- Pakistan faces tighter scrap supply as Gulf routes stall

- Local steel prices firm on rising freight and fuel

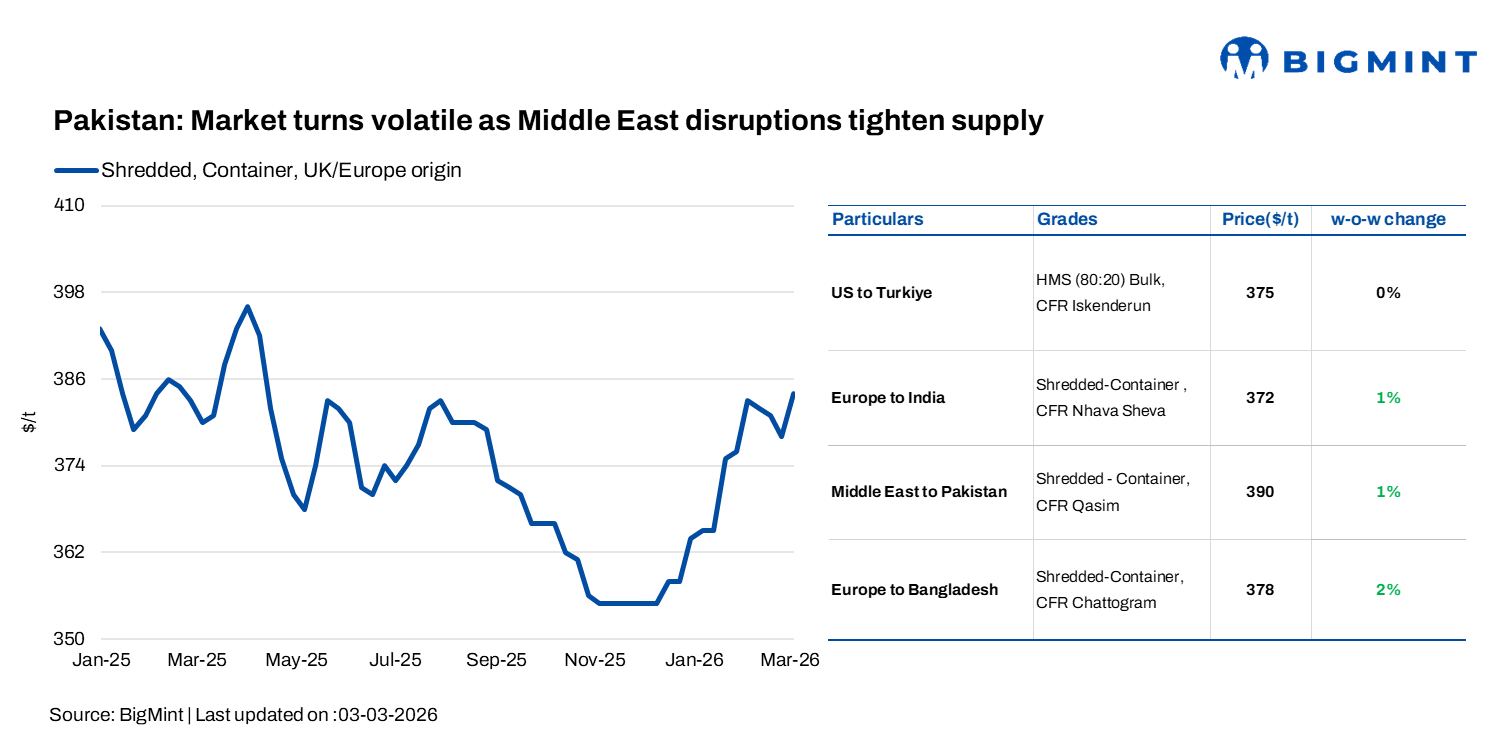

Pakistan’s imported scrap market remained highly volatile on 3 March. EU-origin shredded scrap increased by $5-6/t w-o-w in the week ending 3 March, as escalating Middle East tensions and the US-Iran conflict disrupted vessel movements through the Strait of Hormuz.

Rising bunker costs and port-related uncertainties tightened shredded scrap availability, while no fresh import offers were reported from the United Arab Emirates to Karachi/Qasim ports.

Market comments

UK/EU-origin shredded was heard at $382-388/t CFR, supported by logistical constraints and reduced collection across Europe. With major port movements in the Middle East reportedly seized, and Jebel Ali closed for the past three days, suppliers lifted offers by $5-10/t, anticipating further freight escalation.

The market remained over-cautious as Brent moved into the mid-$70s, pushing bunker fuel prices up 25-35% and forcing vessels to avoid high-risk Gulf routes. Traders warned that a prolonged disruption at Hormuz could raise freight rates 15-25%, embedding an additional risk premium into steel and raw material imports.

As per a trader based in the UAE, “The impact is expected to be more severe for Pakistan, given its heavy reliance on UAE-origin scrap after Europe. Rising instability in Afghanistan is further contributing to market anxiety.”

Domestic market

As per a market participant, domestic steel prices increased by roughly PKR 5,000/t ($18/t) as supply concerns and geopolitical tensions filtered into the local market. Rebar was reported at PKR 226,000-228,000/t ($809-816/t), billets at PKR 195,000-197,000/t ($698-705/t), bala at PKR 178,000-182,000/t ($637-652/t), and local scrap at PKR 138,000-142,000/t ($494-508/t). As per a steelmaker based in Peshawar, “Mill utilisation weakened to 28-30%, with mills operating cautiously amid rising costs, liquidity tightness and limited downstream demand.” Despite soft commercial-grade sales, graded products held steady, though producers remained defensive due to currency pressure and unpredictable import conditions.”

As per a steelmaker based in Peshawar, “Mill utilisation weakened to 28-30%, with mills operating cautiously amid rising costs, liquidity tightness and limited downstream demand.” Despite soft commercial-grade sales, graded products held steady, though producers remained defensive due to currency pressure and unpredictable import conditions.”

Outlook

Market activity is expected to remain subdued over the next 1-2 weeks as war-related supply disruptions, elevated freight, and insurance uncertainty continue to limit visibility. With vessel movements through the Gulf still constrained and bunker costs firm, buyers are likely to restrict fresh bookings and focus only on essential coverage.

Even if post-Eid restocking emerges, procurement will depend heavily on clarity around Hormuz transit and regional energy stability. Any sustained disruption during this period could further tighten scrap availability and keep imported raw material prices elevated, reinforcing a cautious approach among mills already facing liquidity and margin pressures.

Leave a Reply