- India: Buying weak amid currency pressure, slow sales

- Turkiye: Costs firm but mill demand stays limited

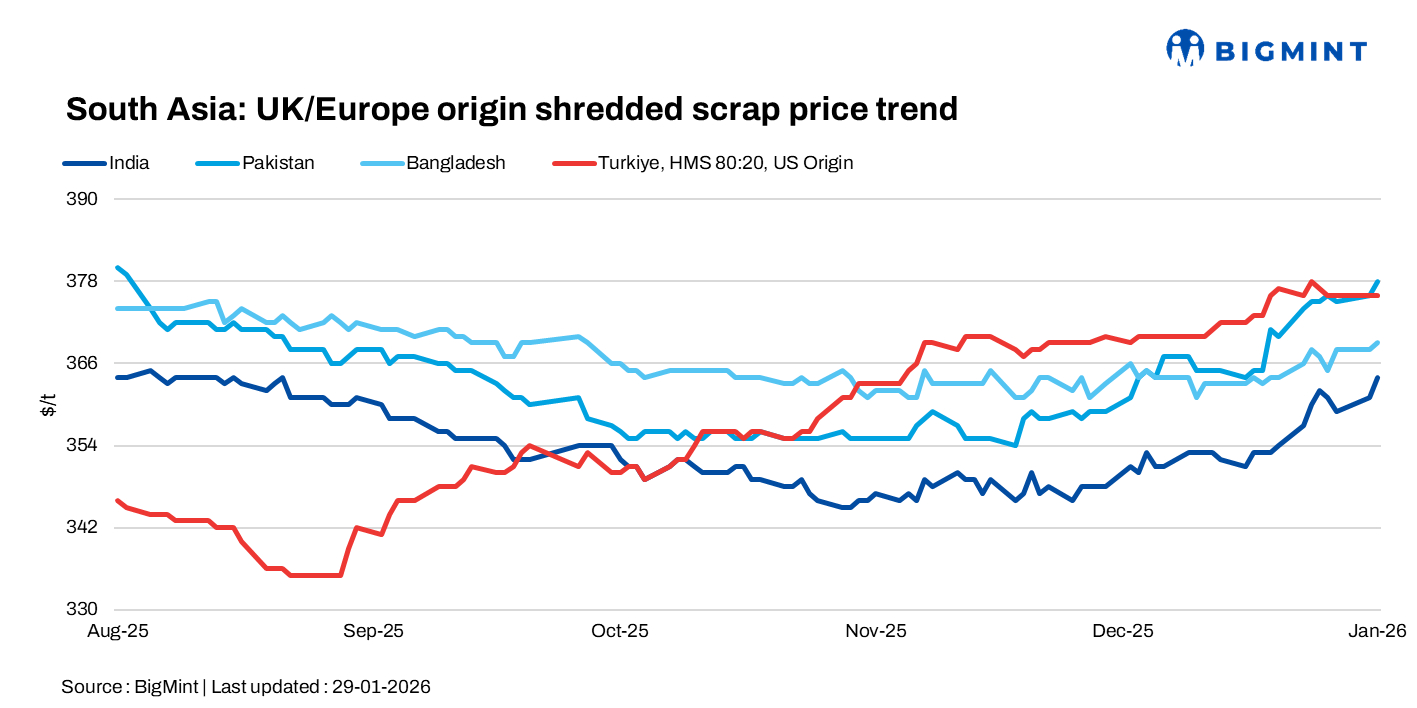

South Asia’s imported scrap market stayed subdued, with India cautious, Pakistan seeing selective buying, and Bangladesh steady but restrained. Turkiye remained supported by higher costs, though mill demand stayed weak, keeping overall trading sentiment muted.

Region-wise highlights

India: Imported scrap demand in India stayed weak as the rupee’s depreciation and sluggish finished steel sales kept buyers cautious, with HMS 80:20 showing a clear regional gap at around 350 CFR Mundra versus 335 CFR Chennai, while EU HMS 80:20 was offered at $340-345 against bids of $330-335. Australia-origin offers into Chennai continued to circulate but faced resistance amid a softer southern market, with indications around $330 for HMS 80:20 and $350 for shredded. Overall, north India remained firmer by $10-15/t compared with the south, keeping buyers selective.

Pakistan: Imported shredded scrap in Pakistan saw mixed indications, with UK/EU offers around $380 CFR, UAE suppliers signaling $395-plus, and a Bahrain-origin cargo expected to conclude near 390-plus. HMS demand also stayed active, with workable levels in the $365-375 CFR range, making Pakistan relatively attractive for suppliers. Local scrap hovered at PKR 135,000-136,000/t ($483-486/t), while the broader imported market continued to hold near the $380 CFR level.

Bangladesh: Imported ferrous scrap prices in Bangladesh remained steady, with Japanese H2 quoted around $355-357 CFR Chattogram and HS heard higher at $362-367. Containerised Oceania-origin offers also held within familiar bands, with HMS 80:20 at $345-350, HMS 1 at 355-360, shredded at $365-370, and PNS at $370-375 CFR, reflecting a stable but cautious buying environment.

Turkiye: Deepsea imported scrap prices inched higher on 28 January, supported by a stronger euro, firm collection costs, and rising dry bulk freight rates. Market participants noted that European sellers now face breakeven levels in the high-$370s CFR due to cost pressure, while US yards remained focused on the domestic market, where February shredded settlements are expected to rise by $20-30/t.

Despite the firmer cost environment, Turkish mill demand stayed muted as weak rebar sales kept buyers cautious. Participants described the week as largely silent, with both sellers and mills stepping back from active negotiations, resulting in limited fresh trade and a wait-and-watch market tone.

Despite the firmer cost environment, Turkish mill demand stayed muted as weak rebar sales kept buyers cautious. Participants described the week as largely silent, with both sellers and mills stepping back from active negotiations, resulting in limited fresh trade and a wait-and-watch market tone.

Leave a Reply