- India’s production climbs up 14% on compliance hurdles

- Weak rupee, rising slab arrivals add to import slowdown

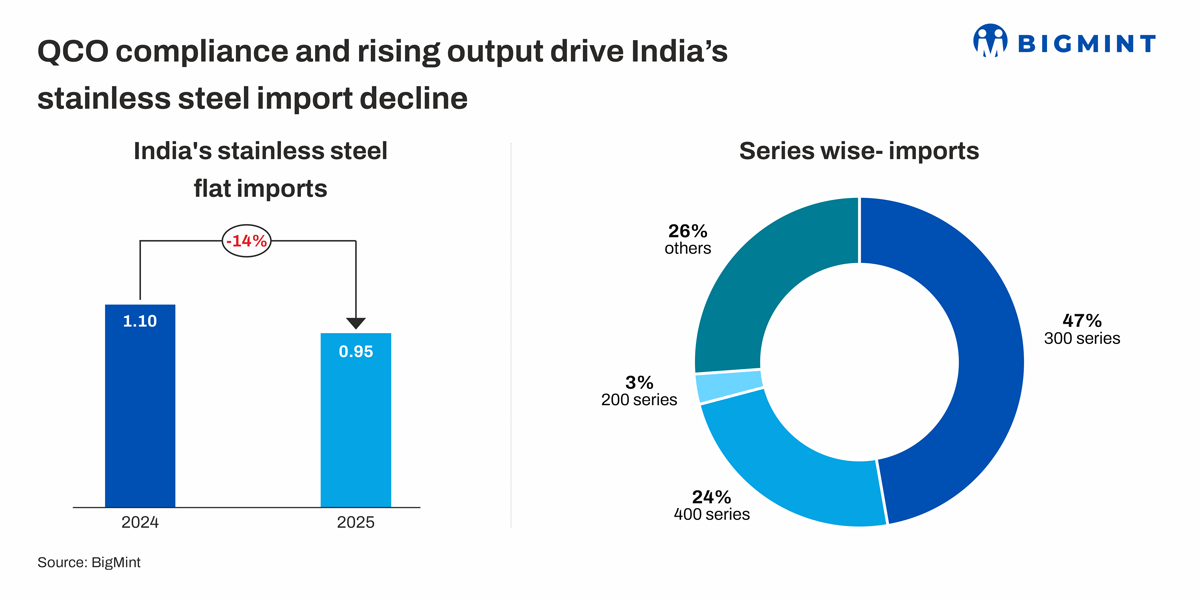

India’s stainless steel finished flat imports declined sharply by 14% y-o-y in CY’25 to around 1 million tonne (mnt), compared with 1.1 mnt in CY’24. The drop was largely driven by a collapse in shipments from China, rising domestic production, and the disruptive impact of Quality Control Orders (QCO) under BIS norms, which altered sourcing patterns across the market.

Series-wise import trends

Imports of 300-series flats slipped 13% y-o-y to 0.45 mnt, while 400-series volumes edged lower by 7% to 0.22 mnt. In contrast, 200-series flats rose sharply by 28% to 30,000 t, supported by demand from cost-sensitive segments. Imports of other special grades declined by nearly 20% as buyers shifted towards standardised and compliant supply sources.

China loses dominance as sourcing shifts

China, traditionally India’s largest stainless steel flat supplier, saw shipments plunge by nearly 57% y-o-y to 0.17 mnt in CY’25 from 0.42 mnt in 2024. This single trend accounted for most of the overall decline in imports.

Meanwhile, Indonesia increased its shipments by 4% to around 0.15 mnt, supported by competitive pricing due to integrated nickel-based production. Japan’s supplies remained steady y-o-y at 75,000 t, as buyers preferred higher-quality and BIS-compliant material.

Factors behind import slowdown

- BIS/QCO compliance reshapes buying behaviour: The rollout of BIS certification under QCO norms (IS 6911, IS 5522, and IS 15997) has structurally changed India’s import market. Although the government extended compliance relaxation until 31 March 2026, documentation hurdles, shipment risks, and longer lead times made overseas sourcing less attractive. As a result, many consumers and traders increasingly favoured domestic mills that offered predictable deliveries and assured quality compliance.

- Domestic production rises 14% y-o-y: India’s finished stainless steel flat output rose 14% y-o-y to 2.95 mnt in CY’25 from 2.59 mnt. Higher capacity utilisation, expanding cold-rolling facilities, and better cost control enabled Indian mills to replace imported material, particularly in the 300-series.

- China’s export regime tightens: From 1 January 2026, China will enforce a mandatory export licensing system for all stainless steel products. Exporters must obtain government approval for each shipment, aimed at curbing under-priced exports and illegal trade. This slowed Chinese export flows towards the year-end and raised supply uncertainty for Indian buyers, accelerating diversification toward Indonesia and Japan.

- Slab imports rise: Stainless steel slab imports rose sharply during the period. India imported 642,000 t of stainless steel slabs in CY’25, up 48% y-o-y from 434,000 t in the same period last year. Indonesia continued to dominate as the leading supplier with 581,000 t volumes recorded, benefiting from competitive pricing and consistent availability.

- Rupee weakens: The Indian rupee depreciated by around 4.7% in 2025, adding to imported cost pressures across the stainless steel value chain. The weaker currency raised the landed cost of key raw materials such as nickel, ferro alloys, and stainless steel flats, reducing the price advantage of imports. This also made overseas purchases riskier amid volatile freight and metal prices, further encouraging mills and traders to rely more on domestic supply.

Price trends

In December 2025, imported 304 hot-rolled coils (HRCs) (3-25 mm) was landing at INR 175,000-176,000/t ($1,947-1,958/t), making it nearly INR 6,000-7,000/t cheaper than domestic prices at around INR 181,000-182,000/t.

BigMint’s assessment placed domestic 304 HRCs at INR 180,000-190,000/t in CY’5 compared to INR 170,000-180,000/t in CY’24. BigMint’s latest assessment on 14 January 2026 placed prices at INR 190,000/t.

Outlook

With domestic capacity continuing to expand, China’s export controls tightening, and BIS compliance becoming the new normal, India’s reliance on imported stainless steel flats is expected to decline structurally in 2026. While short-term volatility may persist due to nickel prices and policy adjustments, the medium-term outlook points towards greater self-sufficiency and disciplined import flows across the Indian stainless steel market.

Leave a Reply