- Indian buyers resist higher scrap prices

- Pakistani buyers face rising freight rates

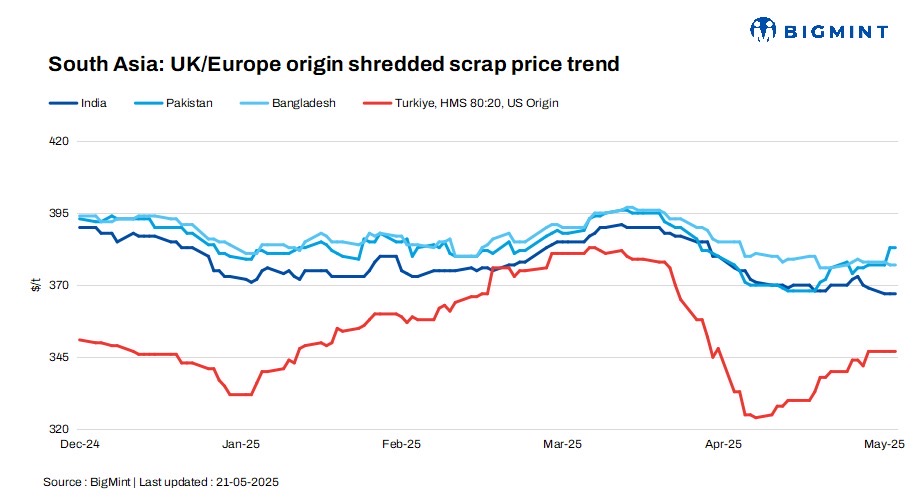

The South Asian imported scrap markets saw subdued activity and cautious sentiments due to weak steel demand and challenging conditions. Shredded scrap offers from the UK and Europe remained steady across India, Pakistan, and Bangladesh.

Indian buyers showed reluctance to accept higher scrap prices, favouring alternatives like sponge iron and pellets. Pakistan struggled with rising freight costs and soft domestic demand, while Bangladesh faced financial constraints and seasonal slowdowns.

Meanwhile, Turkiye’s market remained stable but quiet, with mills holding back amid weak rebar sales.

Market overview

India: India’s imported scrap market remained quiet as buyers resisted higher offer levels amid tepid steel demand and ample availability of alternatives like sponge iron and pellets. UK/Europe containerised shredded scrap was offered at $370-375/t CFR Nhava Sheva, but buyers held back at $360-365/t, resulting in limited trades. HMS 80:20 offers stood at $345-355/t, yet mills showed interest only at lower levels. With the monsoon season nearing and domestic steel margins under pressure, market sentiment stayed cautious and sideways, with traders not expecting a price rise in the immediate term.

Pakistan: Pakistan’s imported scrap market remained under pressure due to rising freight costs and subdued domestic demand. Shredded scrap offers from the UK/Europe are quoted at $380-388/t CFR Port Qasim, but mills are bidding lower at $380-383/t, leading to limited transactions. Shipping lines have imposed surcharges of $300-800/container, effective from mid-May, further inflating import costs. Domestically, scrap prices are stable at PKR 138,000-140,000/ ($496-504/t), while rebar was being offered at PKR 230,000-242,000/t ($827-871/t). Mills are cautious, awaiting clearer signals from global freight and steel markets before increasing bids.

Bangladesh: Bangladesh’s imported scrap market remained under pressure amid weak steel demand, financial constraints, and seasonal slowdown from the monsoon and upcoming Eid holidays. Mills stayed cautious, managing inventories instead of making fresh bookings, as construction activity slowed and bid-offer gaps persisted.

Offers for Australian shredded hovered at $375-380/t CFR Chattogram, with HMS 1 at $360-365/t and HMS 80:20 at $350-355/t.

Turkiye: The Turkish imported scrap market remained subdued with bulk HMS 80:20 prices stable at $347/t CFR, reflecting weak mill appetite amid sluggish domestic rebar demand. A few confirmed deals emerged, including Baltic cargoes sold at $346.50/t and others ranging from $338-342/t CFR from the UK and Europe.

Despite some active offers in the market, mills showed little urgency to book, citing limited finished steel sales and softening rebar prices, now ranging between $550-565/t exw. Mills maintained firm offer levels but avoided higher scrap purchases fearing they couldn’t pass on costs.

Short-sea activity also stayed quiet, with offers from Greece and Romania failing to draw interest. Overall, sentiments remained flat, with mills in wait-and-watch mode, hoping for a recovery in end-product demand before committing to fresh bookings.

Price assessments

India: UK-origin shredded indicatives were assessed at $367/t CFR Nhava Sheva, unchanged d-o-d.

Pakistan: UK-origin shredded indicatives stood at $383/t CFR Qasim, unchanged d-o-d.

Bangladesh: UK-origin shredded prices were assessed at $377/t CFR Chattogram, unchanged d-o-d.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $347/t CFR Turkiye, unchanged d-o-d.

Leave a Reply