- Market sees need-based buying amid high offers

- Pellet tags inch up w-o-w, billet continues to fall

Indian iron ore prices in Odisha remained firm this week, supported by tight material availability and limited offers from miners. Miners highlighted that monsoon-related operational disruptions tightened supply available for the merchant market, while a weak steel sector exerted pressure on prices.

Price update

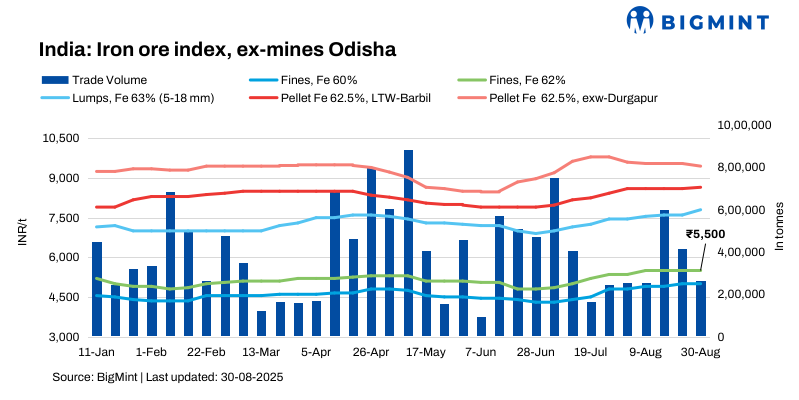

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,500/tonne (t) ($62.5/t) ex-mines on 30 August 2025. Deals for around 260,000 t were recorded by BigMint in Odisha, with steelmakers procuring smaller volumes.

Notably, prices of high-grade iron ore have remained firm since the second half of June 2025, despite a drop in other downstream steel products.

Market highlights

A trader observed, “Production is yet to normalise due to heavy rains, and dispatches remain irregular. Miners have very limited stock, which is keeping prices elevated.”

While the raw material market has remained firm, the downstream steel sector has faced a sharp correction. Sponge iron and semi-finished steel prices have dropped significantly in recent weeks, making buyers increasingly cautious about procuring iron ore at higher costs. Despite this, need-based buying has continued, with steelmakers sourcing material wherever possible.

A steelmaker said, “Steel prices are falling, but iron ore tags are not declining in the same proportion. Still, mills cannot afford to stop operations, so they are picking up material in smaller volumes.”

Adding to the tightness, miners in Odisha were already booked for the coming weeks and were reportedly not entertaining new bulk orders. Regular buyers were being prioritised, with miners quoting higher offers despite concerns about steel margins.

“The cost mismatch is widening. Current ore prices do not align with steel tags, but the prevailing material scarcity has left buyers with little choice,” another market participant said.

Furthermore, a few miners are expected to revise their offers for September deliveries, while upcoming bulk auctions may provide some relief and improve market liquidity. However, given the ongoing supply constraints, market sources expect iron ore prices in Odisha to remain firm in the near term, with only need-based deals likely to dominate the market.

Factors affecting iron ore prices

Pellet offers inch up w-o-w: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil rose by INR 100/t ($1/t) w-o-w to INR 8,700/t ($99/t) loaded to wagon. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur inched down by INR 50/t ($1/t) w-o-w to INR 9,450/t ($107/t) exw on 29 August.

Sponge iron prices drop w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela fell by INR 200/t ($2/t) w-o-w to INR 25,600/t ($291/t) on 30 August.

Billet prices decline w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela fell by INR 500/t ($6/t) w-o-w to INR 36,200/t ($411/t) today.

Rationale

- T1- Three (3) deals for Fe62% fines were recorded in the publishing window, and all were considered for price computation. These were given 50% weightage for index calculation.

- T2 – BigMint received twenty-four (24) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Twenty-two (22) were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Outlook

According to BigMint’s analysis, Odisha iron ore prices will remain supported in the upcoming days, with mixed market dynamics expected in steel tags.

Leave a Reply