South Asia’s ship-breaking market saw a busier week with strong performance from the sub-continent markets encouraging ship owners and cash buyers to begin testing potential prices with firm candidates. Indeed, among several deals concluded, a Singapore-origin capesize bulker was also sold.

Now that the Chinese New Year holidays have ended, the anticipated rebound in freight markets has yet to materialise. Talks on the much-needed IMF loans are still ongoing in Pakistan and Bangladesh in order to restore some essential liquidity and USD required to establish new letters of credit (L/Cs) so that domestic recyclers can resume importing vessels or steel.

Turkey, too, saw prices remaining stable with strengthening steel prices and a currency that has reached a new peak resulting in an extra $10/t firming this week.

India concludes deal

Most industry players’ attention has recently been drawn to India, as they continue to secure all of the admittedly limited number of recycling units available so far this year, while Bangladesh and Pakistan are still hampered due to L/C limitations.

As India remained the most-likely destination for ship recycling, the Chinese-controlled SAMC INTEGRITY (24,181 LDT) was committed in the past week for a reasonable $518/LDT for ‘as is’ Singapore delivery and with bunkers included.

On the domestic front, the Indian Rupee is still trading in the low-to-mid INR 82.66 range as of the first half on Feb 7 compared against the previous week, which was around INR 82.30 against the USD.

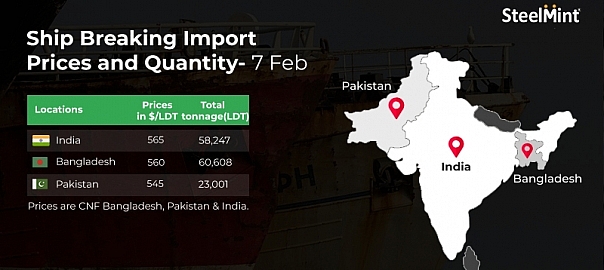

The total tonnage at Alang Port last week was 58,247 LDT.

Bangladesh finding ways to sustain

Although, the Bangladeshi recyclers want to acquire new units, a lack of L/C financing is stifling local efforts.

A capesize bulker was committed on the basis of “as is” Singapore delivery and bears all of the hallmarks of a Bangladeshi resale. However, because of persistent funding constraints, any large vessel is unlikely to arrive at the time being.

As a consequence, a number of container vessels are working directly for HKC recycling into India, ruling Bangladesh out of that tonnage as well.

In the previous week two vessels arrived at the Chattogram port to be beached: Jasmine 201 (9,928 LDT), a bulk carrier and Rose (1,959 LDT), a chemical tanker.

On the domestic fundamentals front, the Bangladeshi Taka further weakened from BDT 106.50 in the previous week to BDT 106.82 against the USD during the first half of the trading session.

The total tonnage reported last week at Chattogram Port was 60,608 LDT.

Pakistan’s persistent funding issues

Pakistan is currently the least competitive in the subcontinent, with the lowest numbers and the most uncertain destination for L/C funding.

As a result, many recent deals have failed only to be offered for sale elsewhere at better numbers. Cash buyers or owners are not even checking with the Gadani market, given the current state of affairs.

A vessel named Witty (23,001 LDT), a bulk carrier that arrived in the previous week was beached. The Pakistani currency fell further below to PKR 276.17 during the trading session on Feb 7 from PKR 275.12 in the previous week against the USD.

The total tonnage at Gadani Port last week was 23,001 LDT.

Prices in $/LDT

Source: SteelMint Research

Leave a Reply