- Turkiye mills delay bookings amid weak steel sales

- Pakistan mills operate below half of capacity

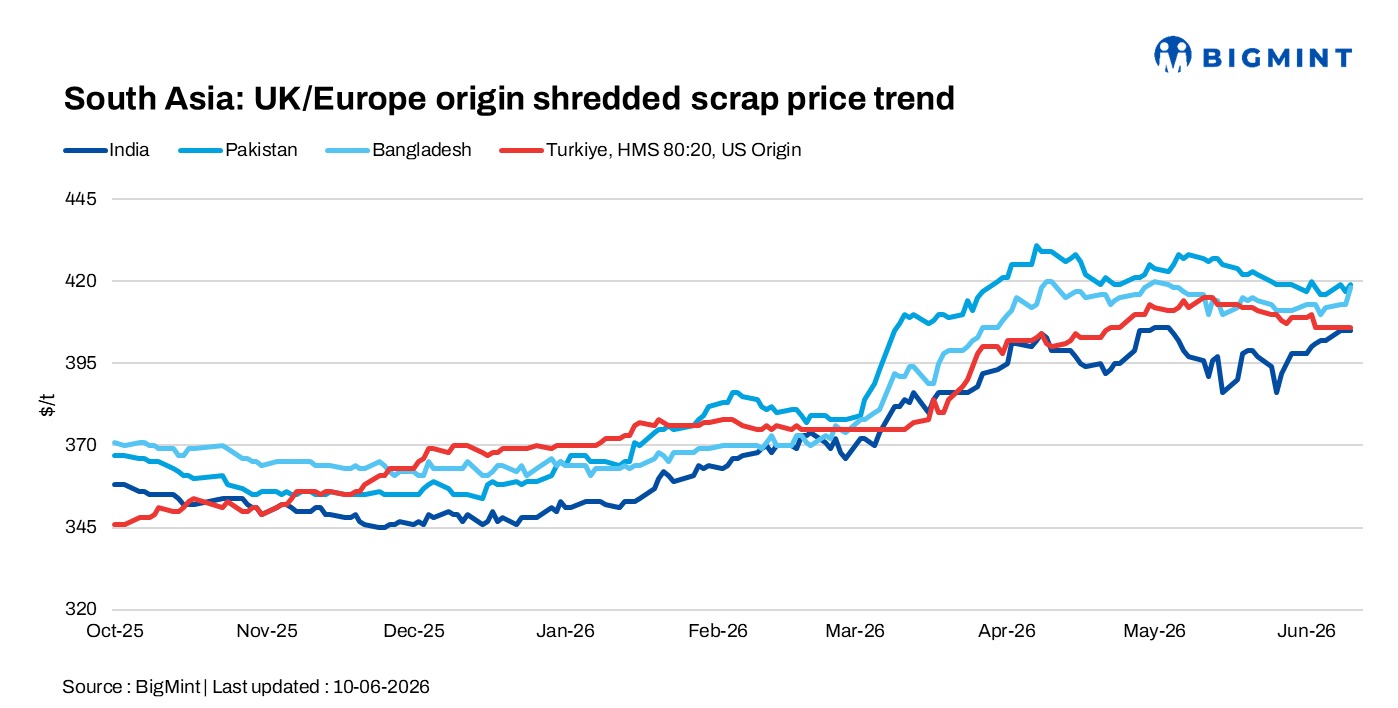

South Asia imported ferrous scrap markets remained subdued on 10 June, with weak steel demand, cautious mill buying, and wide bid-offer gaps continuing to restrict bookings across India, Pakistan, and Bangladesh. Meanwhile, Turkiye’s deep-sea scrap market remained stable, supported by upcoming July-shipment procurement requirements.

India: Imported scrap market remained subdued, with buying interest staying limited as mills continued to resist higher offer levels. Market participants noted that suppliers currently prefer selling into Southeast Asia and Bangladesh, where buyers are willing to pay $15-20/t more than Indian buyers. Offer indications were also heard at $360/t CFR for UK-origin HMS 80:20 (3% impurities) and $345-347/t CFR for Philippines-origin GI bundles.

Pakistan: Imported ferrous scrap market remained subdued, with shredded scrap offers heard at $420-425/t CFR Qasim and UK-origin shredded scrap at around $420/t CFR. Mills continued operating at low capacity utilisation of 35-40% amid weak steel demand. Domestic billet prices were reported at PKR 215,000/t, Grade 60 rebar at PKR 240,000-245,000/t, local scrap at PKR 155,000/t, and Bala at PKR 200,000-205,000/t, while buying activity remained cautious.

Bangladesh: The imported scrap market remained subdued, with mills continuing to show limited buying interest amid weak steel demand and a wide bid-offer gap. Shredded scrap bids were heard around $410/t CFR Bangladesh, while Australia-origin shredded scrap was offered at $420-425/t CFR and UK-origin shredded scrap at $425-430/t CFR.

Market participants noted that suppliers remain more focused on sales to Southeast Asia and Bangladesh, where buyers are willing to pay $15-20/t more than India. UK-origin HMS 80:20 (3% impurities) was offered at $360/t CFR Bangladesh, while Philippines-origin GI bundles were heard at $345-347/t CFR.

Turkiye: Deep-sea imported scrap market remained largely stable on 9 June, with workable levels for bulk cargoes heard at $400-405/t CFR. Mills largely stayed on the sidelines as weak billet and rebar demand continued to pressure steel margins. However, the need to secure July-shipment cargoes helped support sentiment and limit further downside.

Leave a Reply