- Bangladesh saw cautious buying post-Eid

- Turkiye’s imported scrap market weakened further

South Asia’s imported scrap market remained largely subdued this week as buyers across India, Pakistan, and Bangladesh exercised caution amid bid-offer mismatches, financial constraints, and tepid steel demand. In India, expectations of a price drop kept buyers on the sidelines.

Pakistan’s market saw minimal post-Eid activity despite some relief from electricity tariff cuts, while Bangladesh faced persistent LC challenges and selective demand even as rebar sales showed minor recovery.

Meanwhile, in Turkiye, bearish sentiment deepened as bulk scrap prices slipped further with mills reluctant to book amid rising production costs and weak US market cues.

Overview

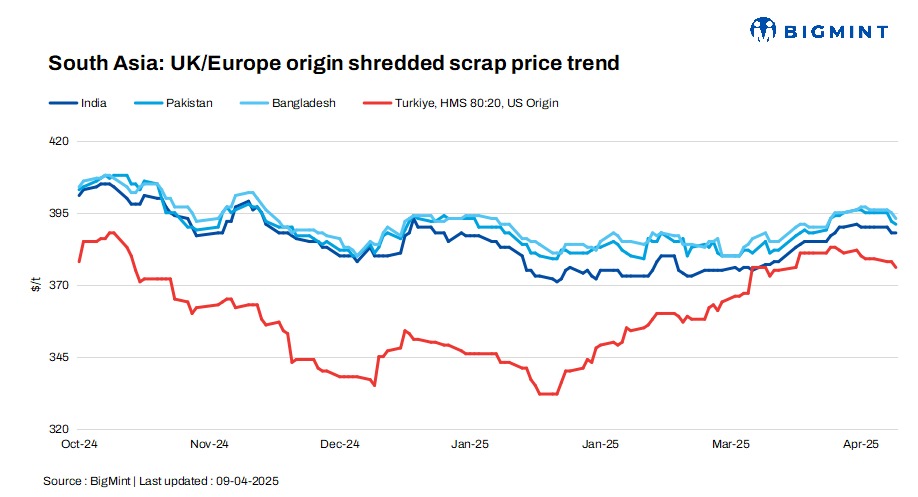

India: Indian buyers stayed mostly on the sidelines as a wide bid-offer gap and expectations of price corrections kept interest low. Shredded scrap offers from the UK/Europe were quoted at $390-395/t CFR Nhava Sheva, but buyers were only willing to bid at $380-385/t CFR.

HMS 80:20 offers stood at $360-365/t CFR.

“Market sentiment is very weak and looks fragile,” said a mill official, while another importer based in southern India noted, “Right now, we’ve stopped imports.”

Pakistan: Pakistan’s imported scrap market remained quiet after Eid, with limited buying activity and a cautious outlook. Shredded scrap offers from the UK/EU were reported at $390-395/t CFR Qasim, while UAE-origin material was offered between $395-400/t.

On the domestic front, scrap prices stood at PKR 135,000-140,000/t ($487-505/t), billets at PKR 200,000-205,000/t ($722-740/t), and rebars at PKR 235,000-240,000/t ($848-866/t).

Recent electricity tariff cuts provided some relief to mill margins, but market momentum remained slow. Imported scrap prices are expected to stay firm in the near term, though a meaningful recovery may depend on restocking interest and policy cues from the upcoming budget.

Bangladesh: Bangladesh’s imported scrap market remained moderate after Eid, with limited buying due to ongoing LC issues and selective demand. Shredded scrap was offered at $385-395/t CFR Chattogram, Australian HMS 80:20 at $365-370/t, and PNS from Hong Kong and East Asia at $390-395/t.

Despite slow imports, domestic rebar sales improved slightly, prompting a BDT 500/t increase by Dhaka mills. Rebar prices were reported at BDT 80,000-82,000/t ($657-674/t) in Dhaka, while major Chattogram mills’ rebar prices were heard BDT 84,000-85,000/t ($690-698/t). Local HMS scrap stood at BDT 55,000/t ($452/t) and PNS at BDT 56,500-57,000/t ($464-468/t).

Turkiye: The Turkish imported scrap market remained under pressure with bulk scrap prices falling further amid a persistent lack of buying interest from mills. Offers for US-origin bulk HMS 80:20 at $376/t CFR, down $2/t d-o-d.

Mills stayed withdrawn from the market, with bearish sentiment deepening due to weak domestic scrap settlement expectations in the US and rising production costs in Turkiye. Sellers reported difficulty in attracting inquiries, as buyers waited for clarity on steel sales.

Ample May shipment availability failed to prompt offers, as suppliers feared self-competition. Overall, sentiment was weak, with both mills and recyclers hesitant to move without stronger market signals.

Price assessments

India: UK-origin shredded indicatives were assessed at $388/t CFR Nhava Sheva, unchanged d-o-d.

Pakistan: UK-origin shredded indicatives edged down by $1/t d-o-d to $391/t CFR Qasim.

Bangladesh: UK-origin shredded indicatives stood at $393/t CFR Chattogram, down by $2/t d-o-d.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $378/t CFR Turkiye, down by $2/t compared to the yesterday.

Leave a Reply