- India demand weak; imports unworkable, activity remains slow

- Pakistan, Bangladesh firm supply; buying cautious, trade limited

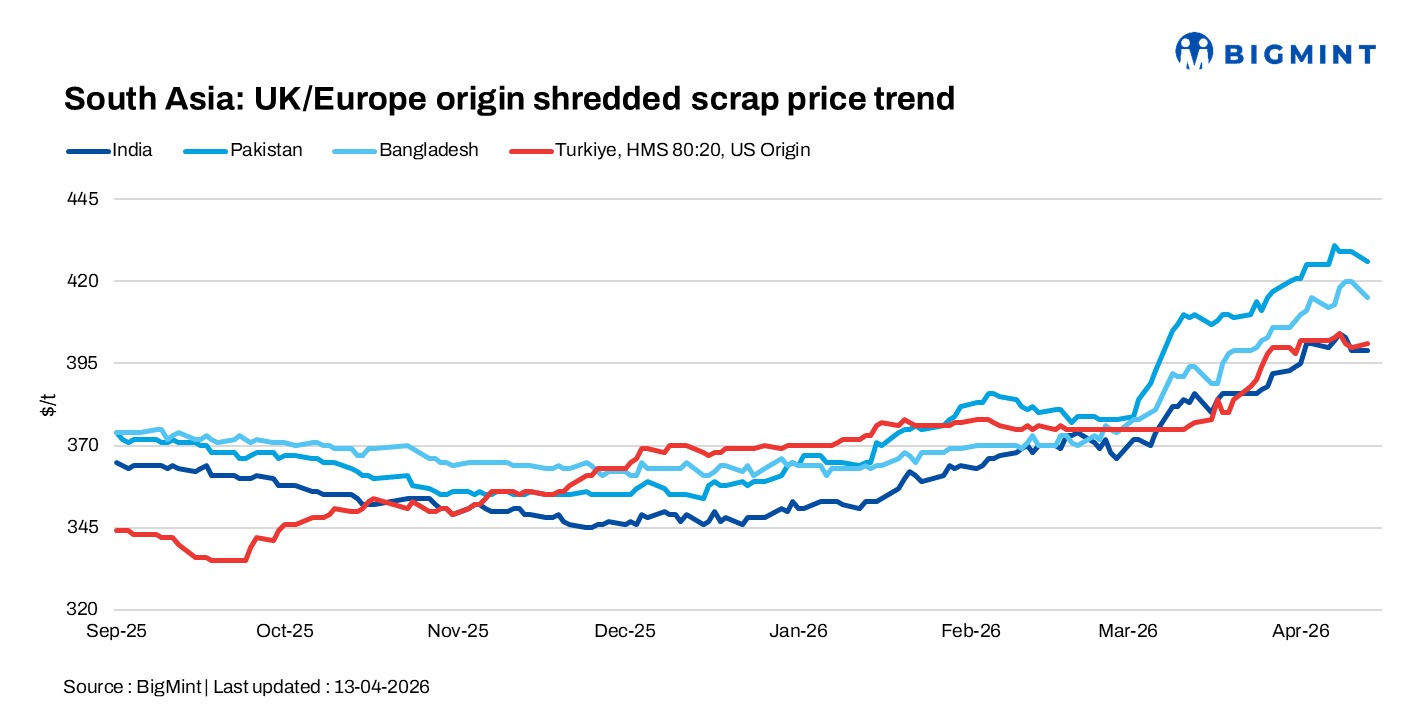

South Asia scrap markets remained slow as of 13 April, with weak demand in India, firm yet cautious sentiment in Pakistan and Bangladesh, and stable Turkiye, as tight supply supported prices but subdued buying limited activity.

India: Imported scrap market remained weak with limited buying interest, as slow finished steel demand continued to weigh on mills’ procurement. HMS 80:20 bookings were reported at $388/t CFR Chennai (Africa origin), while offers from Congo were heard lower at $360/t CFR Nhava Sheva, indicating wide variation by origin. Broader offer levels stood around $380-386/t for HMS 80:20 and $405-410/t for shredded, with bids trailing by $5-10/t as buyers are quoting lower at $375-378/t for HMS and around $390/t for shredded.

Market sentiment stayed cautious as mills resisted higher import prices due to poor margins and preferred domestic scrap. Although raw material prices remained relatively firm, buying activity was limited with very few active participants. Deals such as South Africa-origin HMS at $385/t CFR Mundra and Malaysia LMS offers at $355/t CFR Chennai indicate selective buying.

Pakistan: In Pakistan, the market remained firm but cautious. Imported scrap deals reported for UK-origin bobbin (wire rod bundles) scrap at $445/t CFR Qasim and shredded at $427/t CFR. Offers for UK/Europe-origin shredded continued at elevated levels amid tight supply. Buyers briefly showed interest around $420/t following ceasefire developments, but sellers held firm at $428-430/t, supported by earlier bookings and healthy order books. Prices remained volatile on a daily basis, with fresh offers towards the end of the day heard around $430/t CFR.

Bangladesh: Imported scrap prices into Bangladesh remained largely stable, with HMS 80:20 at $390/t CFR and shredded at $410-415/t. Despite steady pricing, market activity was limited, reflecting cautious sentiment among participants.

The market remained restrained as buyers and sellers stayed apart by around $10/t, with negotiations impacted by lack of price transparency and trust. Although there is willingness to trade, uncertainty over true workable levels continues to delay fresh deal closures. A couple of low-priced containerised scrap deals reported from the UK and Hong Kong appear to be floating or rerouted cargo deals, and may not reflect actual market levels. Current freight rates–having risen to $1,600-1,850 per container for vessels sailing after mid-April–for which such pricing is not viable for broader market assessment.

Turkiye: Deep-sea imported scrap prices remained largely stable in 13 April, with quieter market conditions and reduced participation from US sellers. Limited cargo availability, along with rising collection costs in Europe and a stronger euro, continued to support elevated price levels. However, prices inched up slightly d-o-d as market participants expecting some buying interest to return for May shipments.

Leave a Reply