- Turkiye prices risen by freight, market stays quiet

- Bangladesh oil disruption impacts costs, demand cautious

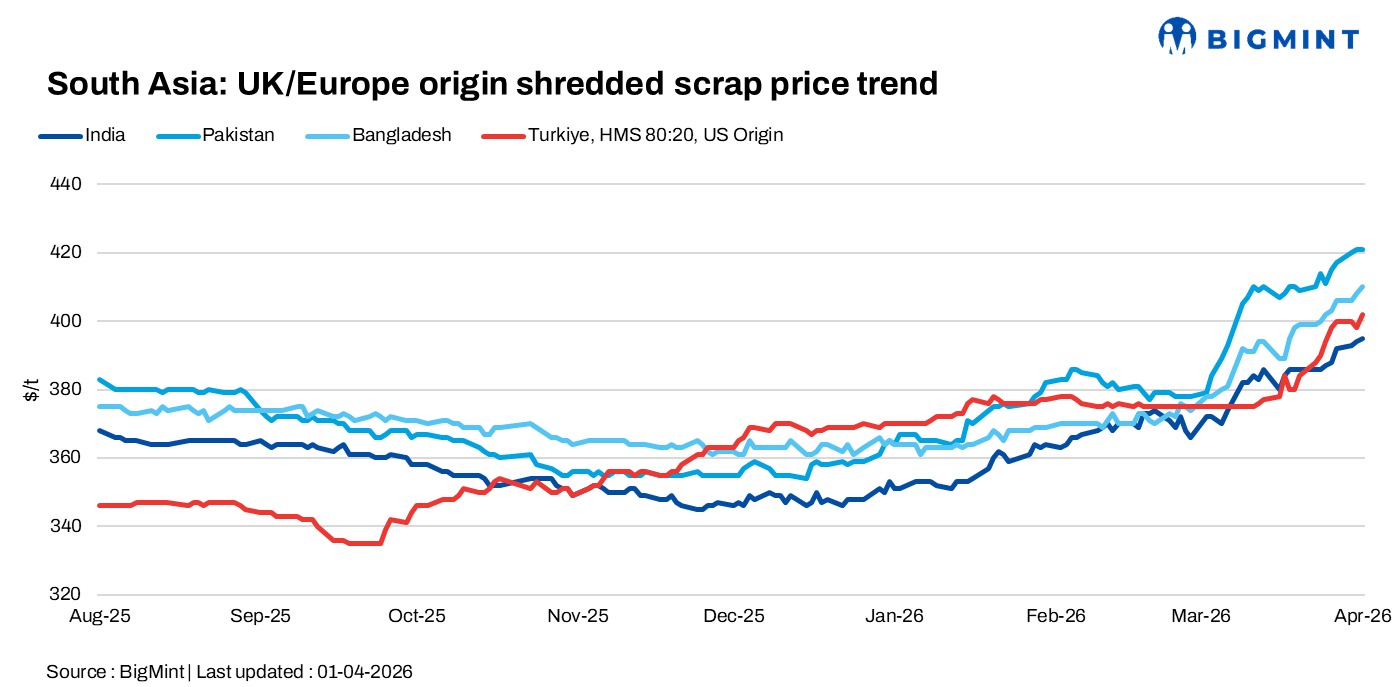

South Asia markets remained firm on 1 April, supported by tight supply and rising freight amid Middle East tensions, while buying stayed cautious across India, Pakistan, and Bangladesh, and Turkiye scrap prices strengthened to around $400/t CFR amid rising freight costs.

India: Imported scrap offers in India remained elevated, with Malaysia-origin HMS heard at $350-365/t, LMS (bundle) booked at $340-345/t CFR Chennai, while Costa Rica offers at $360/t for HMS 60:40 and $390/t for NTP were considered unworkable and largely withheld., while shredded scrap was heard around $420/t CFR. Broader market indications showed UK-origin HMS at $375/t CFR. New Zealand HMS (machine-loaded) was heard at $365/t, reflecting a firm but slow-moving market amid cautious buying.

Pakistan: Imported scrap prices in Pakistan remained firm amid tight supply, with shredded offers heard at $420-422/t CFR while buyers were at $415–417/t, indicating a narrow negotiation range. UK/Europe-origin shredded was reported around $423/t CFR, while shredded material booked at $415/t CFR Qasim. Freight from the UK to Port Qasim surged sharply to around $1,400-1,500/20 ft (up by $200), adding to landed costs, with buyers effectively paying a premium to secure material in the current constrained supply environment.

Bangladesh: The Bangladesh market remains stable from a government standpoint, but economic and industrial activity is yet to fully recover from earlier political disruptions. Ongoing Middle East tensions have impacted oil supply flows, particularly from Qatar.

Imported scrap prices remained stable at elevated levels, with UK-origin HMS at $380-385/t CFR and shredded at $408-410/t CFR, while Australia/New Zealand offers to Chattogram were heard at $380-385/t for HMS 80:20, $405-410/t for shredded, and $415-420/t for PNS.

Turkiye: Deep-sea scrap prices edged up on 1 April, with US-origin material heard around $403/t CFR, although the deals remain unconfirmed by the involved parties. Market activity was relatively subdued following stronger bookings last week, but sentiment remains steady.

Participants expect mills to gradually return to the market, as restocking requirements persist. For now, both buyers and sellers appear comfortable at current levels, with any further upside likely dependent on improved rebar demand.

Freight rates continue to support the firm trend, with US-origin cargoes around $50/t for Handymax vessels and Baltic cargoes at $50-55/t, depending on availability. Additionally, ongoing Middle East tensions post-Easter may provide further support to prices, even as US offers remain limited during the holiday period.

Leave a Reply