- European shredded prices drop $2/t w-o-w

- Mills continue need-based scrap procurement

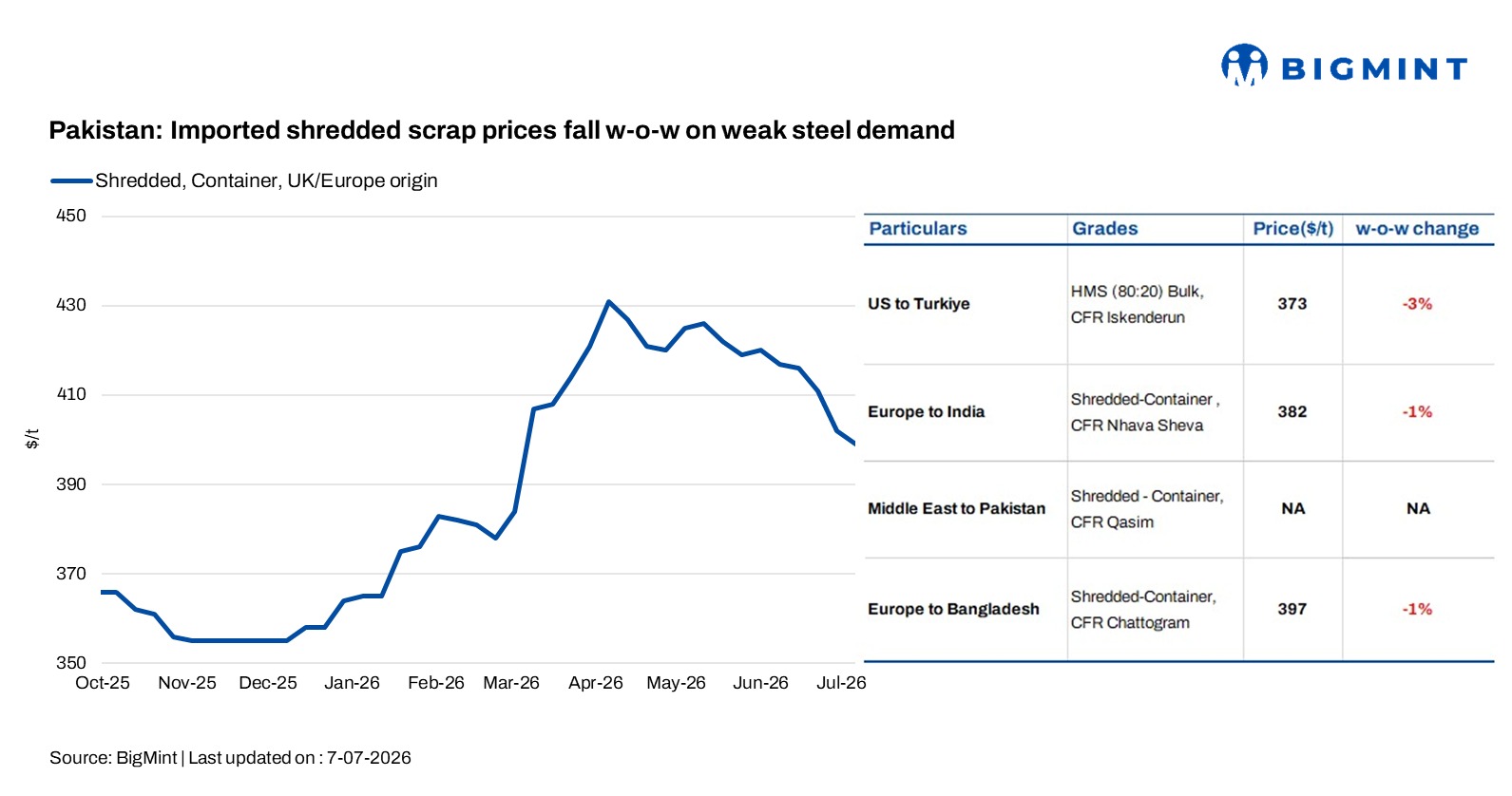

Pakistan’s imported ferrous scrap market remained under pressure during the week ended 7 July as weak domestic steel demand, subdued construction activity, and cautious mill procurement continued to restrict trading activity. Buyers largely stayed on the sidelines, purchasing only for immediate production requirements, while the gap between bids and offers kept fresh deals limited.

BigMint assessed Europe-origin shredded scrap at $399/t CFR Port Qasim, down by around $2/t w-o-w.

Trades during 1-7 July

- UK/EU-origin shredded scrap: 1,000 t booked at $398/t CFR Qasim

- UK/EU-origin HMS 80:20: 1,000 t booked at $390/t CFR Qasim

- UK/EU-origin GI bundles: 1,000 t booked at $390/t CFR Qasim

- UK/EU-origin windmill scrap: 500 t booked at $455/t CFR Qasim

European-origin shredded scrap offers eased to $402-405/t CFR, down from the previous week, while buyers maintained bids at $390-395/t CFR. A few transactions were reported at $400-402/t CFR, although market participants indicated that customers were only willing to conclude deals around $395/t CFR.

Traders noted that several offers remained unsold, including UK/Europe-origin shredded scrap at $399/t CFR for July shipment.

Alternative containerised offers also remained available. Malaysian suppliers offered CR busheling at $425-430/t CFR, LMS at $360/t CFR, and HMS 80:20 at $390/t CFR Port Qasim. Market participants added that these offers generated only limited buying interest as mills continued to delay purchases.

Meanwhile, Middle East-origin scrap availability remained limited at around 15% of normal volumes, though supply has started to improve gradually.

Regional sentiment remained subdued, with buyers maintaining workable levels near $395/t CFR for UK/EU-origin shredded scrap, while mills continued to resist higher offers.

A trader commented, “There is a little bit of activity with some small trades, but the market remains very slow. Demand is entirely need-based and buyers are only comfortable at around $395/t CFR.”

The domestic steel market remained under pressure, with local scrap at PKR 144,000-148,000/t, billet at PKR 205,000-210,000/t and rebar at PKR 235,000-238,000/t. Steelmakers continued operating at only 35-40% capacity utilisation amid weak construction activity and subdued finished steel demand.

Market participants said the FY27 tax and regulatory changes have created uncertainty, particularly among steel buyers and rerollers in Gujranwala, with the market expected to take another 10-15 days to adjust to the new framework.

The uncertainty is also expected to affect production. Industry sources indicated that several steelmakers are evaluating temporary shutdowns or production cuts while assessing the financial impact of the revised tax structure.

Outlook

Pakistan’s imported scrap market is expected to remain subdued, with mills likely to continue need-based procurement amid weak long steel demand and low capacity utilisation. Buyers are expected to keep bids below $395/t CFR, while uncertainty over new tax regulations may further weigh on production and scrap demand.

Leave a Reply