The South Asian imported scrap market showed mixed trends across India, Pakistan, and Bangladesh.

In India, mills were reluctant to import scrap due to the availability of cheaper domestic material and uncertainty in price trends. Pakistan’s scrap consumption, meanwhile, was dampened by slow domestic steel sales, which have exacerbated because of the off-season and diminishing profit margins.

In Bangladesh, demand remained sluggish due to seasonal factors and ongoing banking challenges stemming from recent regulatory changes. However, Turkiye’s scrap market remained stable, with steady purchases despite challenges in the billet market, setting the stage for further late-September shipments.

Overview

India: In India, the demand for imported scrap stayed muted as cheaper domestic scrap remained readily available. Additionally, uncertainty around price trends kept buyers cautious. Despite subdued buyer inquiries, offers have slightly risen, driven by a recent uptick in Turkish scrap offers.

Market participants noted, “Indian scrap bookings stayed low, with mills delaying purchases due to falling steel prices, weak demand, and growing competition from Chinese steel imports.”

A trader based in northern India said, “Local scrap buyers are paying INR 32,500/tonne (t) delivered. If we exclude freight and other charges totalling around INR 2,500/t, the buyer’s cost is around INR 30,000/t, which is roughly $360/t. There are no import offers at that price, making local material more affordable.”

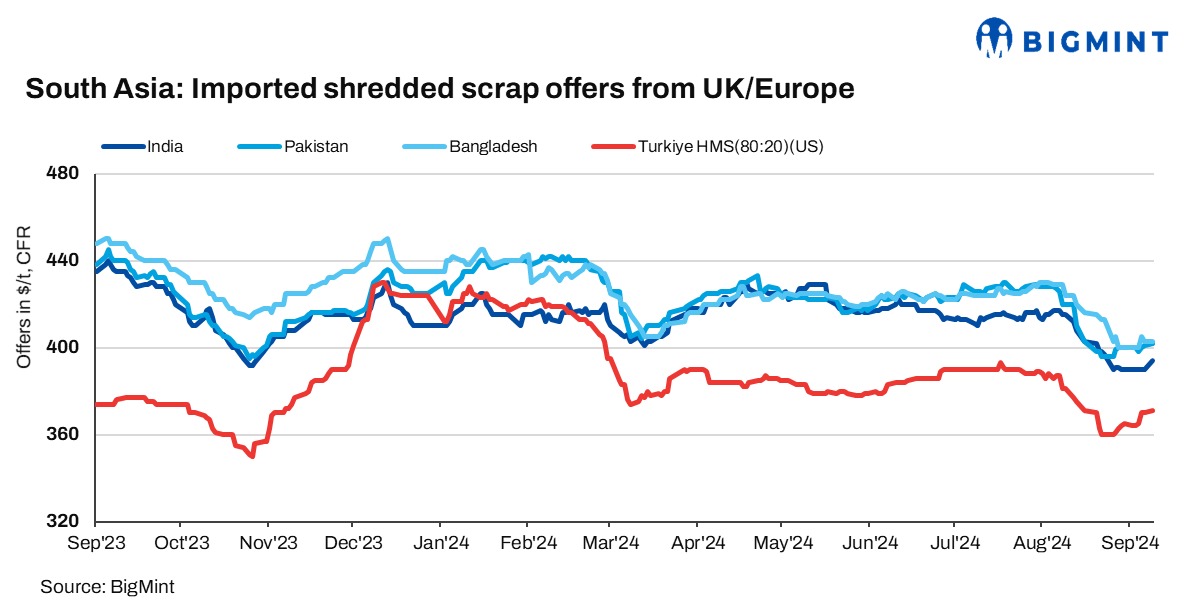

Indicative offers for shredded scrap from the US and the UK/Europe were assessed at $390-395/t CFR Nhava Sheva, while HMS (80:20) offers were at $365-370/t CFR.

Pakistan: Pakistani buyers displayed moderate interest in imported scrap, with sluggish domestic steel sales dampening scrap consumption. The slow steel market was attributed to the off-season, marked by heavy rains and squeezed profit margins. Indicative offers for shredded scrap from the UK/Europe were assessed at $400-405/t CFR Qasim.

Bangladesh: Imported scrap demand in Bangladesh remained sluggish due to seasonal factors and ongoing banking challenges. According to market sources, buyers are experiencing delays in opening letters of credit (LCs) following recent changes in banking regulations after the formation of the new government.

Indicative offers for shredded scrap from the UK/Europe were at $400-405/t CFR Chattogram, while HMS (80:20) was being offered at $390-395/t CFR.

Turkiye: The Turkish imported scrap market exhibited steady activity in early September, with multiple mills securing deep-sea cargoes from both the US and Baltic Sea regions. Turkish steelmakers continued to purchase HMS 1&2 (80:20) and shredded scrap despite challenges in the billet market, which has seen declining prices. The stable demand for scrap was supported by steady long steel prices, as mills strategically reduced production to maintain firm offers amid limited capacity.

Market participants expect further bookings for late-September shipments as mills look to replenish their stockpiles. The outlook remains cautiously optimistic, with the stable scrap market enabling Turkish steelmakers to maintain a consistent flow of raw materials, despite wider market fluctuations in billet prices.

Price assessments

India: UK-origin shredded scrap indicatives were up by $4/t from the last closing day (Friday) to $394/t CFR Nhava Sheva.

Pakistan: UK-origin shredded indicatives inched up by $1/t to $402/t CFR Qasim compared to the last close on Friday.

Bangladesh: UK-origin shredded prices remained unchanged at $403/t CFR Chattogram compared to last Friday.

Turkiye: US-origin HMS (80:20) bulk prices rose by $1/t to $371/t CFR Turkiye from the last close on Friday.

Leave a Reply