- Nickel prices likely range-bound through 2026

- Indonesia NPI capacity expansion sustains global surplus

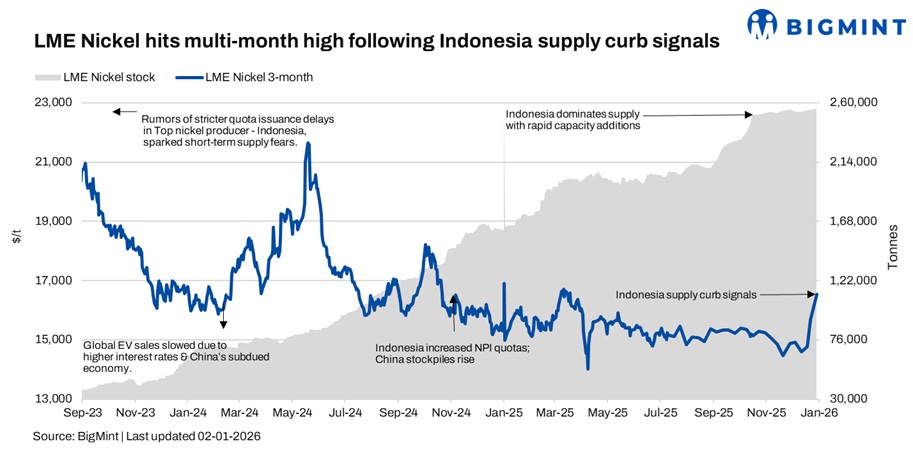

The global nickel market is entering 2026 amid mixed signals. While prices have firmed recently on expectations of tighter Indonesian supply, broader industry forecasts continue to point toward a structural surplus that could cap sustained upside. Nickel futures were assessed at $16,765/t in the week ended 2 January, up nearly 7% w-o-w, largely supported by policy-driven sentiment rather than a fundamental shift in demand.

The key question heading into 2026 remains whether global nickel supply and demand can move closer to balance.

Indonesia policy signals add uncertainty

Indonesia is considering reducing its 2026 nickel ore production quota to around 250 million wet metric tonnes (WMT), sharply lower than the 379 million WMT target set for 2025. While these discussions have lifted near-term price sentiment, market participants note that final quota clarity may take time, and implementation risks remain elevated. Until confirmed, the proposed cuts are viewed as sentiment-supportive rather than a definitive tightening of supply.

NPI expansion keeps surplus intact

Despite policy discussions, Indonesia’s nickel surplus continues to be underpinned by rapid capacity expansion in nickel pig iron (NPI) and intermediate products, led largely by Chinese-backed producers. Industrial hubs such as Morowali and Weda Bay continue to see incremental additions and optimisation of existing smelter capacity. Even as the pace of new project announcements slows, high utilisation rates and incremental expansions are sustaining ample nickel unit availability, reinforcing a structurally oversupplied market.

Banks flag limited upside under surplus conditions

Major financial institutions remain cautious on nickel’s medium-term outlook:

- The World Bank forecasts nickel prices at around $15,500/t in 2026, rising modestly to $16,000/t in 2027.

- Goldman Sachs highlights Indonesian producer margins as the key swing factor and projects prices falling toward $14,500/t by end-2026.

- Nornickel estimates a refined nickel surplus of around 275,000 t in 2026, reinforcing expectations of ongoing pressure.

- ING expects nickel prices to remain range-bound, constrained by elevated inventories and subdued demand, with average prices projected at $15,250/t in 2026.

- ING Research estimates a surplus of around 261,000 t in 2026, broadly in line with 2025 levels, driven largely by Indonesia’s expanding NPI and intermediate output.

Outlook

While Indonesia’s policy discussions have injected volatility and short-term support into nickel prices, the broader outlook for 2026 remains shaped by structural oversupply. Unless supply growth slows materially or demand from stainless steel and battery sectors accelerates beyond expectations, nickel prices are likely to remain range-bound, with upside capped rather than entering a sustained upcycle.

Leave a Reply