- Pakistan firm on tight shredded supply

- Turkiye stable; winter and Ramadan weigh

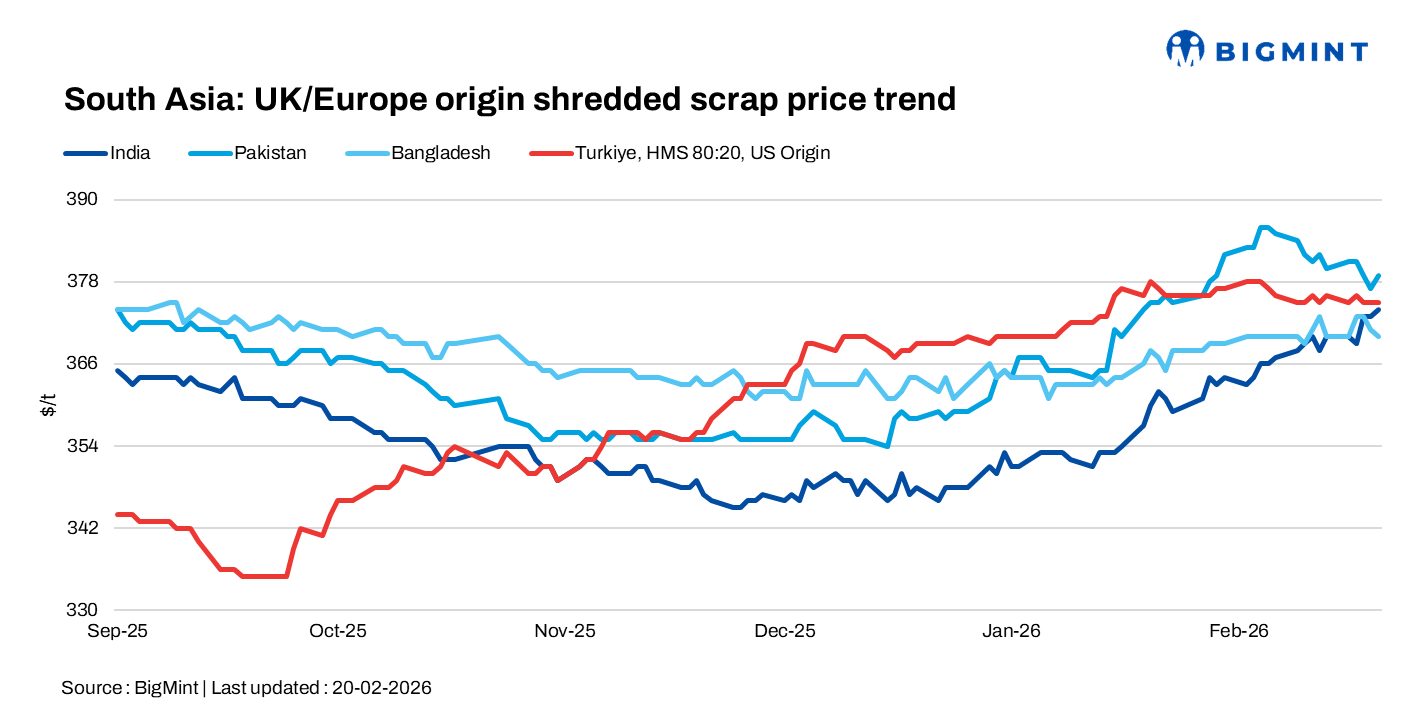

South Asia’s imported scrap markets remained mixed on 20 February, with India cautious amid price resistance, Bangladesh firmer on post-election demand expectations, Pakistan supported by limited supply and selective deals, and Turkiye largely stable as seasonal factors and weak margins kept buying restrained.

India: India’s imported scrap market showed mixed sentiment, with suppliers quoting HMS 80:20 at $352-355/t CFR, though buyers were largely unwilling to conclude deals at those levels. Buying interest at Nhava Sheva and Mundra was heard slightly firmer but still below $350/t, while Chennai remained weaker, with bids $5-8/t lower. West African HMS into Chennai was indicated around $345/t, reflecting continued price resistance.

Offer levels across origins varied, with Brazil grab-loading cargoes around $345/t, UK HMS 80:20 at $345-347/t, Latin American hand-loaded HMS at $360-362/t, and LMS bundles and turnings at $325-330/t. Higher grades were indicated at $370-375/t for PNS and $380-385/t for Bluesteel. Despite a wide range of offers, buying remained selective and price-sensitive.

Bangladesh: Imported ferrous scrap sentiment in Bangladesh improved following the election week, Offer levels remained firm, with Australia-origin HMS 80:20 heard at $360/t and above, HMS 1 at $370/t, and shredded at $380-382/t CFR, though buyer bids at $372-375/t continued to reflect cautious and price-sensitive procurement.

Pakistan: Imported shredded scrap prices in Pakistan remained firm, with offers largely in the $380-382/t range, including UK shredded at $382/t. Supply constraints were evident, with UAE-origin shredded last heard at $395/t. However, selective deals were concluded, including 2,000 t of UAE fabrication scrap at $375/t CFR Pakistan yesterday and 250 t (11 boxes) of UAE HMS 80:20 at $365/t CFR Pakistan earlier in the week, reflecting active but price-sensitive buying.

Turkiye: Deep-sea imported scrap prices remained largely flat d-o-d on 20 February, although market activity picked up toward the end of the week after a relatively quiet first half of the month. The late-week flurry of deals suggests mills re-entered the market selectively, but overall sentiment remains cautious.

Seasonal factors continue to keep the market balanced. Harsh winter conditions in northern Europe are limiting scrap flows, while Ramadan-related slowdown in Turkiye is curbing mill activity. At the same time, a higher number of active sellers is capping upside.

Leave a Reply