- Pakistan sees moderate activity despite liquidity issues

- Turkish offers rise, but mills struggle with rebar sales

South Asia’s imported scrap market saw mixed trends today. India’s offers rose despite muted buying interest, as mills remained cautious amid weak steel demand and economic challenges. Sluggish steel sales kept buyers focused on domestic scrap.

Pakistan witnessed moderate restocking ahead of Ramadan, though liquidity issues and price volatility limited activity. Bangladesh saw slight improvement as some buyers returned, but construction sector weakness kept demand uncertain.

Meanwhile, Turkiye’s scrap prices surged on a US-origin deal, though mills struggled with rebar sales.

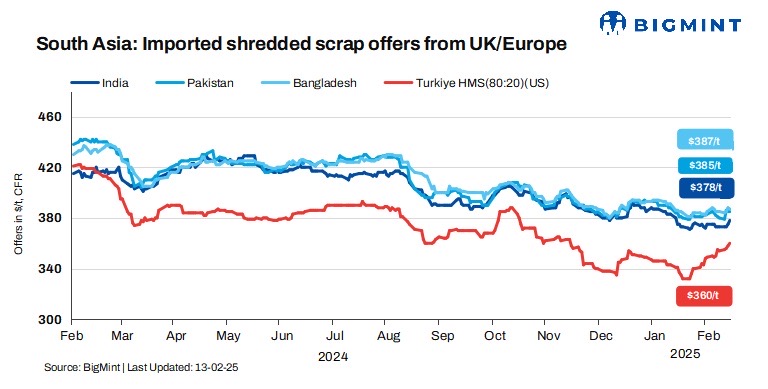

Shredded offers to India rose by $3/t d-o-d, while they remained unchanged in Pakistan and dropped by $1/t in Bangladesh. US-origin bulk HMS offers to Turkiye edged up by $2/t d-o-d.

Overview

India: India’s imported scrap market saw offers rise despite dull demand, as global suppliers held firm on pricing. Shredded from the US and UK/Europe was offered at $380-385/t CFR, while HMS (80:20) touched $355-360/t CFR. However, Indian buyers stayed cautious, preferring domestic scrap due to slow steel sales and higher import costs.

Suppliers also diverted shipments to Pakistan, where returns were better. With production running normally and the local market offering support, mills showed little urgency for imports.

Pakistan: Pakistan’s imported scrap market saw moderate activity, though buyers faced liquidity issues and sluggish rebar sales. Some restocking occurred ahead of Ramadan, but sentiment remained cautious due to price volatility. Shredded offers from the UK/Europe stood at $385-390/t CFR Qasim, while UAE-origin shredded was at $395/t CFR and HMS at $370/t CFR.

Local scrap prices stayed at PKR 140,000-145,000/t ($501-519/t), while rebar traded at PKR 245,000-255,000/t (878-913/t), reflecting a stable domestic market despite limited buying enthusiasm.

Bangladesh: Bangladesh’s imported scrap market showed slight improvement as some buyers returned, though overall sentiment remained cautious. Letter of credit (LC) issuance challenges persisted but were less severe than in previous months. Weak steel demand, sluggish construction activity, and a lack of new government projects kept mills from booking large volumes despite local scrap shortages.

Offers for Australian shredded stood at $370-375/t CFR Chattogram, US shredded at $365-370/t CFR, and Hong Kong PNS at $378-380/t CFR.

Some interest was seen in Japanese, Malaysian, and Singapore-origin material, but overall demand remained uncertain, with mills closely watching global price trends before committing to large purchases.

Turkiye: The Turkish imported scrap market saw a price hike, driven by a US-origin deal at higher levels, prompting recyclers to raise offers. US-origin bulk HMS (80:20) stood at $360/t CFR, up $2/t d-o-d. A 22,000-t deal from a US supplier set the tone for the market, leading to a strengthening in Baltic-origin scrap offers.

However, with mills struggling to sell rebars, preferences are shifting towards billets instead of scrap. The strong US domestic market further fuelled the uptrend, making it unlikely for recyclers to sell near $360/t CFR Europe.

Price assessments

India: UK-origin shredded indicatives were up by $3/t d-o-d at $378/t CFR Nhava Sheva.

Pakistan: UK-origin shredded indicatives were at $385/t CFR Qasim, stable d-o-d.

Bangladesh: UK-origin shredded was assessed at $387/t CFR Chattogram, down by $1/t d-o-d.

Turkiye: US-origin HMS (80:20) bulk scrap edged up by $2/t d-o-d to $360/t CFR Turkiye.

Leave a Reply