- Indian demand rises amid steel price hikes

- Turkiye battles ample stocks, weakened euro

South Asia’s ferrous scrap market experienced contrasting trends as regional demand, economic pressures, and global cues shaped varied market responses. India’s scrap demand strengthened on the back of domestic steel price hikes and tight local supply, while concerns over post-US election price increases added urgency to buying activity. In Pakistan, mills exercised caution amid limited scrap purchases due to elevated offers. Bangladesh, however, saw subdued activity because of weakened construction demand, financial constraints, and paused infrastructure projects sharply reducing rebar sales.

Meanwhile, Turkiye’s scrap market softened slightly as mills remained hesitant amid ample supply and ongoing anticipation of economic policy shifts in China.

Overview

India: India’s imported scrap demand climbed as buyers showed active interest, spurred by tight domestic supplies and concerns over potential price rises following the US elections. In the domestic market, a rise in steel demand, coupled with primary mills raising finished steel prices by up to INR 1,000-1,500/t for November sales, boosted market sentiment.

Imported shredded scrap offers from the US and UK/Europe rose to $400-405/t CFR Nhava Sheva, though buyers aimed to settle around $395/t. HMS 80:20 from the UK/Europe and West Africa saw offers at $370-375/t, while HMS 1 from South Africa was at $385-390/t CFR.

Pakistan: Pakistan’s imported scrap market saw cautious buying, with mills showing limited interest amid higher offers. Shredded scrap from the UK/Europe was quoted at $395-400/t CFR Qasim, while buyers held firm at $390-393/t CFR. The domestic rebar market remained stable with steady sales.

Bangladesh: Bangladesh’s imported scrap market remained sluggish due to weak domestic steel demand and ongoing financial hurdles, with no major transactions reported. The new interim government’s pause on infrastructure investments has led to rebar demand plummeting by 40-50%, leaving mills with high scrap inventories and limited appetite for new bookings.

Rebar prices fell to BDT 81,000-82,000/t in Dhaka and BDT 85,000-86,000/t, down significantly from August levels, as construction slowed. Payment challenges, particularly with letters of credit (LC), have worsened, further complicating imports.

While some mills shifted to smaller bulk purchases from Japan and Singapore, deep-sea and containerised scrap trades remained sparse, with bids well below recent offers.

Bangladesh Steel Re-Rolling Mills (BSRM) has launched a new rebar mill in Chattogram with a 600,000 tpy capacity, boosting its total long products capacity to 2.4 million tpy. The facility will produce 8-50 mm straight rebar and rebar coils.

Turkiye: The Turkish imported scrap market softened today following a Baltic-origin deal at $362/t CFR, down $3/t from the previous day. While demand from Turkish mills remained subdued amid slowed rebar sales and expected billet arrivals, sellers hesitated, awaiting a potential stimulus package announcement from China. The euro’s recent weakness, although partially recovering, made Baltic and EU recyclers slightly more competitive, fueling hopes for lower offers. Despite this, most recyclers held firm, with EU-origin offers hovering around $365/t CFR. Turkish mills, however, capped their bids at $355/t CFR for EU scrap, signaling bearish price expectations amid ample supply and muted buying interest.

Price assessments

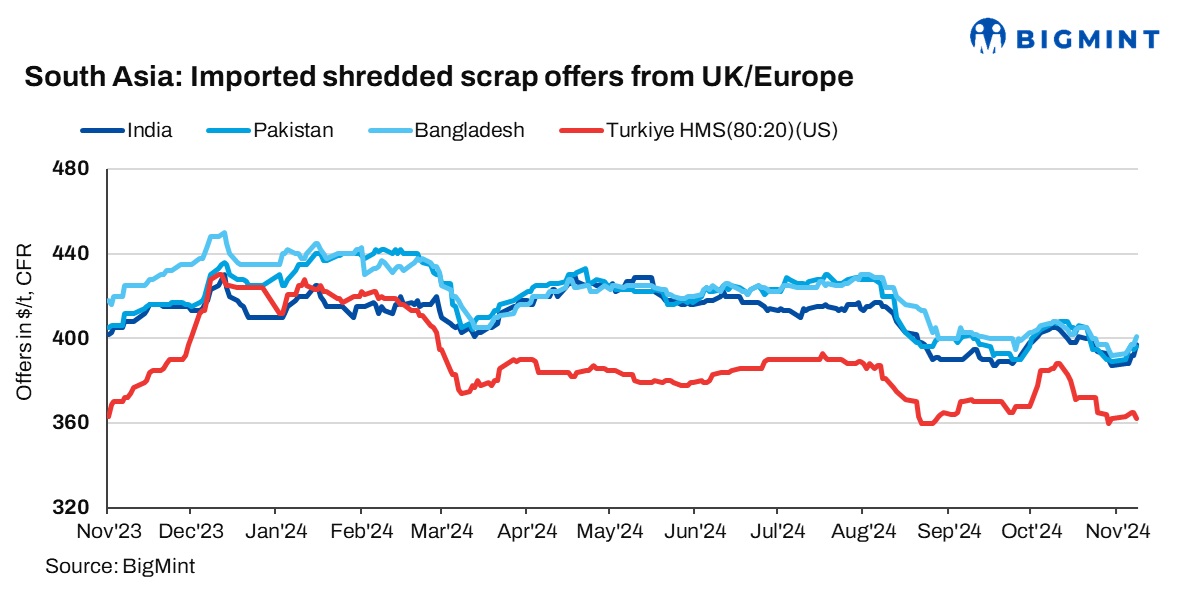

India: UK-origin shredded indicatives edged up by $5/t d-o-d to $397/t CFR Nhava Sheva.

Pakistan: UK-origin shredded indicatives inched up by $1/t d-o-d to $396/t CFR Qasim.

Bangladesh: UK-origin shredded prices were assessed at $401/t CFR Chattogram, up by $4/t d-o-d.

Turkiye: US-origin HMS (80:20) bulk prices edged down by $3/t d-o-d at $362/t CFR Turkiye.

Leave a Reply