In Pakistan, market activity remained comparatively slow in terms of fresh imported scrap bookings amid weaker domestic rebar sales followed by liquidity issues for imported scrap buyers. Shredded scrap offers from Europe and the Middle East ranged between $430-438/t CFR Qasim.

Current rates for US/Europe origin shredded stand at $430-434/t CFR Qasim, while HMS from the UAE is offered at $415-418/t.

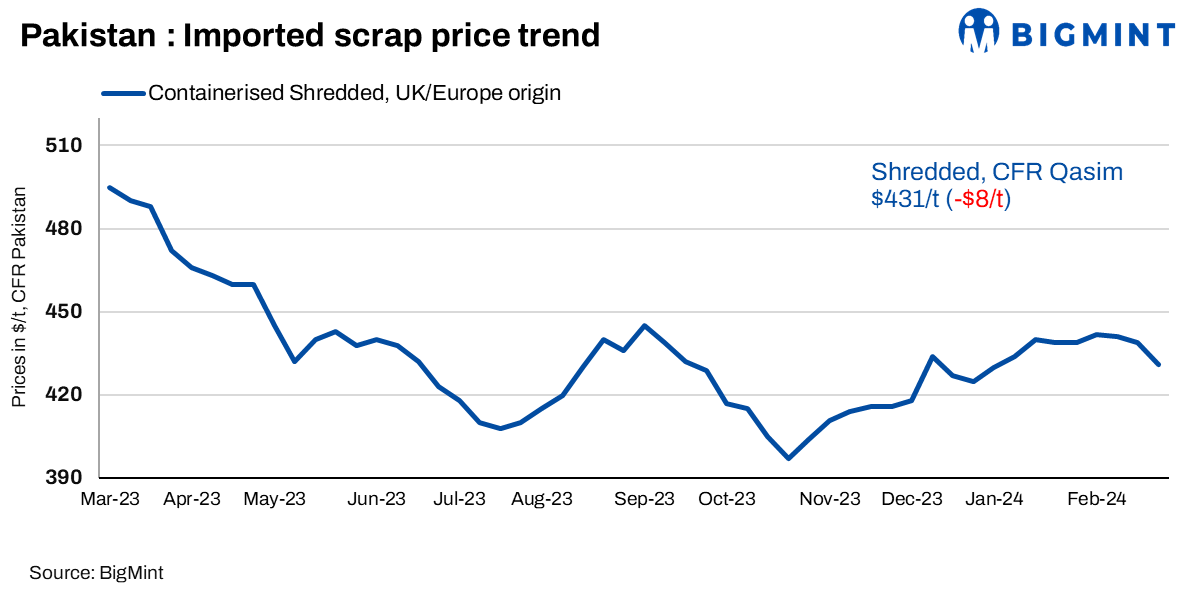

BigMint’s assessment for European-origin shredded stood at $431/t, sharply dropped by 8/t w-o-w.

A trader source mentioned, “Shredded offers have dropped by almost $8-10/t; currently, we are getting $430/t from the UK and Europe and specific yards are around 432-33, sellers are also facing pressure now as last week no major buying was reported.”

As per a mill-side source, “Pakistani buyers are facing a sluggish finished steel market, so delaying bookings in anticipation of improved output. Continued slow buying is anticipated due to extended utility bill liabilities and liquidity concerns among customers.”

As per another mill source, “Market remained slow as people are waiting for the steady formation of the government since this is assembly week and all sales would be on the bill, so it’s slow and payments are also slow.”

Recent deals:

- Around 1,000 t of PNS from UAE sold at $420/t on a CFR Qasim basis

- Approximately 4,000 t of shredded from Europe were booked at $435/t on a CFR Qasim basis.

- Around 1,000 t UK origin shredded were sold at $438/t on a CFR Qasim basis.

- Nearly 1,000 t of shredded from Europe was booked at $440/t CFR Qasim basis.

Domestic market: In the domestic market, local scrap offers and indicatives were reported at PKR 165,000-168,000/t ($596-607/t) on an exw-Punjab basis, respectively. Similarly, rebar offers were heard at PKR 263,000-265,000/t($950-958/t) on an exw basis, whereas billet offers were heard at PKR 230,000-232,000/t($831-838/t) on an exw basis.

Moody’s Investors Service maintained Pakistan’s credit rating with a stable outlook but suggested a potential upgrade if liquidity and external vulnerability risks decrease substantially. The agency cited Pakistan’s high external financing needs and political uncertainty as key challenges. While the caretaker government stabilised the economy and secured IMF financing, concerns remain about future funding sources post-April 2024. Moody’s emphasised the importance of continued IMF engagement in reducing default risks. The rating could improve with increased reserves and fiscal consolidation, but it may downgrade if debt obligations default. Political instability may hinder negotiations for a new IMF programme.

Pakistan’s CPI-based inflation is projected to decline to 23.5% y-o-y in February from 28.3% in January, according to a local research centre. Core inflation is expected to decrease to 18.6% y-o-y. The m-o-m increase is forecasted at 0.4%, primarily due to rises in transport and housing indices.

Currency rate: In the open market, the PKR gained against the USD but lost against the Euro, while remaining steady against the UAE Dirham and Saudi Riyal. The Pakistani rupee marginally declined by 0.03% against the US dollar in the inter-bank market, settling at 279.28, as per the State Bank of Pakistan.

Outlook: The formation of the government later this week could potentially boost market sentiment and provide a positive outlook. Imported ferrous scrap prices are expected to remain range-bound in the near term.