- Peak-season cargo demand strengthens across key trade lanes

- Red Sea rerouting continues to tighten vessel capacity

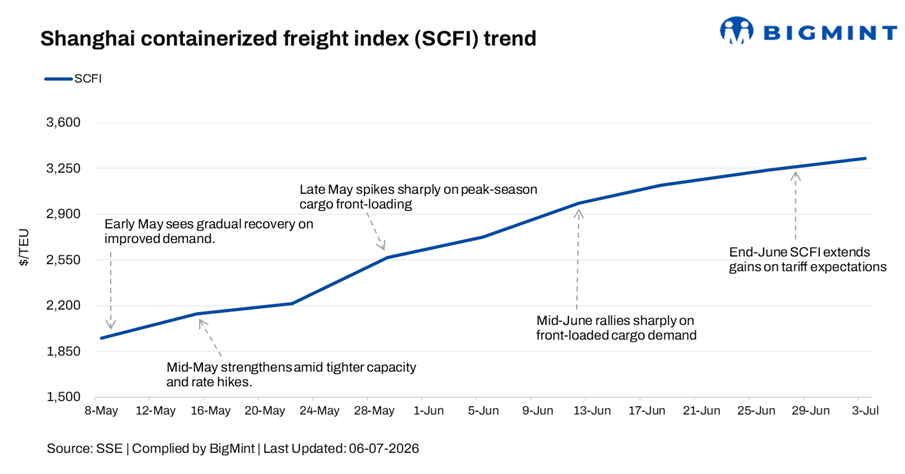

The Shanghai Containerized Freight Index (SCFI) gained 2.7% to $3,326.87/twenty-foot equivalent unit (TEU) on 03 July 2026 as against $3,239.64/TEU on 26 June amid all major east-west trade lanes as seasonal cargo demand strengthened and carriers continued to exercise disciplined capacity management.

Meanwhile, continued vessel diversions around the Red Sea via the Cape of Good Hope kept effective capacity constrained on Europe-bound services, providing additional support to freight levels. Overall, the market remained underpinned by resilient export demand and supply-side discipline despite easing geopolitical concerns.

Trans-Pacific demand remains exceptionally strong, with carriers deploying record container ship capacity on the Asia-US trade. Despite the additional capacity, spot freight rates continue to rise as cargo bookings outpace available space.

Carriers have announced fresh General Rate Increases (GRIs) and Peak Season Surcharges (PSS) for July, anticipating sustained peak-season cargo volumes. Early peak-season shipping has accelerated, with US importers front-loading cargo ahead of tariff changes and seasonal inventory build-up, resulting in stronger export bookings from China and Southeast Asia.

Outlook

Container freight rates are expected to remain firm in the near term as peak-season cargo volumes support demand and carriers continue capacity discipline. However, the pace of further increases will depend on the sustainability of export bookings, success of carrier rate hikes, and developments in Red Sea shipping conditions.

Leave a Reply