The South Asian ferrous scrap market exhibited stability today, with sluggish buying interest prevailing across markets. Indian buyers continued to adopt a wait-and-see approach, influenced by price differentials. Pakistani buyers opted for need-based bookings, while Bangladeshi mills faced delays in opening fresh Letters of Credit (LCs).

Stability was seen in shredded scrap offers to India, Pakistan, and Bangladesh. Similarly, offers for US bulk HMS (80:20) to Turkiye remained unchanged today.

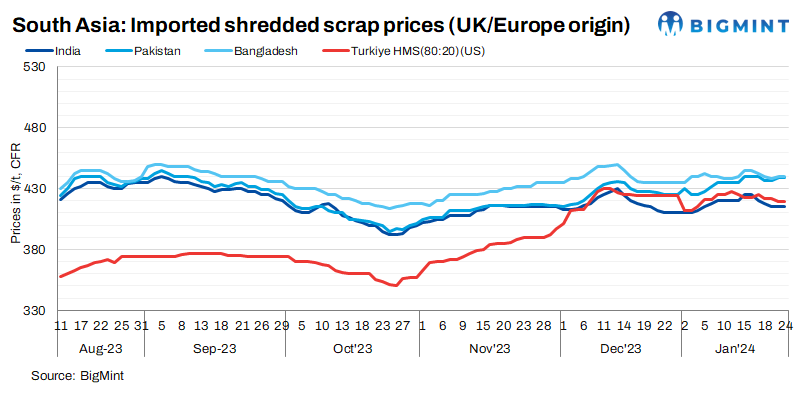

Market overview

India: In India, demand for imported scrap continued to be subdued due to the disparity between offers and bids, resulting in the absence of any firm offers or bids today. Indicative offers for shredded scrap from Europe were at $410-415/t CFR Nhava Sheva, while HMS (80:20) was reported at $395-400/t CFR.

A representative from a steel mill said, “Imported scrap prices are presently considered unviable; hence, we are abstaining from purchases.”

Pakistan: In Pakistan, demand for imported scrap remained as mills focused on meeting immediate requirements, influenced by a slowdown in the domestic steel market ahead of elections and the winter season. Indicative offers for shredded scrap from Europe were at $435-440/t CFR Qasim, while those from the Middle East were higher at approximately $445-455/t CFR. However, no transactions were reported due to uncertainty surrounding the potential implementation of export duties, as rumours circulated in the market.

Within the domestic market, major mills such as Faizan Steel, Moiz Steel, and Naveena Steel raised prices for grade 60 rebar effective from 23 January. Revised prices for 9.5/10mm and 12mm rebars were in the range of PKR 268,500-271,500, and for 12mm and above, prices were at PKR 266,500-269,500/t. The adjustments were deemed necessary by steel mills due to recent fluctuations in operational costs, increased input expenses, and prevailing market conditions.

Bangladesh: Market activities in Bangladesh remained sluggish, which can be attributed to the impending elections and challenges faced by buyers in obtaining LC approvals. Indicative offers for shredded scrap from Europe were reported at $440/t CFR Chattogram, while HMS (80:20) was priced at $420/t CFR.

In the domestic market, local scrap prices experienced an uptick due to shortages, compounded by difficulties in LC openings for buyers, as highlighted by market participants. Consequently, local scrap prices were at BDT 62,000/t for HMS (90:10), while PNS grade scrap was assessed at BDT 64,000/t.

Billet prices remained stable at BDT 77,000/t, while rebar prices were in the range of 89,000-90,000/t ex-Dhaka and BDT 90,000-95,000 ex-Chattogram.

Turkiye: The Turkish import market for ferrous scrap saw no change today, with uncertainty prevailing in the determination of tradable values. In contrast, US recyclers maintained firm positions. Indicative tradable values for US/Baltic-origin HMS (80:20) fluctuated between $415 and $420/t CFR, with a minimum of $420/t CFR.

Meanwhile, buyers chose to stay on the sidelines, exerting pressure on sellers, leading to a temporary halt in trading activities. In the Iskenderun region, domestic rebar sales were recorded at $630-$640/t exw. The spread between scrap and rebar widened to $197/t FOB compared to $184/t a week earlier.

Recent deals

- Around 500 t of AB bundles were procured from Philippines at $410/t CFR Chattogram.

Price assessments

India: UK-origin shredded scrap indicatives were assessed stable at $415/t CFR Nhava Sheva.

Pakistan: UK-origin shredded scrap indicatives were assessed stable d-o-d at $439/t CFR Qasim.

Bangladesh: UK-origin shredded scrap prices were assessed unchanged at $440/t CFR Chattogram d-o-d.

Turkiye: US-origin HMS (80:20) bulk prices were assessed flat at $419/t CFR Turkiye d-o-d.

Outlook

Imported ferrous scrap offers are expected to exhibit volatility, driven by a dearth of buying interest coupled with sellers maintaining a firm stance due to elevated collection costs.