- Portside inventories of thermal coal up 5% w-o-w

- Sponge iron prices in eastern India drop by INR 500/t w-o-w

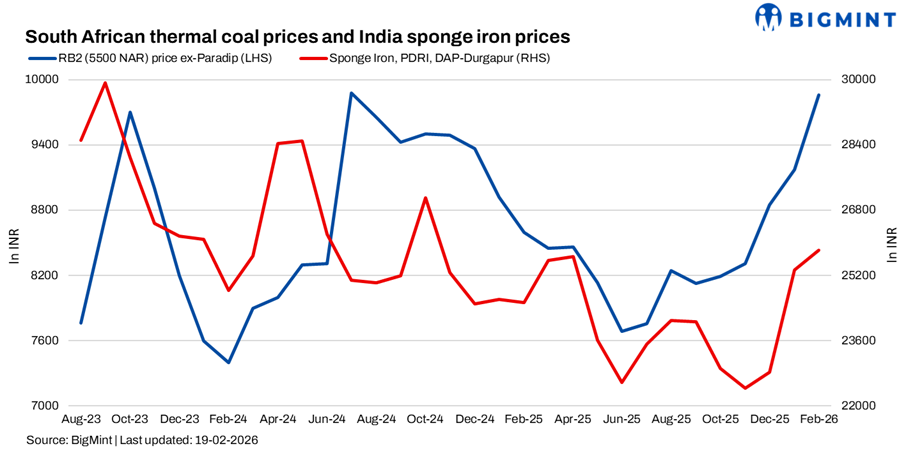

South African thermal coal prices at Indian ports continued to increase w-o-w amid firm export offers and tight grade-wise availability. As per BigMint’s assessment, exw-Paradip 5,500 NAR rose by INR 350/t to INR 10,350/t, while 4,800 NAR increased by INR 400/t to INR 9,000/t.

At Vizag, 5,500 NAR gained INR 200/t to INR 10,100/t and 4,800 NAR rose by INR 350/t to INR 8,850/t. Export offers for 5,500 NAR increased by $4-6 w-o-w to around $91/t FOB RBCT, supported by mine maintenance and operational disruptions in South Africa, which tightened prompt supply and lifted sentiment at Indian ports. No South African stock was reported at Haldia, reinforcing concerns of cargo shortage ahead.

“Despite higher offers, hardly any fresh deals were heard, as buyers remained in wait-and-watch mode due to margin pressures.”, quoted a source.

Port side inventories climb to 27-week high

Total portside thermal coal inventories across India increased 5.3% w-o-w to 14.06 mnt in week 7 from 13.35 mnt in week 6. The latest level marked a 27-week high, last seen in week 31 of CY25 at 14.27 mnt.

While aggregate stocks improved, availability of specific South African grades remained uneven across ports, and supply tightness in certain locations continued to support elevated offers. The stock build reflected broader arrivals, but did not fully ease concerns around prompt South African cargo inflows.

Sponge iron weak; domestic coal steady

Sponge iron P-DRI DAP Durgapur declined by INR 500/t w-o-w to INR 25,000/t. The sponge iron market witnessed mixed trends, with subdued regional demand patterns dampening overall trading activity. In eastern India, buyer participation remained weak, with procurement restricted to need-based volumes amid slow finished steel movement and limited liquidity.

Domestic non-coking coal prices remained stable w-o-w, with 4,500 GCV at INR 4,850/t and 5,000 GCV at INR 5,850/t as per BigMint’s assessment. However, the widening differential between imported and domestic coal continued to influence procurement strategies, with several consumers showing preference for domestic material. Market participants indicated that imported coal prices were rising sharply due to Indonesian production cuts linked to RKAB policy discussions, further strengthening domestic coal’s competitive position.

Outlook

Sentiment remained firm but cautious. Higher export offers from South Africa amid mining disruptions and policy uncertainty in Indonesia continued to support imported coal prices. However, buyers were holding back fresh trades as elevated raw material costs threatened margins.

Going ahead, domestic coal is likely to emerge as a stronger alternative if imported prices remain elevated. At the same time, cargo shortages and export constraints may keep portside sentiment firm, even as actual transaction activity stays selective.

Leave a Reply