- Indian buyers cautious amid falling Turkish prices

- Turkiye’s market stabilises with improved rebar sales

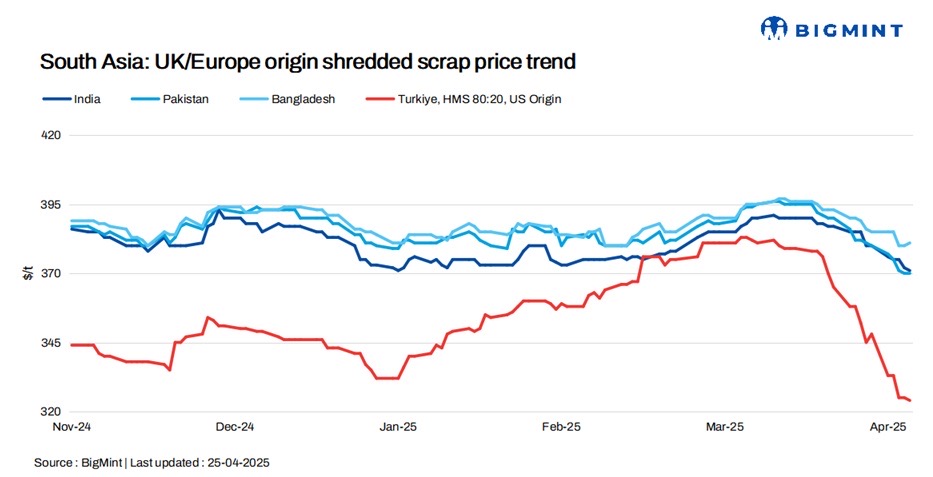

Imported ferrous scrap offers in South Asia showed mixed trends d-o-d, though movements were limited to a narrow range. UK-origin shredded dipped by $1/t in India, edged up by $1/t in Bangladesh, and remained unchanged in Pakistan. This follows subdued market sentiments, with sluggish demand and heightened caution among buyers due to global price fluctuations and domestic challenges.

In India, market activity was muted, as buyers adopted a wait-and-watch approach amid falling Turkish scrap prices and slack steel demand. Similarly, in Pakistan, weak domestic steel consumption and falling billet prices led to a slowdown in scrap trade, with limited activity in the market. Bangladeshi buyers also adopted a cautious stance, with mills delaying new bookings due to adequate inventories and rising production costs.

In contrast, Turkiye’s scrap market shows signs of stabilisation, driven by strategic restocking and some optimism from improving domestic rebar sales. US-origin bulk HMS 80:20 offers to Turkiye edged down by $1/t d-o-d.

Overview

India: India’s imported scrap market stayed subdued, as buyers adopted a cautious approach amid falling Turkish scrap prices, global uncertainty, and muted domestic demand. Shredded offers from the UK/Europe stood at $370-375/t CFR Nhava Sheva, but bids lagged at $365-370/t, with most buyers staying on the sidelines.

Even though seasonal demand and a 12% safeguard duty on steel imports offered momentary support, high freight costs, port inventories, and weak liquidity restricted fresh bookings.

HMS 80:20 offers from the UK/Europe stood at around $350/t CFR, while West African HMS 80:20 ranged within $350-360/t CFR, depending upon the container loading size.

Pakistan: Pakistan’s imported scrap market remained muted due to weak domestic steel demand, falling billet and rebar prices, and global market uncertainty led by Turkiye’s bearish trend.

Shredded offers from the UK/EU dropped to $370/t CFR Port Qasim, but buyers pushed for $365-370/t, leading to a bid-offer deadlock. A few small-lot container deals were done at $368-371/t CFR earlier in the week, but activity slowed sharply later.

Bangladesh: Bangladesh’s imported scrap market stayed sluggish, as buyers remained cautious amid weak finished steel demand, rising production costs, and currency concerns.

With sufficient stocks for May-June, mills delayed fresh bookings and focused on July shipments.

Shredded offers from Australia stood at around $380-385/t CFR, but these struggled to gain traction, while HMS 80:20 saw bids closer to $360/t CFR against $365-370/t CFR offers.

Turkiye: The Turkish imported scrap market remained under pressure but showed signs of stabilising, as mills continued restocking at slightly lower prices.

Bulk HMS 80:20 offers from the US and Baltic hovered at around $324-325/t CFR, while EU-origin cargoes traded lower at $315-320/t CFR.

Despite a persistent oversupply, some market participants believed a bottom was near, driven by improving domestic rebar sales and increased bookings.

European recyclers struggled to maintain margins due to high collection costs and currency pressure. With mills motivated to push down input costs and rebar exports firming up, sentiment leaned cautiously optimistic, with participants expecting stabilisation in the short term.

Price assessments

India: UK-origin shredded indicatives were assessed at $371/t CFR Nhava Sheva, down by $1/t d-o-d.

Pakistan: UK-origin shredded indicatives stood at $370/t CFR Qasim, unchanged d-o-d.

Bangladesh: UK-origin shredded indicatives edged up by $1/t d-o-d to $380/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices edged down by $1/t d-o-d to $324/t CFR Turkiye.

Leave a Reply