- Scrap imports increase despite soft steel demand

- Tight margins keep mills at low capacity utilisation

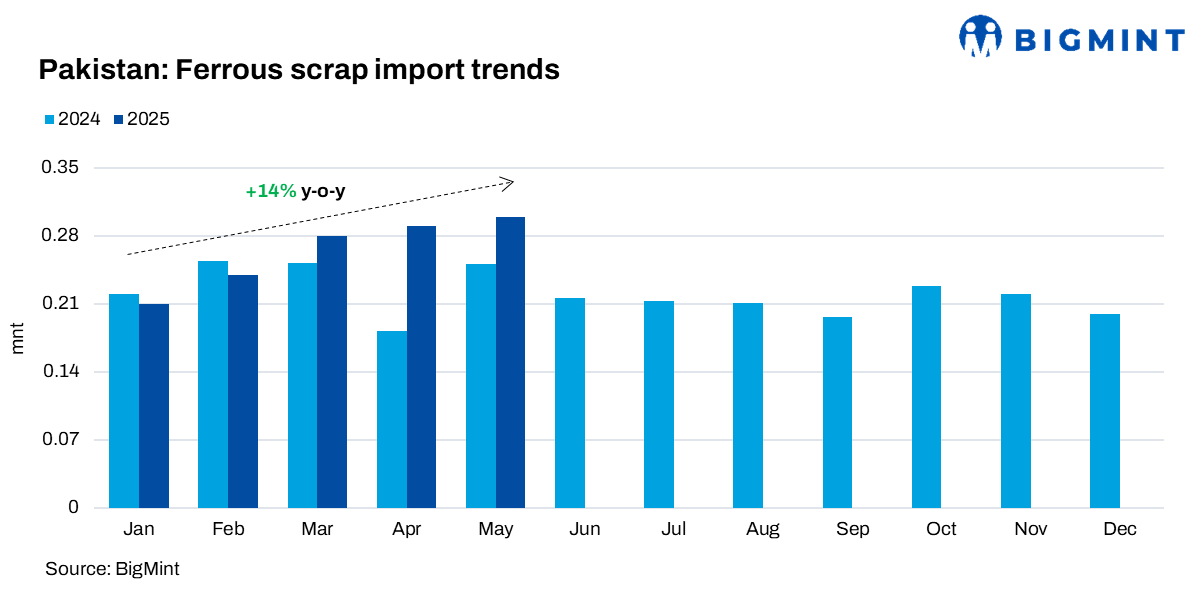

Pakistan’s ferrous scrap imports rose by 14% to 1.33 million tonnes (mnt) during the first five months of CY’25 (5MCY’25) compared to 1.17 mnt in the same period of CY’24.

In May alone, imports reached 304,060 tonnes (t), reflecting a 4% increase from 292,630 t in April. On a y-o-y basis, May imports were up 20% from 253,216 t recorded in May 2024.

It is noteworthy that this uptick in scrap imports occurred despite sluggish domestic steel demand. A key driver was the price differential between India and Pakistan. While shredded scrap prices in India averaged lower at $377/t in 5MCY’25, Pakistan’s average price was higher at $383/t during the same period. This price gap incentivised sellers to divert more scrap shipments toward Pakistan, where they could secure better margins.

Average scrap prices

Pakistan: The average price of UK-origin shredded scrap in 5MCY’25 stood at $383/t, down $24/t from $407/t in 5MCY’24.

India: The average price of UK-origin shredded scrap was $377/t in 5MCY’25, reflecting a steeper drop of $40/t compared to $417/t in 5MCY’24.

The higher average scrap price in Pakistan relative to India made it an attractive destination for exporters seeking better returns.

Moreover, seasonal trends also played a role. In Turkiye, average HMS 80:20 prices stood at around $377/t prior to Eid in March but fell sharply by $20-25/t during the festive period. Pakistan mirrored this trend, with mills stepping up scrap procurement ahead of Eid for restocking, then continuing to maintain higher import volumes afterwards to ensure supply stability amid market volatility.

EU, UAE remain top exporters

Europe and the UAE remained the leading sources of Pakistan’s ferrous scrap imports in 5MCY’25.

Shredded scrap from the UAE continued to flow steadily into Pakistan, thanks to its short four-to-five-day transit time, ensuring consistent supply despite the weak demand environment.

A UK-based market participant noted, “Construction activity picks up during Ramadan as contractors rush to complete projects before labourers go on holiday. Mid-Ramadan often brings some steel demand, and typically, restocking happens during this period, contributing to higher scrap imports.”

Outlook

Pakistan’s steel market continues to face headwinds from weak finished steel demand and tight profit margins. Operating rates remain low as mills grapple with subdued demand, thin margins for billets and rebars, and additional pressure from recent geopolitical tensions.

The industry’s short-term outlook depends on policy clarity regarding scrap import duties and a potential revival in construction and infrastructure activity. Mills are expected to maintain cautious buying strategies unless there is a sustained uptick in steel consumption.

Leave a Reply