- US Gulf freight surge tightens supply, lifting landed values

- Mediterranean demand steady, India continues to anchor global prices

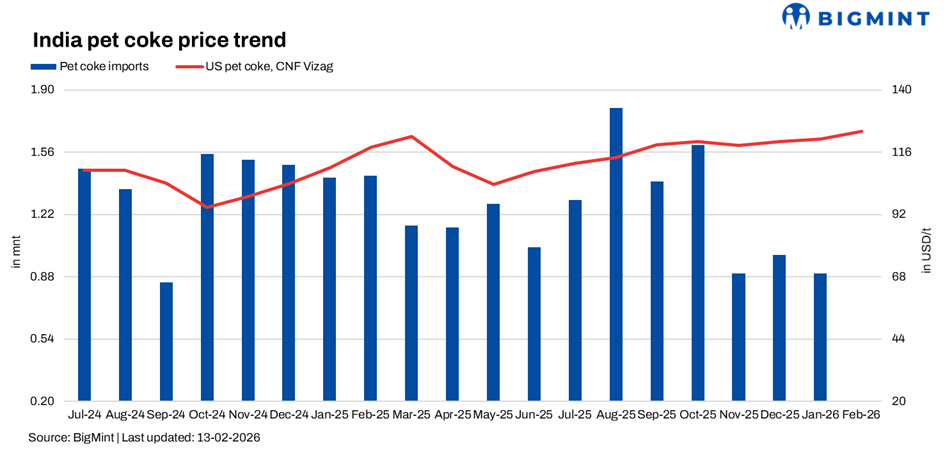

The global petroleum coke market strengthened further in mid-February, led by firm Indian import pricing, rising US freight costs, and steady Mediterranean demand. What began as gradual tightening in late January has now evolved into a replacement-cost-driven structure, with delivered prices into India approaching levels that materially reset the market floor.

While there is no panic buying, the market tone has clearly shifted from negotiation to disciplined firmness.

Delivered prices edge higher across regions

CFR India pricing for 6.5% sulphur US-origin petcoke has consolidated in the $122-125/t range for March loading. Bids have firmed into the $120-122 corridor, narrowing the bid-offer spread compared with earlier weeks.

Saudi-origin high sulphur material (9.5%) is being offered around $121-124/t CFR, in some cases at a premium to US barrels due to prompt delivery positioning.

US Gulf Coast FOB values remain firm across grades:

- 4.5% sulphur: $82-83/t

- 5.5% sulphur: $79-85/t

- 6.5% sulphur: $76-77/t (with prompt vessel trades printing higher)

In the Mediterranean:

- Turkiye is trading 5.5% sulphur in the $108-115 range CIF

- 6.5% sulphur in Turkiye is trading around $106-110

- Egypt is seeing 5.5% sulphur between $108-112

- Brazil is absorbing 6.5% sulphur near $105-108

India remains the premium outlet, pricing roughly $12-15 above Turkiye and Brazil on a delivered basis.

Freight has become a decisive variable. US Gulf to India freight is now in the low-to-mid $50s/t, up sharply due to heavy grain cargo movement competing for Panamax tonnage. This has pushed full replacement economics for some high-NAR cargoes toward the $138-140 CFR mark into west coast India.

Factors impacting prices

1. Freight Inflation

Grain exports out of the US have tightened vessel availability. Freight rates have climbed into the $52-56 /t corridor, significantly higher than January levels. Even if FOB values remain stable, landed costs automatically rise when freight escalates.

Replacement arithmetic now leaves little room for aggressive discounting into India.

2. Stable Indian demand

Cement producers in India continue to prefer imported petcoke over equivalent calorific coal alternatives on a heat-adjusted basis. While offers are viewed as elevated, there has been no material shift away from petcoke in kiln blends.

Domestic coal alternatives, including RB2 and RB3 equivalents, remain competitive but do not fully displace petcoke at current blending ratios. As a result, import demand remains steady rather than speculative.

3. Reduced short exposure

Earlier in the quarter, several traders sold forward cargoes at lower CFR levels, assuming stable freight and easier replacement. With freight rising and FOB values firm, some of those short positions have become difficult to cover.

This has altered market behaviour. Sellers are now less willing to commit forward volumes without firm vessel cover, tightening available prompt supply.

The result is a more disciplined market structure.

India leads, Mediterranean follows

India continues to anchor global pricing. With CFR India at $122-125, Mediterranean destinations remain discounted but firm.

More significantly, at least one large refiner has reportedly offered petcoke at $138/t CFR Kandla. At that level, delivered petcoke economics rise sharply, especially when freight inflation is factored in.

Turkiye’s 5.5% sulphur cargoes are largely clustering around $110-113, while Brazil trades were heard at around $105-108 for 6.5% sulphur. Egypt remains opportunistic but aligned with Turkish parity.

US FOB spreads between sulphur grades remain compressed, reflecting balanced demand across qualities rather than isolated tightness.

Replacement cost will dictate direction

The petcoke market is not experiencing explosive demand growth. Instead, it is adjusting to higher delivered cost inputs.

The key variables to monitor are:

- US Gulf freight rates

- Grain cargo intensity

- Indian cement offtake

- Turkish and Brazilian buying activity

If freight remains above $50 /t, India’s CFR floor is unlikely to fall meaningfully below $120-122. Conversely, a normalization in freight could shave $5-8/t off landed values without altering the underlying demand structure.

For now, the market is firm, orderly, and replacement-cost driven.

Leave a Reply