- Domestic longs stable; liquidity constraints cap aggressive restocking

- Mill utilisation may dip to 25-30% during Ramadan

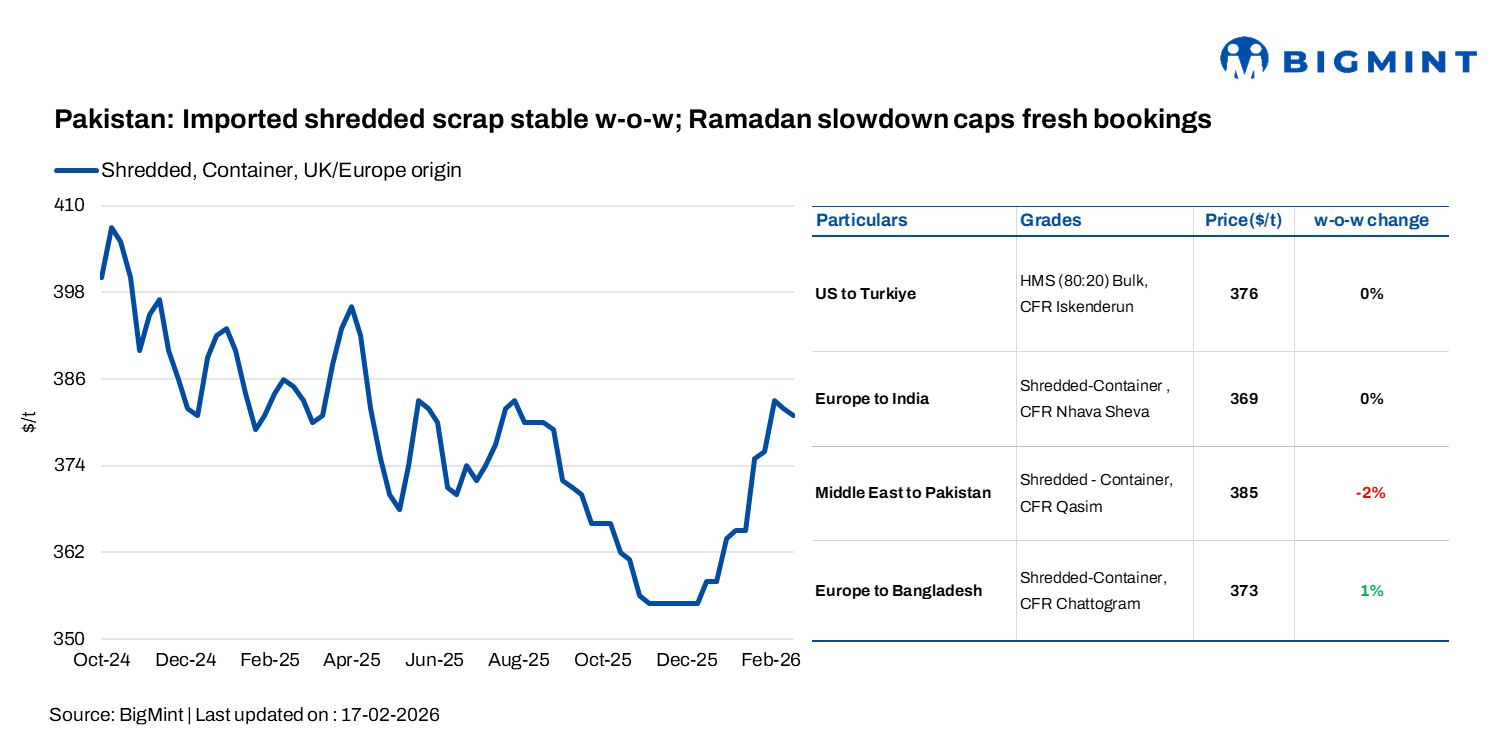

Imported scrap prices remained largely stable w-o-w in the week ended 17 February. Shredded scrap was heard at $380-382/t CFR Qasim, with buyers testing lower bids but failing to secure deals as yard prices and export offers stayed firm on healthy order books. HMS (Middle East origin) held steady at $368-370/t CFR.

EU-origin shredded scrap was assessed at $381/t CFR Qasim, easing marginally by $1/t w-o-w.

Imported scrap buying interest remained weak ahead of Ramadan, with most Pakistani mills refraining from fresh bookings. A major long steel producer based in Peshawar said, “We have not purchased anything from overseas yet. Maybe by Thursday we will consider it.”

Offers were heard at $382/t CFR from the EU and $388-392/t CFR from the UAE for shredded scrap, while mills’ workable levels were significantly lower at $375-378/t for EU origin and $382-383/t for UAE origin.

The market softened amid low buying appetite, as mills largely stayed away from bookings ahead of Ramadan, which is expected to begin mid-week.

A UAE-based trader noted that Pakistan’s recent power tariff reduction of PKR 4.40/unit, translating to roughly a 13-14% cut, may provide some cost relief to local mills.

That said, firm Indian buying at comparatively higher levels is offering regional support.

In the domestic market, rebar prices were heard at PKR 225,000-226,000/t ($804-808/t), while billet traded at PKR 195,000-196,000/t ($697-701/t). Bala scrap was assessed at PKR 188,000-190,000/t ($672-679/t), and local scrap at PKR 138,000-140,000/t ($493-501/t).

Mill capacity utilisation remained low at around 35-38%, reflecting cautious operations. Although commercial-grade rebar had corrected earlier due to liquidity pressures, major listed mills have not announced any significant price revision. With Ramadan starting this week, demand may slow, but lower scrap inflows from the UAE could prevent a sharp fall in steel prices.

Mill capacity utilisation remained low at around 35-38%, reflecting cautious operations. Although commercial-grade rebar had corrected earlier due to liquidity pressures, major listed mills have not announced any significant price revision. With Ramadan starting this week, demand may slow, but lower scrap inflows from the UAE could prevent a sharp fall in steel prices.

Outlook: Based on market feedback, we expect mill utilisation to decline further to around 25-30% during Ramadan. Steel prices may see a mild correction over the next two weeks as construction activity slows and scrap procurement weakens. However, scrap collection constraints on the supply side are likely to limit any sharp downside, keeping the market broadly range-bound in the coming week.

Leave a Reply