- South Asia’s scrap demand weak amid rains, slow steel market

- Turkish mills pause purchases; EU-origin offers remain firm

South Asia’s imported scrap markets kicked off July on a muted note, with buying activity across India, Pakistan, and Bangladesh weighed down by seasonal monsoon disruptions, weak steel demand, and a cautious approach from mills.

Indian buyers remained largely inactive amid cheaper domestic alternatives, while Pakistan’s market slowed further due to Muharram observances and limited downstream offtake. In Bangladesh, mills deferred purchases to later months, avoiding high-priced prompt shipments.

Meanwhile, Turkiye’s scrap market held steady, as mills paused fresh bookings, with firm EU offers supported by currency strength and stable collection costs.

Overall, sentiment across the region remained subdued, with limited near-term recovery triggers.

Market overview

India: India’s imported scrap market remained muted as weak steel demand, monsoon-related disruptions, and availability of lower-cost domestic alternatives curbed buying interest.

Containerised shredded offers were pegged at $360-365/t CFR Nhava Sheva, but bids lagged at $355-360/t, limiting trade. HMS 80:20 offers ranged between $330-345/t CFR across various origins.

Traders noted limited inquiries and a disconnect between offers and buyer expectations, keeping sentiment sluggish.

Pakistan: Pakistan’s imported scrap market remained quiet, as Muharram holidays and ongoing monsoon rains disrupted logistics and construction, limiting mill operations to 35-40% of their capacity. Buyers stayed largely on the sidelines amid weak downstream demand. UK/EU-origin shredded was heard traded at $372-375/t CFR Qasim,

Sentiment stayed subdued, with little appetite for fresh bookings amid slow steel offtake and weather-related constraints.

Bangladesh: Bangladesh’s imported scrap market extended its subdued trend in early July, with buying activity restrained by seasonal monsoon effects, a post-Eid production slowdown, and weak construction demand. Mills steered clear of prompt shipments, instead eyeing August-September arrivals.

Australian shredded offers were heard at $370-375/t CFR Chattogram, while HMS 80:20 was heard at $350-355/t CFR and HMS 1 at $360/t CFR.

Turkiye: The Turkish deep-sea imported scrap market remained largely steady today, as mills paused fresh bookings amid limited rebar demand and availability of competitively priced billets. Offers for HMS 80:20 were at $345/t CFR, unchanged d-o-d, with muted trade activity.

Eurozone suppliers held firm, buoyed by a stronger euro and elevated collection costs, keeping offers for EU-origin scrap around break-even levels. Market participants cited a recent Marmara mill booking at $338/t CFR for HMS and $360/t CFR for bonus.

Chinese billet offers were heard in the range of $455-465/t CFR, keeping scrap buyers cautious, although any rise in billet prices could lend upside potential to scrap values.

Price assessments

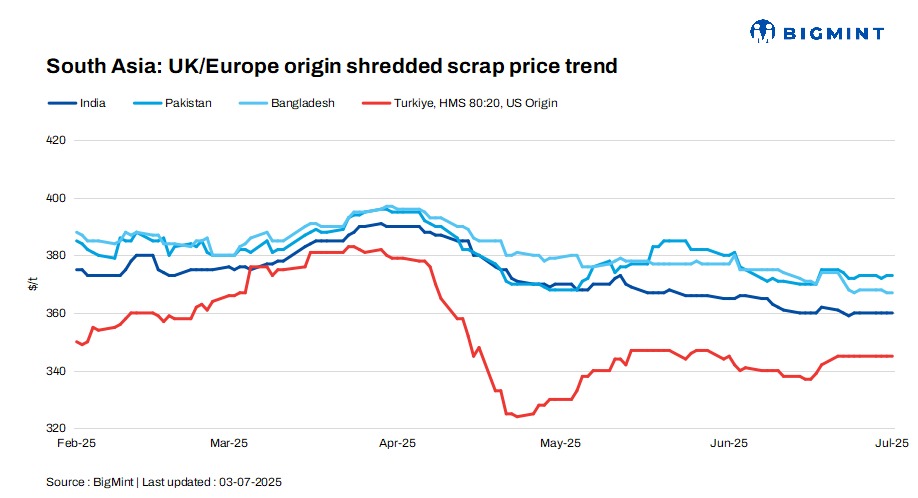

India: UK-origin shredded indicatives were assessed at $360/t CFR Nhava Sheva, unchanged d-o-d.

Pakistan: UK-origin shredded indicatives stood at $373/t CFR Qasim, stable d-o-d.

Bangladesh: UK-origin shredded prices were assessed stable d-o-d at $367/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $345/t CFR Turkiye, unchanged d-o-d.

Leave a Reply