- Bangladesh: Monsoon rains continued to dampen scrap demand.

- Turkiye: High grade- scrap shortage clouded price direction.

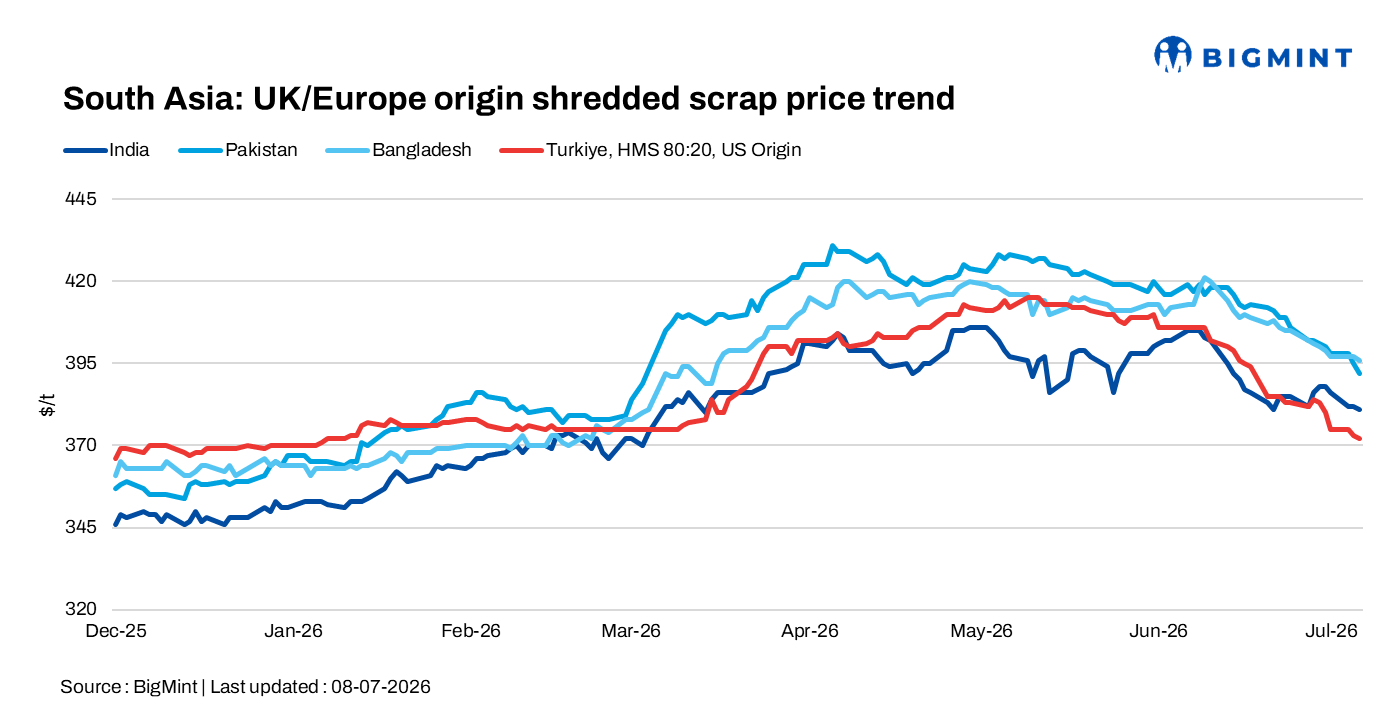

South Asia: Imported ferrous scrap markets remained subdued on 8 July as weak steel demand, monsoon disruptions and cautious mill procurement limited buying across India, Pakistan and Bangladesh. Meanwhile, Turkiye’s deep-sea scrap market stayed under pressure amid mixed sentiment and limited trading activity.

India:Imported ferrous scrap trading remained quiet as weak steel demand and unfavourable import economics continued to keep mills on hand-to-mouth procurement. Africa-origin LMS and HMS 80:20 were offered at $290/t and $330/t C&F Mundra (CAD), respectively, while UK-origin shredded scrap was heard at $380-385/t CFR. No firm bids, offers or trades for containerised shredded scrap were reported, reflecting persistently weak import viability and cautious buying sentiment.

Pakistan: Imported shredded scrap buying remained subdued, with mills continuing need-based procurement amid weak steel demand. A UK-origin shredded scrap deal was heard at $391/t CFR Qasim, while fresh offers were reported at $390-395/t CFR. Buying sentiment remained cautious despite slightly lower offer levels.

Bangladesh: Imported ferrous scrap buying remained subdued as heavy monsoon rains and weak steel demand continued to weigh on sentiment. Buyers indicated HMS 80:20 bids at $355-356/t CFR and shredded bids at $385-390/t CFR, against offers of $370/t CFR for HMS and $395-400/t CFR for shredded scrap. UK-origin shredded scrap was also heard at $398/t CFR.

Domestic steel trading remained slow, with rebar offers at BDT 90,000-92,000/t ex-Chattogram. Meanwhile, Brazil-origin HMS 80:20 was offered at $345/t CFR and HMS 90:10 at $350-355/t CFR, although buying interest remained limited.

Turkiye: Deep-sea imported ferrous scrap market remained under pressure on 7 July, although sentiment turned mixed as trading activity slowed and few suppliers were active. Market participants remained divided over the near-term direction, with limited premium-origin transactions and a widening price gap between premium and non-premium cargoes making price discovery increasingly difficult.

Most mills continued to resist higher offers due to weak finished steel demand, with some expecting further downside, while others believed the market had approached a floor after recent corrections. Tradable values for US-origin HMS 80:20 were heard at $370-375/t CFR, with buying interest remaining cautious.

Leave a Reply