- Indian buyers resist high scrap offers

- Turkish scrap market at a standstill

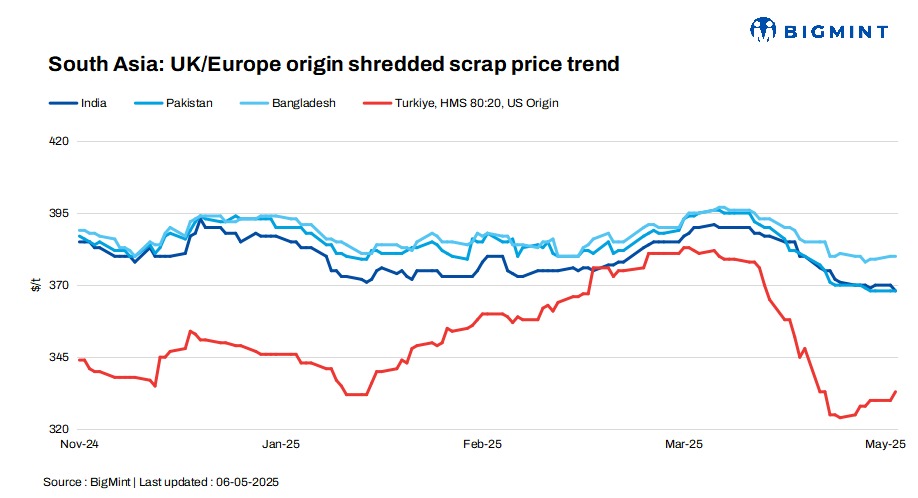

South Asia’s imported scrap markets remained subdued across the board, marked by sluggish buying interest, persistent bid-offer gaps, and caution stemming from both global and domestic uncertainties.

While India grappled with geopolitical concerns and weak finished steel demand, buyers in Pakistan and Bangladesh stayed on the sidelines due to soft market fundamentals, tight liquidity, and high inventories.

Despite some positive indicators like improved LC activity in Bangladesh and a slight currency lift in India, scrap trades remained limited.

Meanwhile, Turkiye’s market offered little support, as price resistance and weak demand kept buyers from engaging, further dampening sentiment across the region.

Overview

India: India’s imported scrap market remained quiet as buyers stayed cautious amid geopolitical uncertainty and soft domestic steel demand. Shredded scrap offers stood at $370/t CFR, but buyers held bids lower at $360-365/t, leaving limited room for deals. HMS 80:20 from the EU was offered at $358-360/t CFR, while buyers resisted crossing $350/t. High-quality grades like German busheling, offered at $384-388/t CFR, saw no major response. Mills preferred ready material and avoided bulk bookings, reflecting limited confidence. Despite currency support and firm offers from suppliers, the wide bid-offer gap and slow inquiries kept trading activity subdued.

Pakistan: Pakistan’s imported scrap market remained sluggish as buyers stayed cautious amid falling domestic steel prices, soft demand, and Turkish market volatility. The UK/EU-origin shredded scrap was offered at $370-372/t CFR Port Qasim, but deals were limited to $365-370/t, with bids mostly at the lower end. The persistent bid-offer gap and weak sentiment kept trading volumes low.

Mills operated below capacity, with inquiries selective and focused on lower prices. Domestic scrap rates held steady at PKR 135,000–138,000/t, but purchases stayed minimal due to high inventories and slow market activity.

Bangladesh: Bangladesh’s imported scrap market stayed muted as mills held back from fresh purchases amid weak steel demand, tight liquidity, and high inventories. After a wave of recent bookings, both bulk and containerised trade slowed.

Offers for Australian shredded were heard at $380-385/t CFR Chattogram, with bids trailing at $375-378/t, leading to limited deal-making. PNS scrap from Singapore was offered at $385-390/t CFR.

Despite easing port congestion and improved LC activity — with March LC openings and settlements crossing $6 billion — buyers remained cautious, tracking global cues and anticipating price corrections. Domestic rebar demand stayed soft, with Dhaka mills offering discounts amid low interest.

Turkiye: The Turkish imported scrap market remained sluggish, with no fresh deals as mills held back, waiting to gauge rebar demand. Suppliers stayed firm amid weak collection, while US exporters pushed for over $340/t CFR. Turkish buyers resisted, keeping the market at a standstill with HMS 80:20 prices stable at $330-335/t CFR.

Price assessments

India: UK-origin shredded indicatives were assessed at $368/t CFR Nhava Sheva, down by $2/t d-o-d.

Pakistan: UK-origin shredded indicatives stood at $368/t CFR Qasim, unchanged d-o-d.

Bangladesh: UK-origin shredded prices remained unchanged d-o-d at $380/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $333/t CFR Turkiye, up by $3/t d-o-d.

Leave a Reply