- Elevated scrap costs pushed smelters to raise billet offers

- Finished steel demand stayed moderate

Steel prices across South India remained largely stable to firm during the week, supported by higher raw material costs and disciplined supply from producers. Despite moderate downstream demand, controlled availability and firm cost fundamentals helped prevent any major price correction across key segments.

Sponge iron price movement:

Sponge iron prices in the Bellary cluster stayed supported, backed by steady demand from steel manufacturers and improved movement of material. Producers had already secured sufficient bookings in the previous weeks. As a result, no notable sales pressure was observed during the week.

Most sponge iron manufacturers are currently covered with bookings for the next 10-12 days. This forward coverage has helped maintain price stability even as fresh buying interest remained cautious. Limited urgency to sell among producers has further supported prices in the region.

On the cost side, production expenses increased during the week as iron ore pellet and coal prices in southern India edged higher. Fe 63% iron ore pellet prices are currently assessed at around INR 9,700 per tonne ex-Bellary. Elevated input costs continue to provide a strong floor to sponge iron prices, discouraging aggressive price cuts.

Melting scrap sentiments :

In the melting scrap segment, prices in the Chennai region remained slightly supported. The market was underpinned by tight material availability and firm global scrap trends. Domestic scrap supply remained constrained, limiting downside risk despite subdued finished steel demand.

Limited realizations from imported scrap and the absence of fresh import bookings encouraged domestic steelmakers to rely more on locally sourced scrap. This shift resulted in a marginal uptick in domestic scrap prices. Imported HMS 80:20 (Australian origin) is currently hovering around $335 per tonne CFR Chennai, which continues to lend support to the domestic scrap market.

Semi’s and finished steel scenario :

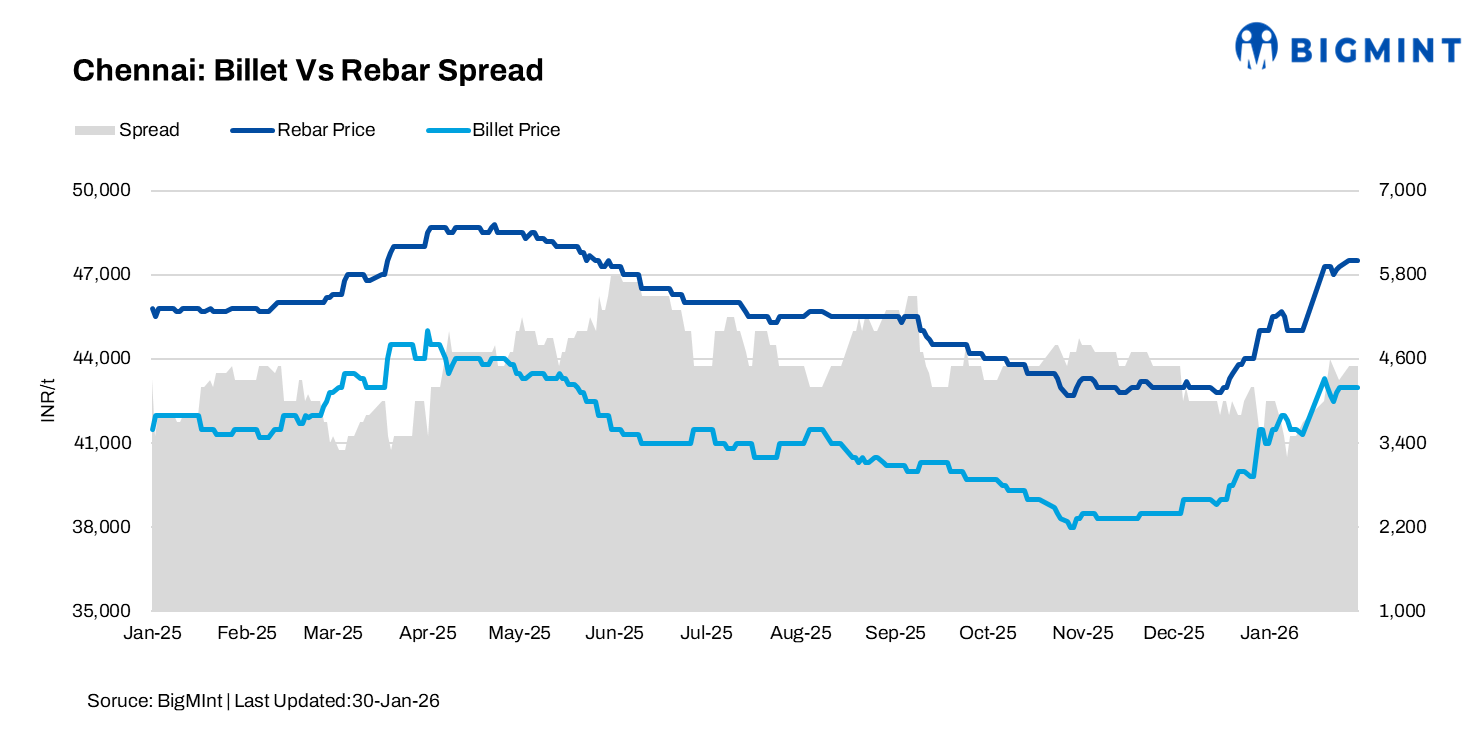

Semi-finished steel prices, particularly MS billets in Hyderabad and Chennai, also remained supported during the week. Material shortages and rising raw material costs, especially higher scrap prices, prompted steel smelters to maintain firm offers. Merchant billet availability in Chennai remained limited due to elevated production costs.

However, finished steel demand in the local market stayed moderate. Steel manufacturers faced challenges in liquidating volumes, while re-rollers continued to operate under margin pressure. High-priced semi-finished inputs, combined with relatively less finished steel realizations, compressed conversion margins and restricted overall market activity.

Market Outlook:

Looking ahead, steel prices are expected to maintain a positive bias in the near term. Market participants anticipate further firmness supported by expected price hikes from blast furnace-route steelmakers. Additionally, optimism surrounding the Union Budget, with expectations of continued focus on infrastructure spending and domestic steel consumption, is likely to support sentiment. Firm raw material costs and improving producer confidence may provide further upside support to steel prices in the coming weeks.

Leave a Reply