- Indian buyers hesitant amid weak demand, geopolitical uncertainty

- Turkish scrap market quiet, buyers cautious about prices

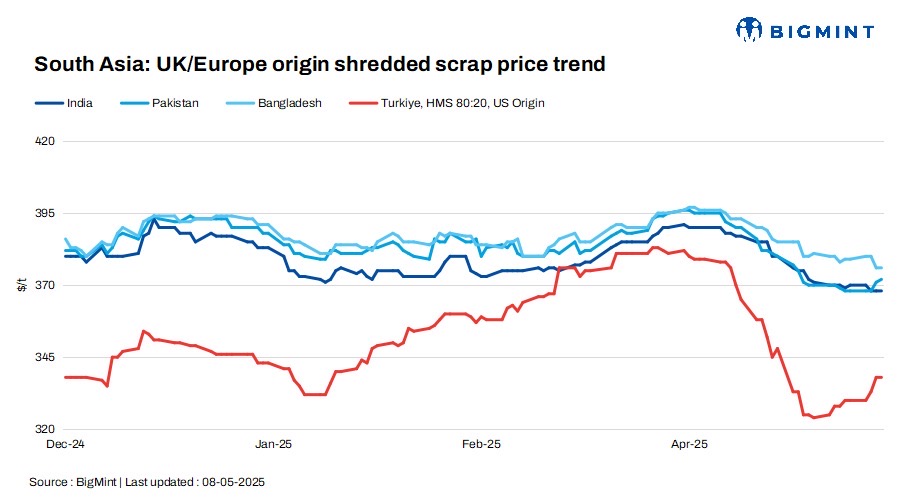

The South Asian imported scrap market remained largely quiet this week, with key players in India, Pakistan, Bangladesh, and Turkiye showing cautious behaviour amid weak domestic steel demand, geopolitical uncertainties, and seasonal factors.

In India, the market was slow as buyers refrained from purchasing due to approaching monsoons and weak steel demand, while Pakistan’s market faced low activity due to high inventory levels and stagnant domestic demand.

Similarly, Bangladesh’s market was subdued amid rising freight rates and weak construction activity.

In Turkiye, a similar cautious approach prevailed as buyers hesitated in the face of political and economic uncertainty, keeping overall market sentiment weak across the region.

UK-shredded scrap offers remained unchanged in India and Bangladesh, while edging up by $1/t in Pakistan. US-origin bulk HMS 80:20 offers to Turkiye also remained stable d-o-d.

Overview

India: India’s imported scrap market stayed muted as buyers remained hesitant amid approaching monsoon, weak domestic steel demand, and regional geopolitical uncertainties.

Shredded scrap offers hovered around $370-375/t CFR, while bids stayed lower at $360-365/t, causing a wide bid-offer gap and limited trades.

EU HMS 80:20 was offered at $350-355/t CFR, but buyer resistance capped it below $350/t.

Mills showed little interest in forward bookings, preferring ready cargoes instead. Market sentiment remained weak, with most participants in a wait-and-watch mode. Despite some support from the currency side and firm seller offers, subdued inquiries and unclear Turkish market trends weighed on activity.

Pakistan: Pakistan’s imported scrap market remained slow as mills had sufficient inventories while demand for steel still remained low in the domestic market. UK/Europe shredded scrap was offered at $370-375/t CFR Qasim. A few trades were heard at $373-375/t, yet margins remained tight.

Domestic rebar prices hovered at PKR 230,000-240,000/t ($823-859/t), while billet and scrap prices were stable at PKR 135,000-140,000/t ($480-497/t) and 195,000-200,000/t ($693-711/t).

Mills operated cautiously, facing pressure from geopolitical tensions and stalled public sector projects. With limited end-user demand and a persistent bid-offer gap, market sentiment stayed bearish, and scrap prices are expected to remain subdued in the short term.

Bangladesh: Bangladesh’s imported scrap market stayed muted as mills refrained from fresh bookings, pressured by rising freight rates, subdued construction activity, and squeezed rebar margins.

Australian shredded and PNS were offered at $375-380/t and $380-385/t CFR Chattogram, respectively, but trade remained limited due to buyer resistance and lower counterbids.

Ongoing liquidity issues, seasonal demand weakness, and overall market uncertainty kept mill buying interest low, resulting in minimal scrap transactions throughout the week.

Turkiye: Turkiye’s imported scrap market remained quiet as buyers stayed cautious amid weak steel demand and political-economic uncertainty.

US-origin bulk 80:20 prices held steady at $338/t CFR, with mills showing limited interest despite firm seller offers.

EU suppliers were also hesitant to make offers, awaiting a clearer market signal. Scrapyards in Europe raised dockside prices to attract flows, but Turkish buyers resisted higher prices, prioritising rebar sales before locking in scrap deals.

Price assessments

India: UK-origin shredded indicatives were assessed at $368/t CFR Nhava Sheva, unchanged d-o-d.

Pakistan: UK-origin shredded indicatives stood at $372/t CFR Qasim, up by $1/t d-o-d.

Bangladesh: UK-origin shredded prices were kept stable d-o-d at $376/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $338/t CFR Turkiye, unchanged d-o-d

Leave a Reply