- Mills buying selectively; hand-to-mouth procurement continues

- Trader offers seen ahead of workable mill levels

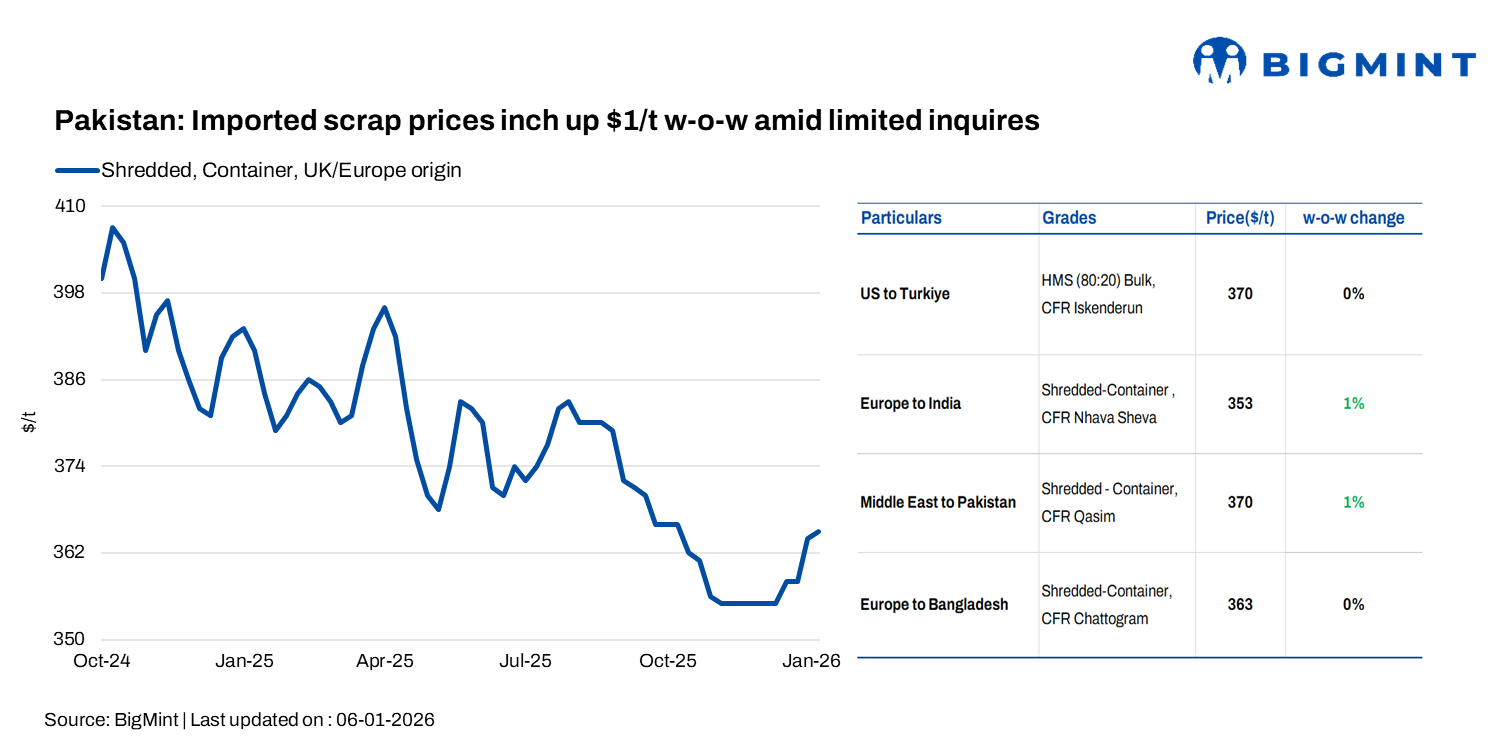

Pakistan’s imported shredded scrap prices inched up by $1/t w-o-w to $365/t CFR for the week ended 6 January. Current offers for EU shredded scrap are being quoted as high as $365/t, with reports of deals around $360/t, though these are viewed with caution and not fully credible.

As per Europe-based scrap suppliers, current offers from Europe and the UK are in the $366-368/t CFR range, while workable levels are seen at $362-364/t. Market sources also indicated that four to five deals were booked at around $362-366/t CFR Qasim

Market comments

As per a mill-side source, current indicative prices in Pakistan stand at around PKR 130,000/t ($465/t) for local scrap, PKR 184,000-185,000/t ($657-661/t) for billet, PKR 218,000-220,000/t ($778-785/t) for rebar, and PKR 175,000-178,000/t ($625-636/t) for bala. Mill utilisation remains low at around 38-40%. Despite subdued operating rates, some traders are still offering imported scrap at $360-362/t CFR, although mills remain cautious and selective in fresh bookings given ongoing margin pressure.

“We recently booked around 4,000-5,000 tonnes of scrap from the UAE, with shredded at $370/t CFR Qasim and sheared HMS at $345/t. The market tone is slightly positive at the moment, supported by renewed buying from Turkiye and relatively high domestic scrap prices in the UAE, which are keeping exporters firm. Given current replacement costs, sellers are not under pressure to reduce prices, and downside appears limited in the near term.” A Karachi-based steel mill.

Gadani remains sluggish despite potential opportunities from Bangladesh’s slowdown. Local bids are still below $400/LDT, and activity through December and early January has been muted, with anchorage levels low. While yards are upgrading for HKC compliance, limited compliant capacity continues to constrain demand. Stable steel plate prices, a slightly weaker rupee, and easing inflation offer marginal support, but India is expected to absorb most near-term tonnage.

Outlook

Near-term sentiment is cautious but stable. Limited availability may support prices briefly, but weak steel demand and liquidity stress should cap upside. The source expects prices to ease after 25 January, as current firmness is driven by year-end supply tightness.

Leave a Reply