- India: Imported scrap high, freight rise slows buying

- Pakistan: Domestic firm, Middle East shortage supports prices

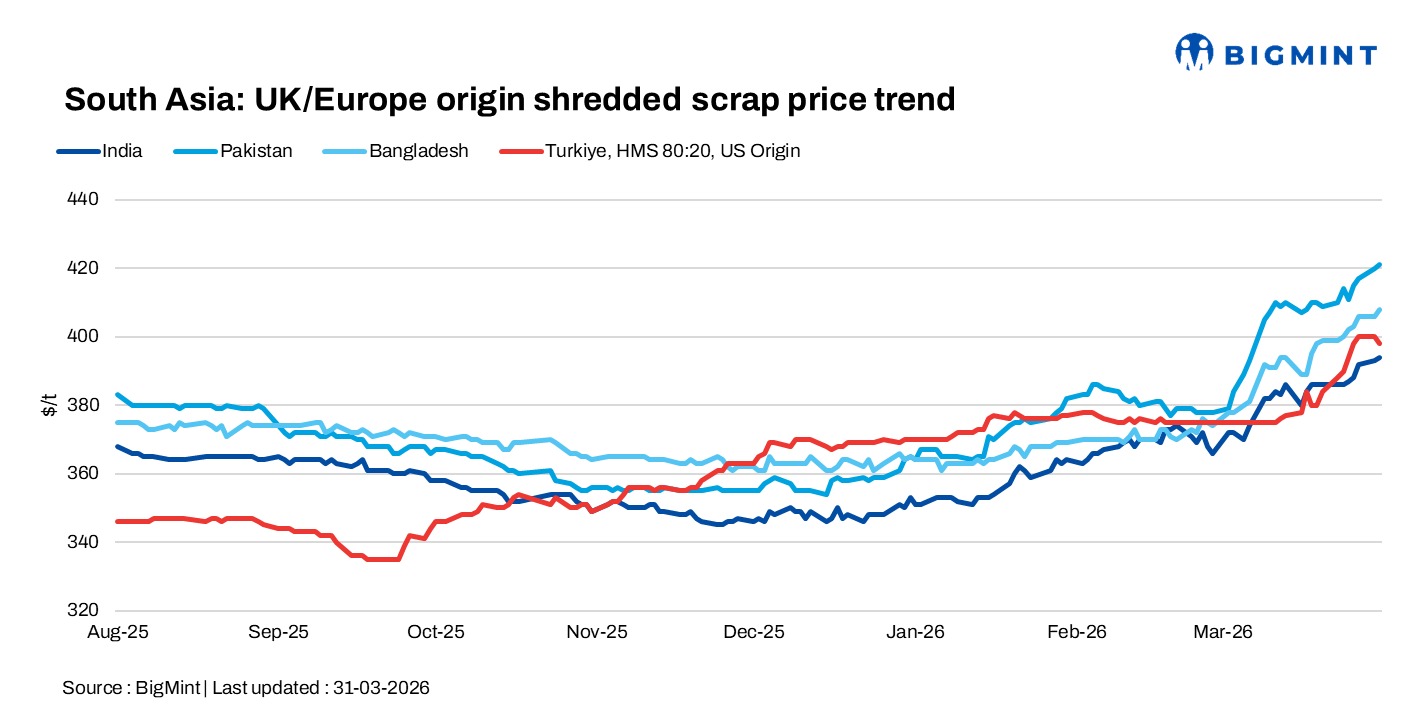

South Asia scrap markets on 31 March remained firm but sluggish, with elevated prices in India, Pakistan, and Bangladesh limiting buying interest. Tight supply, higher freight, and Middle East uncertainty kept sentiment cautious, while Turkiye market stayed stable with an upward bias.

India: Imported scrap market in India remains on the higher side, with Europe-origin HMS 80:20 offers at $380/t but workable at $370-375/t CFR and shredded near $390/t CFR. Freight has increased by $20-30/container due to ongoing geopolitical tensions, raising landed costs and slowing buying activity, as most buyers are holding back at current price levels.

Offers and indications in the market include UK-origin HMS at $375/t CFR, Chile-origin HMS at $376/t CFR, and Europe-origin PNS (heavy) at $415/t CFR. HMS 80:20 is heard at $380/t CFR with workable levels at USD 372-373/t, while New Zealand HMS (machine-loaded, 1-2% impurities) is at $365/t. Sub-grade shredded is at $355/t CFR, Senegal-origin HMS to Mundra at $373/t, and Mandvi/Ludhiana levels are around $370/t.

Africa-origin deep-sea scrap market is heard slightly up, with LMS at $325/t CFR CAD and 80:20 at $365/t CFR CAD, with against packing about $10/t lower. HMS vessel availability remains tight due to scrap shortage and transit container volumes are minimal. In India, supply concerns are emerging, particularly in Chennai where shortages are expected, while constraints in dolomite and limestone may impact primary steel producers.

Pakistan: Scrap market remains slow due to elevated finished steel and scrap prices, with domestic scrap currently around PKR 150,000/t and overall sentiment stable. Imported shredded scrap from the UK/Europe is heard at $423/t, while tightening supply in the Middle East-amid exhaustion of end-of-voyage cargoes in Dubai, Qatar, and Bahrain-has reduced regional availability, contributing to the recent firmness in Pakistan scrap prices.

Bangladesh: The imported scrap market remained stable at elevated levels, with UK-origin HMS at $380-385/t CFR and shredded scrap at $405-410/t CFR from various origins, while Australia-origin Bluesteel/Busheling workable at $425/t impurities is also being offered into the market, indicating continued firm pricing despite quality variations.

Turkiye: Deep-sea imported scrap market remained stable on 31 March with limited trading activity as mills stayed cautious, while US-origin scrap was heard around $398/t CFR. Demand remained subdued, driven more by geopolitical uncertainty than fundamentals, with rising freight and energy costs adding pressure. The outlook is slightly upward biased amid Middle East tensions, while rebar prices remain stable with export offers at $600/t FOB Turkiye and above as mills attempt to pass on higher costs.

Leave a Reply