- Importers negotiate lower prices in sluggish market

- Discounts offered on rebar list prices amid slow demand

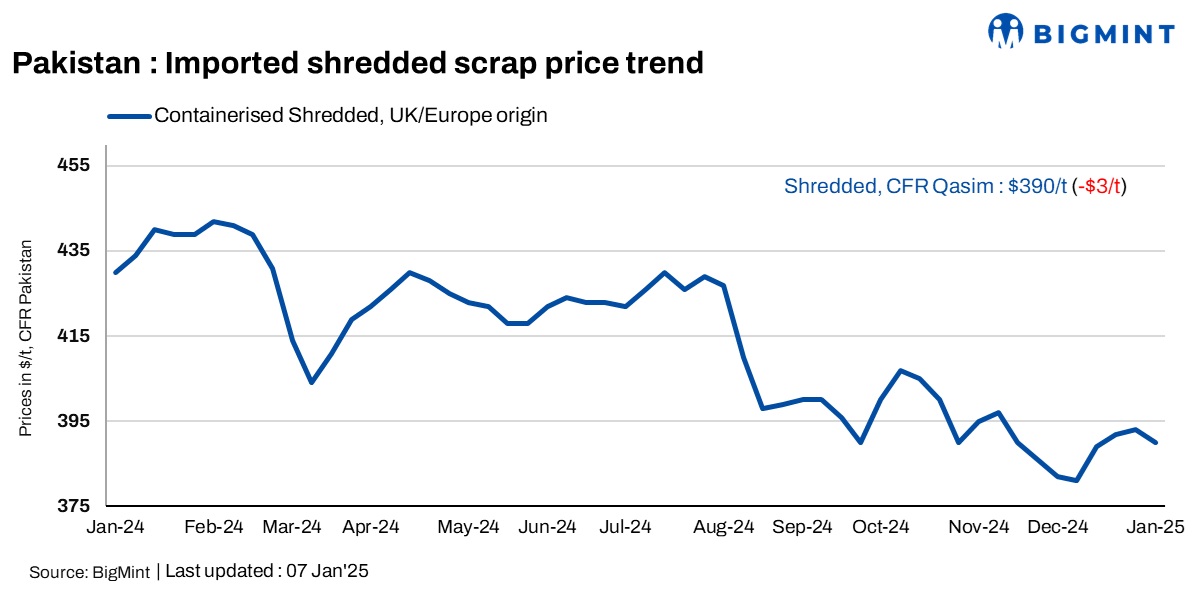

Pakistan’s imported ferrous scrap market began CY’25 on a sluggish note, with limited supplier activity. As market players gradually returned to the market, offers remained scarce, while buyer interest was subdued, with some attempting to negotiate even lower prices.

Amid a sluggish market, manufacturers offered discounts on rebar list prices to attract buyers.

BigMint’s weekly assessment revealed that European shredded was at $390/tonne (t) CFR Qasim, reflecting a slight decline of $3/t w-o-w.

Market comments

A source from a Lahore-based steel mill stated that they expect the market to hover at around $395/t, though suppliers may push offers up to $400/t this week. “Every year, following the New Year holidays, buying typically sees a surge during the first 20 days, leading to a price mark-up. However, prices tend to ease after this period. Let us see if the trend holds true this time,” he noted.

A source from a Karachi-based steel mill said, “Activity has improved, and if sustained, rates are likely to rise further. We have increased rebar prices by PKR 3,000-4,000/t ($11-14/t), in the wake of an improved market. Currently, scrap is at PKR 139,000-142,000/t ($498-508/t), billets at PKR 205,000-208,000/t ($735-747/t), and rebars at PKR 240,000-245,000/t ($861-879/t). Demand is steady, and the seasonal scrap shortage during winter, coupled with lower production levels, has provided support to the market.”

Another market participant observed, “The rise in rebar tags is more of an adjustment on list prices and does not reflect the reality of the market. Actual transaction prices are lower, with discounts of PKR 2,000-3,000/t being offered on the advertised rates.”

According to a trading house representative, shredded was heard at around $390/t a few days back. Overall, the market remained slow, with only a slight increase in finished prices, which had minimal impact on sales. Demand for finished products continued to be sluggish. UAE-origin HMS was traded at $368-370/t, while shredded was priced at $392-395/t CFR.

European recyclers continued to increase their offers to Asian markets, particularly India and Pakistan. Shredded prices from UK and EU yards remained steady at GBP 250-255/t ($310-320/t) ex and Euro 300-310/t ($315-325/t). Container freights from the UK to Pakistan ranged within $45-50/t ($1,480-1,500 per container), bringing the total to $388-390/t CFR.

Meanwhile, Pakistani buyers are negotiating lower levels, with their purchase prices estimated at GBP 245-248/t ($308-312/t) exw and Euro 295-300/t ($310-315/t), translating to $385-388/t CFR.

Steel mills operated at reduced capacity this week, at approximately 45-50% of maximum levels, with no indications of a sales recovery in the near term.

Meanwhile, the IMF has demanded that Pakistan disconnect the gas supply to industrial captive power plants (CPPs) by January 2025 as part of the $7-billion Extended Fund Facility agreement. The decision aims to eliminate the cost advantage CPPs have over grid electricity. The move is necessary for Pakistan to receive the second $1-billion tranche in March 2025. However, industrial stakeholders, particularly textile exporters, opposed the decision, citing the loss of export competitiveness and the potential use of alternative fuels such as coal. While the IMF suggested imposing a hefty levy on gas supply to CPPs, this was considered unfeasible by industrial units. Despite protests, the IMF’s demand for gas disconnection remained unchanged.

Outlook

The market is expected to remain range-bound in the near term, with a slight increase to around $392-396/t CFR. Post-holiday buying typically causes a short-term price surge in the first two to three weeks, but prices usually ease afterward. Limited trading volumes and ongoing seasonal factors will likely keep market sentiment subdued, with prices stabilising in the near term.

Leave a Reply