- Indian buyers make selective purchases amid demand recovery

- Bangladeshi mills remain quiet on mill shutdowns, tight liquidity

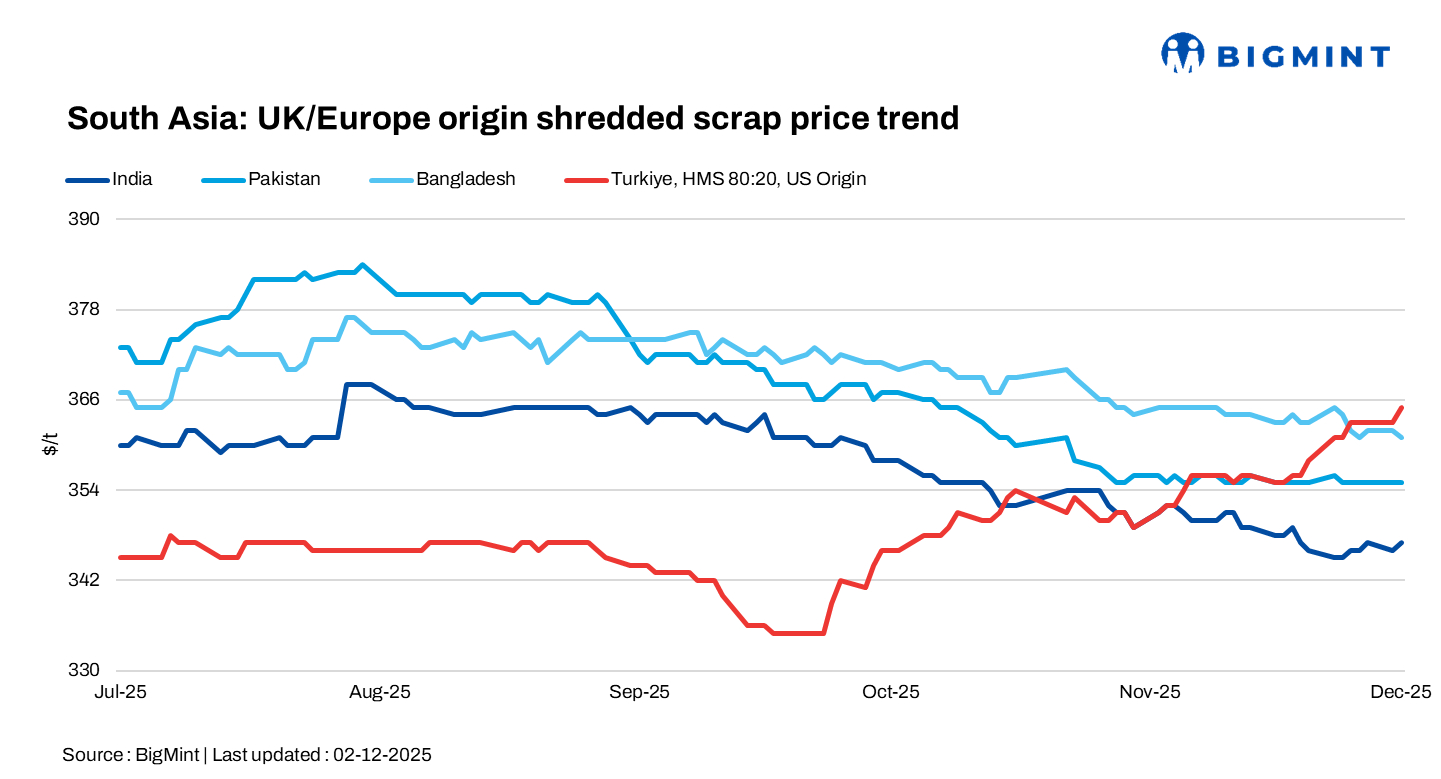

The South Asian imported scrap markets remained subdued on 2 December: India recorded selective purchases, Pakistan remained quiet but steady, while Bangladesh showed poor demand amid liquidity pressure and mill shutdowns. On the other hand, in Turkiye, prices rose, driven by tight supply, strong freights, and improved rebar demand.

India: Indian importers made selective purchases of ferrous scrap, indicating a slight recovery in demand. Last week, material flows from Australia into both South India and the Far East remained slow. While buying interest is gradually picking up, supply remains tight, as yards pause for the winter holidays. Rising Turkish prices have also rendered India temporarily unviable for some exporters.

Current offers include EU shredded at $350-352/t CFR Nhava Sheva, Hong Kong PNS at $360-365/t CFR Chennai, Malaysia busheling at $364-366/t CFR Chennai, and Australian shredded at $348-352/t CFR Chennai. Australian HMS 90:10 was indicated near $300/t for Far East buyers.

Pakistan: Imported scrap prices remained steady in Pakistan, with trade subdued, as mills remained cautious, focusing mainly on fabrication scrap from the UAE.

Recent deals for shredded were heard closed at around $355-360/t CFR amid soft demand despite firm offers from sellers. A 500-t EU shredded cargo was recorded as sold at $352/t CFR Qasim. Indicative levels for UK-origin shredded were at $350-355/t CFR, European shredded at $355-358/t, UAE HMS at $335-340/t, and UAE shredded at $360-362/t.

Bangladesh: Imported scrap demand in Bangladesh remained weak, as several mills were heard to have shut operations amid poor demand and liquidity pressure.

Current offers included Hong Kong PNS at $360/t CFR, Hong Kong shredded at $350/t, Australia HMS 80:20 at $330/t, Chile containerised HMS 80:20 at $320/t, and GI bundles from the Philippines at $295-300/t.

Turkiye: Deep-sea scrap prices rose d-o-d on 2 December, supported by strong dry-bulk freights, higher collection costs, and elevated rebar prices. Several deals were rumoured to have been closed late last week, but these remain unconfirmed, while sellers continued targeting higher levels amid bullish shipping costs.

Turkiye: Deep-sea scrap prices rose d-o-d on 2 December, supported by strong dry-bulk freights, higher collection costs, and elevated rebar prices. Several deals were rumoured to have been closed late last week, but these remain unconfirmed, while sellers continued targeting higher levels amid bullish shipping costs.

In Europe, a stronger euro and higher collection expenses also underpinned scrap pricing, limiting sellers’ flexibility. As a result, EU-origin HMS 80:20 was indicated at around $358/t CFR, while US-origin material was heard at $364-366/t CFR, with sellers maintaining a bullish stance for this week.

Leave a Reply