- Stringent safety inspections could tighten thermal coal supply too

- Imports cannot easily replace Chinese production disruptions at scale

China’s recent mine accident in Shanxi has triggered an important repricing in domestic coal markets. At first glance, the reaction appears counterintuitive. The accident primarily affected coking coal mines, yet the sharper market signal has emerged in thermal coal, with Qinhuangdao prices moving higher after a period of stability.

The reason is simple: the thermal coal market is not reacting merely to direct supply loss. It is responding to the risk of a broader safety inspection cycle across China’s main coal-producing provinces. That distinction matters because China’s domestic coal balance had already tightened before the accident. The incident did not create the tightness — it exposed the lack of supply cushion in an already finely balanced market.

China’s coal balance was already tightening

Headline production data initially suggested relative stability. According to NBS China, cumulative raw coal production during January-April 2026 reached around 1.58 billion tonnes, marginally lower by 0.1% y-o-y, indicating broadly stable output despite weaker m-o-m production in April.

However, steady production growth had not kept pace with stronger power demand.

Thermal power generation during the same period rose 3.1% y-o-y, while total electricity generation increased 3.3% y-o-y, supported by industrial activity and seasonal demand. Although hydro output rose a strong 12.2%, helping moderate thermal coal burn, coal consumption remained resilient.

The implication is important: China entered the Shanxi accident with stable domestic coal supply, while power demand continued growing. The market, therefore, had little margin for fresh disruption, particularly ahead of summer cooling demand.

Why thermal coal is reacting to a coking coal accident

The direct production impact remains concentrated in coking coal, where mine closures and inspections matter immediately for steelmaking raw materials.

Thermal coal, however, is reacting through a different mechanism: regulatory contagion.

If safety inspections remain confined to the affected region, the price impact may prove temporary. But if inspections broaden across major producing regions such as Inner Mongolia, Shaanxi and Shandong, the implications for China’s thermal coal supply become materially larger.

The market is therefore not pricing the accident alone. It is pricing the possibility that inspections evolve into a broader supply-management event.

The Inner Mongolia and Shaanxi risks

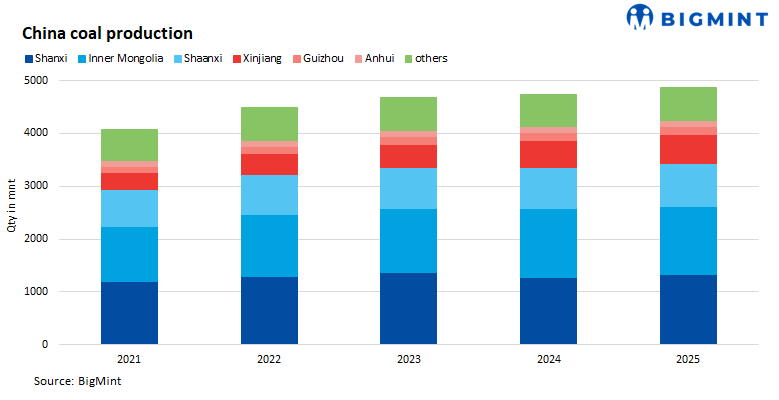

The most important province to watch is Inner Mongolia, whose annual output is broadly comparable to Shanxi’s. Together, Shanxi and Inner Mongolia account for more than half of China’s coal production.

If inspections meaningfully spread to Inner Mongolia, the supply risk effectively doubles.

Shaanxi is equally important because of its large base of private mines, which are often more vulnerable to extended shutdowns following accidents. Historically, private operations have faced stricter scrutiny after fatal incidents, and restart approvals can take significantly longer than for state-owned mines.

This explains why thermal coal prices have responded with urgency. China cannot easily offset a meaningful domestic disruption through imports alone. The scale of domestic coal consumption is simply too large for seaborne markets to provide a complete replacement.

Qinhuangdao sends the first signal

The clearest signal has come from Qinhuangdao.

After plateauing for several sessions, thermal coal prices reportedly moved up by around RMB 10/t to approximately RMB 845/t, reflecting the emergence of an inspection-driven risk premium.

The move is notable because it follows a period of stabilisation. Prices had already firmed earlier in the year, but lacked fresh momentum. The Shanxi accident became the catalyst that revived concerns over supply adequacy heading into peak summer demand.

Why imports cannot fully solve the problem

China can increase coal imports at the margin, but it cannot easily replace domestic production disruptions at scale. Even a modest slowdown in domestic supply can translate into very large tonnage requirements relative to the seaborne market. This explains why mine inspections matter so much to thermal coal pricing. The market is effectively asking whether domestic output growth will remain stable just as seasonal demand strengthens.

This is also why Russia and Indonesia matter. Russian coal exports are increasing and may provide some relief, while Indonesia’s proposed export agency and tighter production controls risk adding uncertainty to regional supply.

The policy dilemma

Beijing now faces a familiar balancing act. A serious accident demands visible enforcement, particularly if safety failures are involved. Yet aggressive inspections ahead of the summer demand season risk tightening power coal supply at precisely the wrong time.

The government’s next move will likely determine whether the recent rally proves temporary or evolves into a more sustained repricing.

Leave a Reply