- Renewables are driving growth, coal share is declining but still critical

- Rising peak demand and volatility signal summer supply risks

India’s power market is undergoing a visible shift as the system moves toward the summer months, with renewable energy now driving most of the incremental increase in generation while coal’s share gradually declines. However, this shift is not translating into greater system flexibility.

As solar output drops in the evening and alternative sources such as gas and liquid fuels remain limited, the burden of meeting peak demand continues to fall on thermal capacity, raising the risk of tighter supply conditions during critical hours.

Renewables drive growth, coal remains indispensable

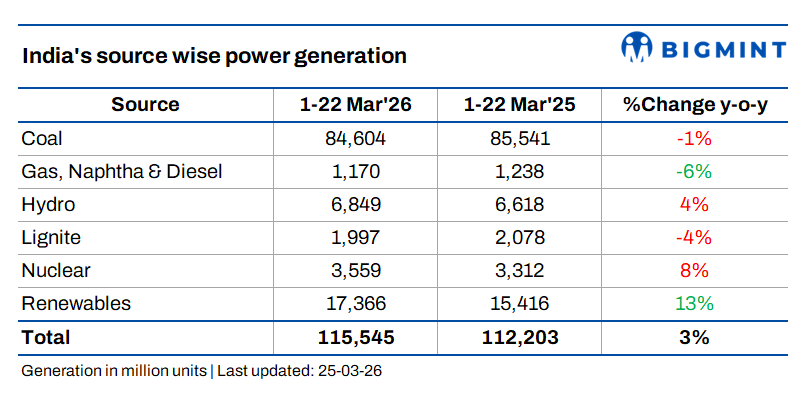

Total generation during March 1-22, 2026 stood at 115,545 MU, up 3% year-on-year from 112,203 MU, indicating modest overall growth. Incremental supply was entirely driven by renewables, which added nearly 2,000 MU over the period and grew 12.7% year-on-year, while nuclear and hydro also recorded moderate increases. In contrast, coal-based generation declined by 1.1% and gas-based generation fell more sharply by 5.5%, reflecting fuel constraints.

This divergence highlights a shift in the quality of supply growth. Incremental generation is coming from sources whose output cannot be adjusted to match demand, while flexible thermal capacity is weakening. The decline in gas-based generation is particularly significant, as it reduces available peaking and balancing capacity at a time when renewable intermittency is rising.

The generation mix has accordingly shifted, with coal’s share declining to 73.2% from 76.2% last year, and renewables increasing to 15% from 13.7%. Despite this, coal remains the primary source of reliable supply and continues to anchor system stability, particularly during peak demand periods.

Demand variability and market signals point to rising stress

Demand trends indicate increasing system stress through variability rather than aggregate growth. Average peak demand for March 1-22 remained broadly flat at around 222 GW, but the maximum peak rose to 238,378 MW from 235,224 MW last year, while the minimum peak declined to 194,118 MW from 199,143 MW. This has widened the demand range by over 8,000 MW year-on-year, increasing the burden on supply during peak periods.

This expanding spread reflects greater volatility in consumption patterns, driven by weather variability and uneven industrial activity. The system is therefore facing sharper peak requirements without corresponding growth in average demand. Greater variability is also increasing reliance on thermal capacity to manage intra-day imbalances, particularly during peak hours.

These pressures are visible in spot market behaviour. Purchase bids increased by 34%, sell bids by 54%, and cleared volumes rose 38%, indicating improved liquidity. While higher supply pushed average prices down 6.7% to INR 3,830/MWh, intra-month price movements remained volatile, with spikes above INR 6,600/MWh followed by a sharp correction to around INR 1,976/MWh.

The combination of higher liquidity and sharp price swings suggests that the system remains sensitive to short-term imbalances, with limited buffer during periods of peak stress.

Outlook

The late-March softening in demand, with average daily generation declining from 5,463 MU during March 8-14 to 5,082 MU in March 15-22, is seasonal and does not indicate a structural easing in system conditions. The decline coincides with improving renewable output and lower seasonal load, temporarily masking underlying tightness in supply.

While hydro generation has supported supply during March, its availability is likely to tighten as water is diverted toward irrigation during peak summer. At the same time, solar output will drop sharply during evening peak hours, and gas-based generation remains structurally constrained. This limits flexible supply precisely when demand peaks.

As a result, we expect coal to remain the primary source of peak supply, with plants operating at higher utilisation levels to meet rising demand during critical hours. The combination of higher peak demand, reduced flexibility, and increasing intra-day variability is likely to tighten supply-demand conditions during peak hours and sustain elevated price volatility through the summer months.

Leave a Reply