- India: Weak demand, wide gaps, imports remain slow

- Bangladesh: Stronger buying, better prices, deals continue

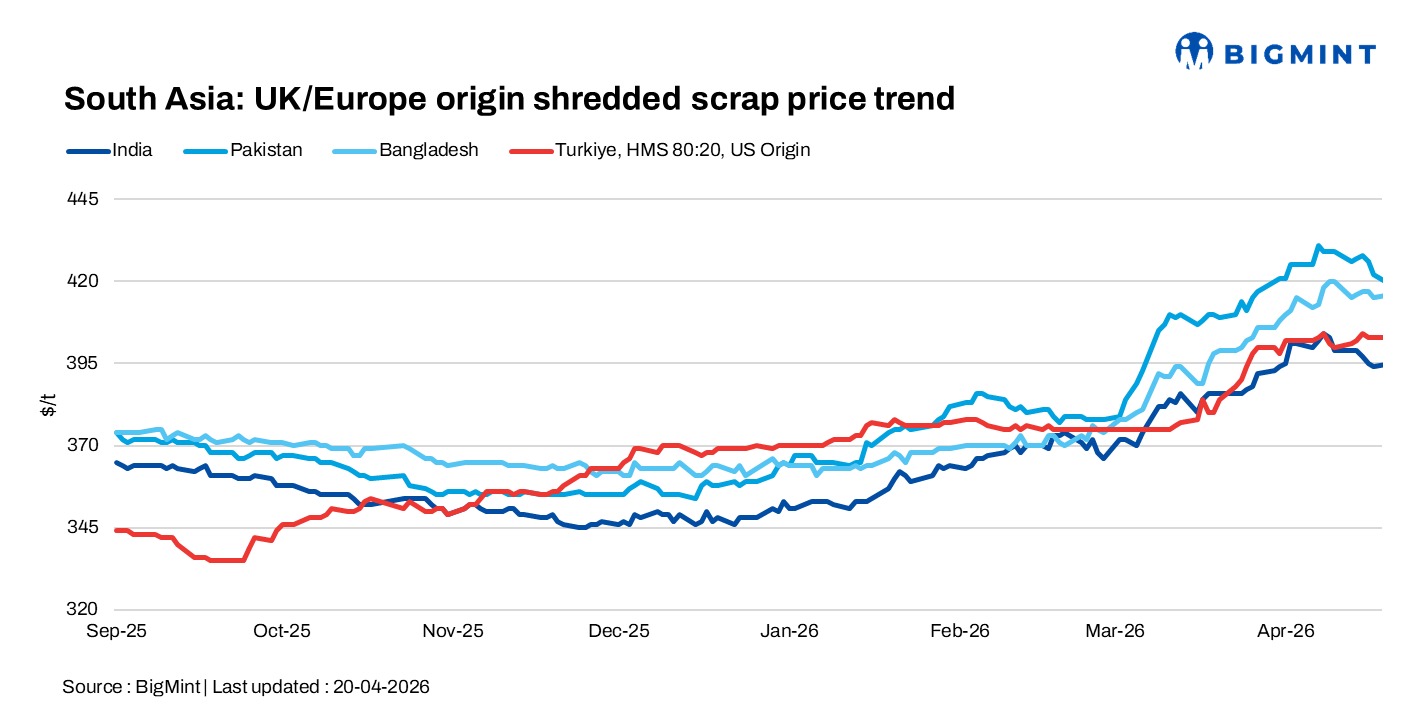

South Asia scrap markets remained subdued as of 20 April, with weak demand in India, soft sentiment in Pakistan, relatively stronger buying in Bangladesh, and firm Turkiye prices, as supply-side support persisted but downstream demand continued to limit activity.

India: The imported scrap market in India remained subdued, with limited buying interest and a clear gap between buyer expectations and seller offers. Offers for Chennai were heard at $415/t for NTP, $350/t for LMS bales and turnings, while NZ-origin HMS (2%) was at $390/t CFR with no takers. Brazil-origin HMS at $372-375/t and Central America sub-grade HMS at $358-360/t also struggled to find buyers, as mills continued to target lower levels.

Market sentiment stayed weak as buyers remained around $365-380/t, with offers such as East Africa cast iron at $390/t and Latin America handloaded HMS at $390/t failing to attract interest. Supply from UK/EU/US remained largely absent, with active origins limited to Brazil, Australia, and West Africa, while stronger buying from Bangladesh further diverted cargoes away from India, keeping the market quiet.

Pakistan: The imported scrap market in Pakistan softened slightly, with limited buyer interest keeping activity subdued. UK-origin shredded was heard at $420-422/t CFR Port Qasim, as reported by a shipper, reflecting cautious sentiment despite relatively firm offer levels.

Bangladesh: Imported scrap prices into Bangladesh remained largely stable, with PNS offers heard at $430-440/t CFR. A deal was reported for Australia-origin HMS 80:20 at $390/t CFR Chattogram, reflecting relatively stronger buying interest, as Bangladesh buyers continued to offer better rates compared to India.

Turkiye: Deep-sea scrap prices inched up on 17 April, supported by a pickup in deal activity towards the end of the week as mills returned to the market for May shipment requirements. Tradable levels for US/premium-origin HMS 80:20 were heard at $401.5-403/t CFR, reflecting firm supply-side support.

However, mills continued to resist higher prices amid weak downstream demand, with rebar export offers softening to $595-610/t FOB. This kept overall sentiment cautious, even as buying activity improved slightly.

Leave a Reply