish prices stable

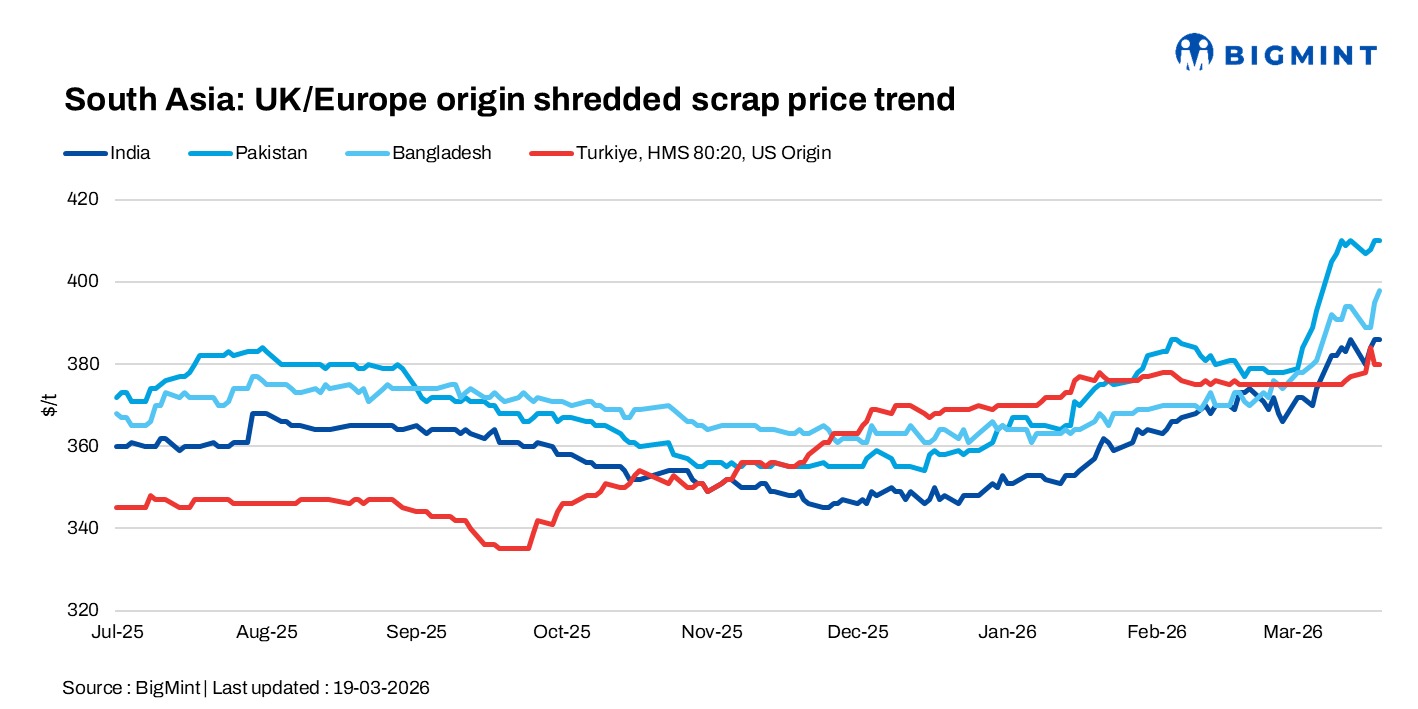

South Asia imported scrap markets remained mixed on 19 March, with the Indian market remaining steady amid supply constraints, Pakistan subdued due to Eid holidays, Bangladesh cautious on freight uncertainty, and Turkiye stable amid rising freights and tightening supply conditions.

India: Imported scrap market sentiment in India remained steady d-o-d, with limited cargo availability and persistent gas supply issues impacting domestic scrap generation and Alang shipbreaking activity. Offers were heard around $390/t for UK-origin shredded, $375/t for HMS 80:20 (1% impurities), $365/t for HMS 80:20 (3% impurities), and US-origin turnings at $365/t, while Africa-origin HMS was indicated at $360-365/t.

Market sentiment was influenced by ongoing Strait of Hormuz tensions, with India increasing Russian oil imports amid supply disruptions. Participants noted that if the situation persists for another 10-15 days, domestic prices could rise above INR 40,000/t ($429/t), while a resolution may ease prices toward INR 33,000/t ($354/t) which impact the market.

Pakistan: Scrap market activity in Pakistan remained slow due to Eid al-Fitr holidays, with trading expected to normalise about a week after reopening. Despite earlier strong buying amid Middle East disruptions, activity has stalled with no fresh deals and limited offers. While UK-origin shredded was last heard near $410/t CFR Qasim, with sentiment weak and trading currently stuck.

Bangladesh: Imported scrap sentiment in Bangladesh remained cautious, with mills keeping quotations open amid freight uncertainty. Firm rates from Australia, Hong Kong, and Singapore pressured buyers, while finished steel demand covered only basic margins. Hong Kong-origin PNS was heard at $405-410/t CFR Chattogram, with HMS (80:20) at $375-380/t.

Turkiye: Deep-sea imported scrap prices in Turkiye remained largely stable, with mills resisting above $370-374/t CFR despite rising freight and energy costs. Sellers targeted higher levels, with US-origin offers at $385-390/t CFR and EU-origin at $378-380/t CFR, though no major deals were reported. Market activity remained limited during the Eid period, with only isolated deals heard done at around $370s.

However, sentiment remains firm as rising freight makes current levels unsustainable for sellers. Disruptions in billet trade from China and Malaysia have reduced alternatives, while export rebar offers increased to $570-575/t. Buying activity is expected to resume post-Eid, supporting prices.

Leave a Reply