- Mid-November demand lift created V-shaped rebound

- Mills to begin pre-holiday ore restocking soon

Mysteel Global:With iron ore shipments expected to rise markedly near year’s end, imported iron ore supply in China will increase further in December with a marked rise in carrier arrivals, while demand for the steelmaking material is set to cool amid production cuts at steel mills, Mysteel predicts in its latest monthly report on the commodity.

Although weakening fundamentals may pressure iron ore prices, the report notes that positive macro-economic signals and anticipated restocking demand among steelmakers will lend some support. Consequently, prices will fluctuate within a wider band this month rather than relentlessly tracking south, the report concluded.

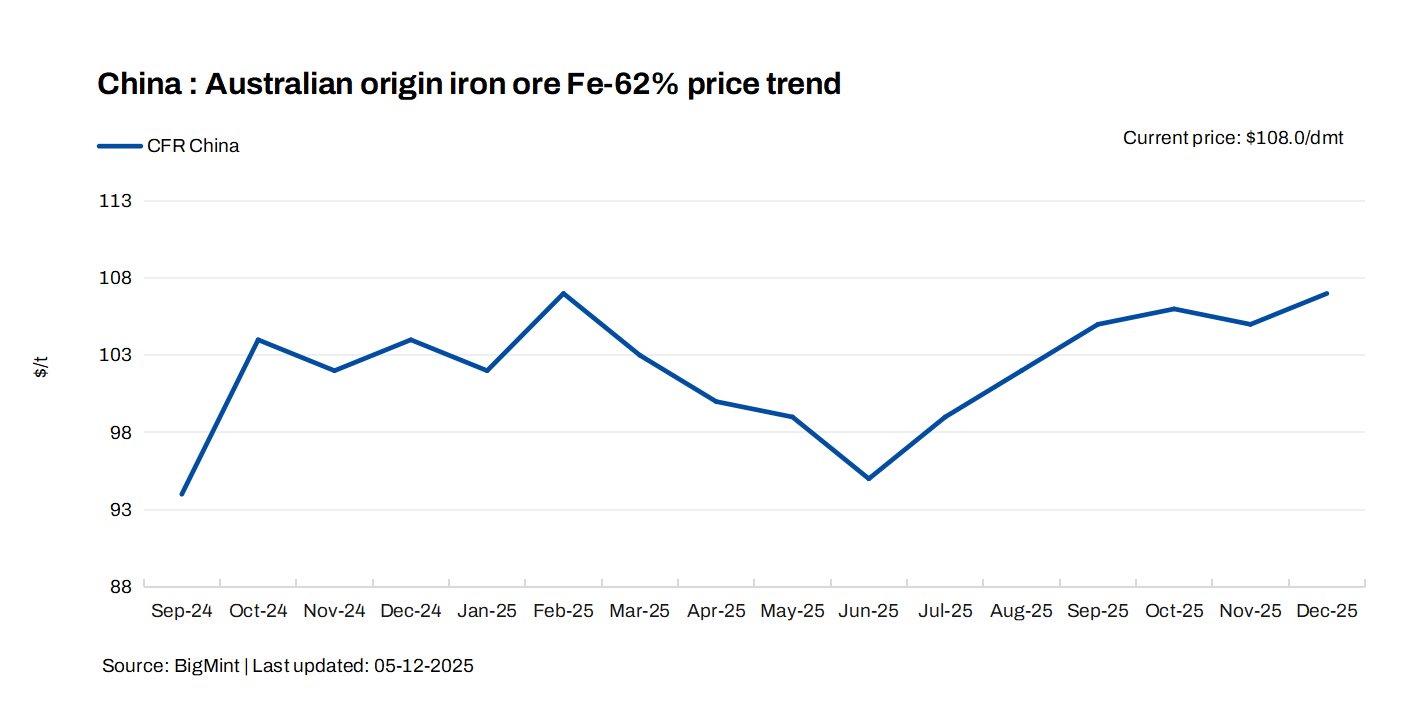

In November, Mysteel SEADEX 62% Australian Fines index averaged $103.76/dmt CFR Qingdao, lower by $1.01/dmt from October’s average. The drop was largely due to ample supply driven by robust global ore shipments, the report suggests.

Daily global iron ore shipments during November rose by 0.4% on month or 7.3% on year to 4.71 million tonnes/day, Mysteel’s tracking showed. As the world’s largest iron ore buyer, China also saw inventories of imported ore at the 45 major ports monitored by Mysteel grow by 4.6% on month to 152.1 million tonnes by November 27.

However, the decline in prices last month was contained, as demand – albeit weak in general – picked up around mid-November after production curbs on steelmakers in many northern cities had been removed, as reported. This contributed to a rebound in ore prices late last month, forming a V-shaped the price trend throughout November.

Looking ahead to this month, iron ore prices will continue to face pressure from easing fundamentals. On the supply side, Australian miners typically ramp up their shipments in December to meet annual or half-year targets, so global ore shipments are expected to increase significantly this month, potentially creating a new monthly record, the report predicts.

On the demand side, the seasonal slowdown in steel consumption during winter and shrinking steel margins will prompt domestic steel producers to further cut their production, weighing on iron ore demand.

Daily hot metal production among the 247 Chinese blast-furnace steelmakers under Mysteel’s tracking averaged 2.36 million t/d during November 21-27, down by 16,800 t/d or 0.7% on month. However, by the end of this month daily output is seen falling below 2.3 million t/d, Mysteel forecasts.

That said, iron ore prices may find support from global and domestic economic news, the report points out. Growing optimism that the US Federal Reserve will cut interest rates soon could bolster market sentiment and lift commodity prices. In addition, China’s Central Economic Work Conference, scheduled to convene in mid-December, may also underpin market confidence by announcing new stimulus programs and work targets.

Further support may come from pre-Chinese New Year holiday restocking, the report adds. Chinese steelmakers usually begin replenishing seaborne iron ore about two months ahead of Chinese New Year, and with the holiday beginning on February 10 next year, mills are expected to start restocking late this month, providing some upward momentum to prices.

Overall, both upside and downside room for iron ore prices is limited in December, the report concludes. Mysteel SEADEX 62% Australian Fines index is forecast to fluctuate between $100-108/dmt this month, compared with November’s range of $100.75-106.55/dmt.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply