The South Asian ferrous scrap market witnessed a mixed trend today, reflecting varying dynamics across the region. In India, there was a slight uptick in demand for imported scrap due to limited availability domestically. Pakistani buyers maintained caution amid sluggish sales of finished steel, while Bangladesh faced sluggish demand attributed to a slowdown in the domestic steel market exacerbated by adverse weather conditions.

Shredded scrap offers saw a modest increase of $1/t in India and $2/t in Bangladesh while remaining unchanged in Pakistan. Meanwhile, US bulk HMS (80:20) offers to Turkiye remained steady d-o-d.

Overview

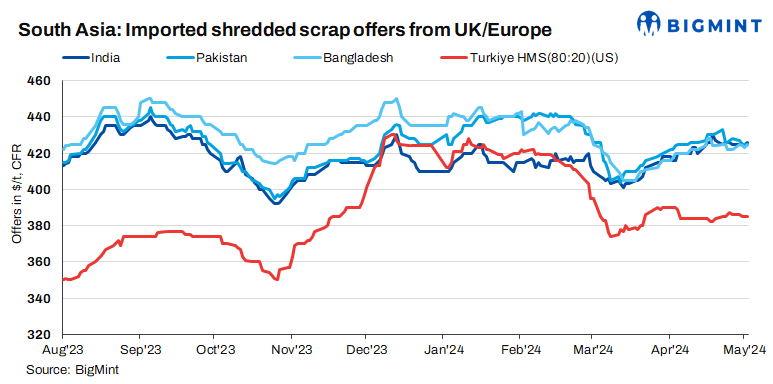

India: In India, demand for imported scrap has seen a slight uptick due to the limited availability of scrap in the domestic market. Shredded scrap offers from the US and Europe were reported at $425-430/t CFR, while HMS (80:20) from West Africa and Europe stood at $405-410/t CFR.

A representative from a steel mill based in southern India remarked, “The domestic market is witnessing an increase due to scarcity, albeit temporarily. Internationally, prices remain stable, and currently, international scrap is priced lower than local scrap. With scrap stocks dwindling, imports comprising 30-40% of our supply are becoming necessary. We’re avoiding purchases from the UK, the US, and the EU due to higher freight costs. Instead, destinations like Hong Kong, Australia, and South America are preferred.”

Pakistan: Pakistani buyers have continued to remain cautious, largely due to sluggish sales of finished steel in the domestic market. Notably, there have been no firm offers or bids reported today. However, indicative offers for shredded scrap from the UK/Europe were noted at $425/t CFR Qasim.

Bangladesh: Demand for imported scrap in Bangladesh has been sluggish, primarily due to a slowdown in the domestic steel market exacerbated by adverse weather conditions and the absence of significant new government project developments. Offers of shredded scrap from the UK/Europe were reported at $420-425/t CFR Chattogram, while HMS (80:20) stood at $400-405/t CFR.

According to a trader, “The current market is experiencing a relative slowdown, particularly in the rebar segment, following the absence of major government projects announced post-elections. The rebar market remains volatile, witnessing continuous fluctuations of approximately BDT 1,000-2,000/t w-o-w.”

Turkiye: Turkish deepsea imported ferrous scrap prices remained steady with offers for HMS (80:20) from the US at $385/t CFR, unchanged d-o-d. EU-origin HMS (80:20) ranged between $380-382/t CFR. Collection costs for HMS in the Benelux region rose to Euro 315-320/t delivered to the docks, impacting prices. Despite current Turkish mills’ disinterest, future demand is anticipated to drive prices up. However, a mill source expressed concerns over the competitiveness of Turkish steel due to the threat of Chinese exports, suggesting scrap prices should be below $350/t CFR. Meanwhile, Turkish rebar exports remained unchanged at $588-590/t FOB, with slow sales reported.

Price assessments

India: UK-origin shredded scrap indicatives were assessed at $426/t CFR Nhava Sheva, up by $1/t d-o-d.

Pakistan: UK-origin shredded indicatives were assessed unchanged at $425/t CFR Qasim, d-o-d.

Bangladesh: UK-origin shredded prices were assessed at $425/t CFR Chattogram, up by $2/t d-o-d.

Turkiye: US-origin HMS (80:20) bulk prices were assessed at $385/t CFR Turkiye, stable d-o-d.

Outlook

In the near term, imported scrap offers are expected to fluctuate due to sellers’ insistence on higher collection costs, while demand in Bangladesh and Pakistan remains subdued due to sluggish domestic steel markets. Meanwhile, in India, market activities may gain momentum post-elections, driven by increased steel demand and an anticipation of expansion in infrastructure projects.