The South Asian scrap market experienced significant fluctuations influenced by regional economic and political factors. In India, buyers have remained distant from the seaborne market due to bid-offer disparities, domestic scrap market volatility, and a slowdown in the steel market. The newly announced budget for financial year 2024-2025 (FY24-25) maintained a nil import duty on ferrous scrap, supporting the country’s carbon-neutral goals.

Meanwhile, Pakistan’s scrap demand has been subdued owing to slow rebar sales, though market recovery is anticipated following an IMF approval that might address letters of credit (LC)-related issues. In Bangladesh, imported scrap inquiries have dwindled amid violent civil unrest and a deepening economic crisis.

Turkish deepsea scrap prices have remained stable, with a reported stalemate among mills and sellers due to lack of fundamental market changes. The market anticipates further price stability, with Turkish mills opting for more cost-effective billet imports from the Far East and CIS regions.

Overview

India: Indian buyers continued to stay away from the seaborne market due to bid-offer disparities, volatility in the domestic scrap market, and a slowdown in the domestic steel market. Today marked the announcement of the budget for FY24-25, in which the import duties on ferrous scrap remained nil, aligning with the country’s goal to achieve a carbon-neutral footprint.

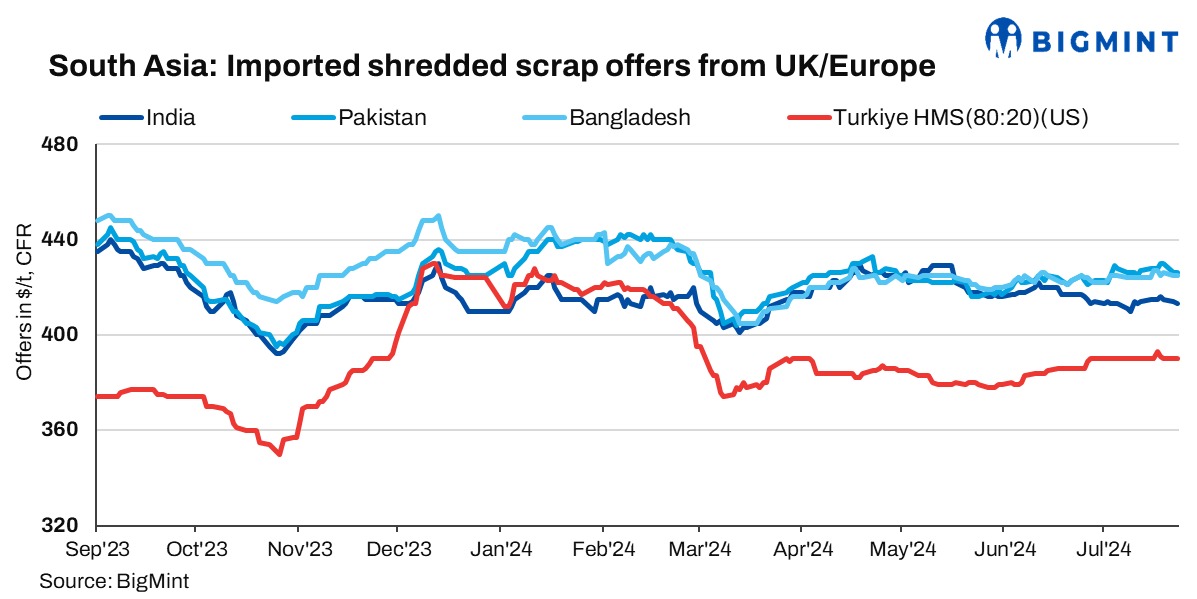

Indicative offers for shredded scrap from the US and UK/Europe were assessed at $410-415/t CFR Nhava Sheva. Some suppliers quoted prices above $420/t, but there were no takers at these levels. HMS (80:20) offers from West Africa and the UK/Europe were assessed at $385-390/t CFR.

Pakistan: In Pakistan, demand for imported scrap has been subdued, primarily due to sluggish rebar sales. Indicative offers for shredded scrap are currently reported at $425-430/t CFR Qasim from the UK/Europe, $420-425/t CFR from the US, and $435/t CFR from the UAE, with buyers adopting a cautious approach to procurement.

As per market participants, the market may see improvement following the recent IMF approval, which could alleviate LC-related issues and potentially lead to a recovery in the near term.

In the domestic market, scrap prices were assessed at PKR 150,000-160,000/t, rebars were at PKR 255,000-260,000/t and billets at PKR 215,000-220,000/t.

Bangladesh: Imported ferrous scrap inquiries remained minimal in Bangladesh due to violent civil unrest and a worsening economic crisis. Indicative offers for shredded scrap from the UK/Europe were reported at $420-425/t CFR, while HMS (80:20) was offered at $405-408/t CFR.

Turkiye: Turkish deepsea imported ferrous scrap prices remained largely stable at 390/t CFR as mills and sell-side sources reported a stalemate due to minimal fundamental changes. Indicative tradable values for US/Baltic-origin premium HMS (80:20) were at $389-390/t CFR. Shortsea scrap prices also stayed stable, with Romanian-origin HMS (80:20) assessed at $370-373/t CFR. Market participants expected continued price stability in the near term. Meanwhile, Turkish mills showed a preference for importing billets from the Far East and CIS regions, as these were more cost-effective compared to current scrap prices, allowing for more competitive rebar production.

Price assessments

India: UK-origin shredded scrap indicatives were assessed at $413/t CFR Nhava Sheva, down by $1/t d-o-d.

Pakistan: UK-origin shredded indicatives were assessed unchanged d-o-d at $426/t CFR Qasim.

Bangladesh: UK-origin shredded prices were assessed stable at $425/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk prices were assessed unchanged at $390/t CFR Turkiye.

Leave a Reply