- Pakistan scrap imports rebound despite severe industry pressure

- High freight and energy costs weaken import sentiment

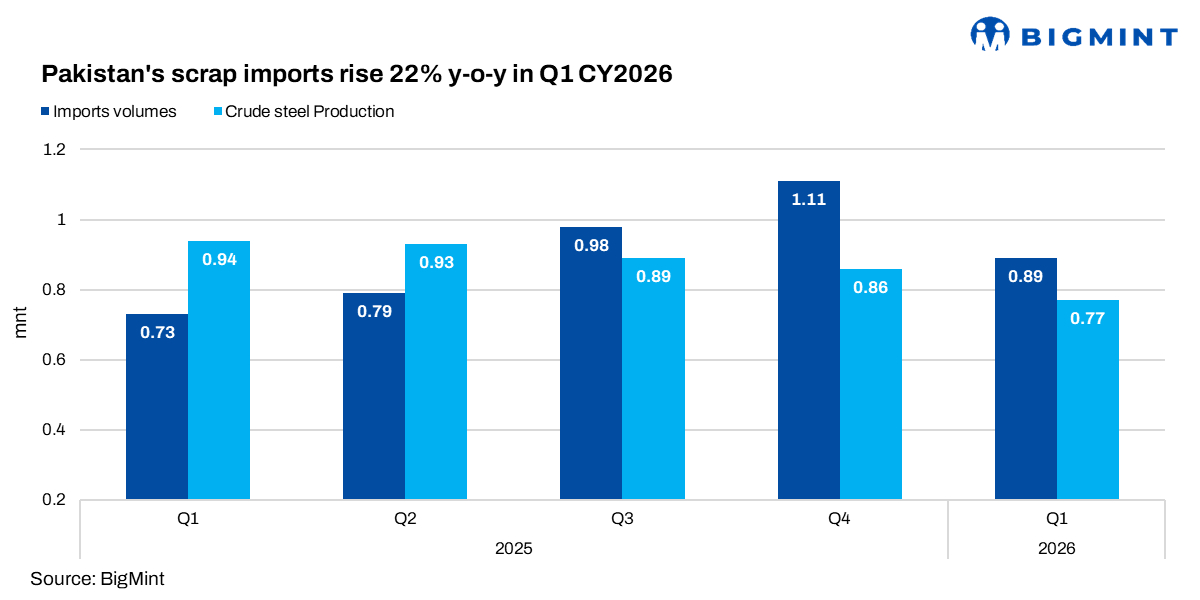

Pakistan’s ferrous scrap imports registered a 22% y-o-y increase in Q1 CY2026 to 0.89 million tonnes (mnt), compared with 0.73 mnt in Q1 CY2025, according to BigMint analysis. However, imports declined sharply by 20% q-o-q from 1.11 mnt in Q4 CY2025, highlighting continued weakness in the country’s steel sector amid mounting structural and economic pressures. March 2026 imports alone dropped by 28% m-o-m to 0.21 mnt.

Steel production in Q1 CY2026

Crude steel production during Q1 CY2026 fell 17% y-o-y to 0.78 mnt and was also down 9% q-o-q, reflecting persistent margin pressure across the industry. Despite an installed steelmaking capacity of nearly 9 mnt, actual output remained limited to around 3.8 mnt annually, with several mills shut and others operating at only 30-50% utilisation rates.

Price trend during Q1 CY2026

Imported shredded scrap prices remained relatively firm during the quarter despite weak buying activity in Pakistan. UK-origin shredded scrap averaged around $386/t CFR in Q1 CY2026, compared with $358/t CFR during the same period last year and nearly unchanged from Q4 CY2025 levels.

Why are imports under pressure?

Market participants noted that, “Pakistan’s imported scrap market continues facing pressure from weak steel demand, elevated energy costs, excessive taxation, rising freight expenses, and tighter monetary conditions. Lower industrial activity and high electricity tariffs have significantly reduced mills’ appetite for imported scrap cargoes.”

Scrap prices and freight costs remain key concern: Imported scrap procurement became increasingly difficult during the quarter due to elevated freight costs and war-related shipping disruptions. Container freight rates from the UK and Europe reportedly surged by nearly $300/container in March 2026, amid Middle East conflict-related rerouting and vessel shortages.

As a result, effective landed costs for imported shredded scrap increased by an estimated $15-25/t. Freight inflation and vessel constraints continued to weaken import sentiment across the market.

Outlook

Pakistan’s imported ferrous scrap market is expected to remain cautious in Q2 CY2026 amid continued pressure from weak downstream steel demand, elevated freight costs, currency volatility, and high financing expenses. Market participants expect imports to remain largely rangebound at around 0.80-0.90 mnt during the quarter, while shredded scrap prices may stabilise near $385-400/t CFR if freight conditions partially ease. Additionally, if higher interest rates persist following the State Bank of Pakistan’s policy rate hike, borrowing costs could further restrict scrap procurement activity and increase margin pressure on steelmakers.

Leave a Reply