Mysteel Global: The demand for imported iron ore in China is expected to remain strong in April, as the recovery of steel consumption underway among end-users will encourage steelmakers to lift their hot metal output further, according to Mysteel’s latest monthly report on the commodity. But ore prices will likely come under pressure with supply outstripping demand, the report forecasts.

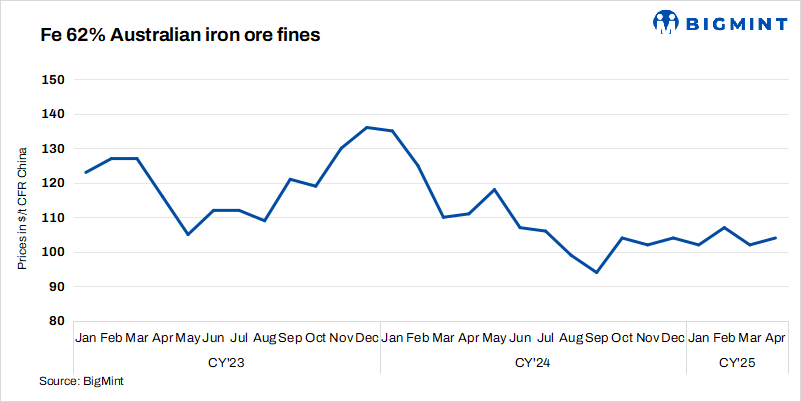

Last month, imported iron ore prices generally fluctuated within a narrow range, with Mysteel SEADEX 62% Australian Fines index settling at $102.55/dmt CFR Qingdao on March 31, recording a small dip of $0.9/dmt from end-February.

The resumption of production among domestic steel mills accelerated last month, as many blast furnaces were brought back online after maintenance. The combined daily hot metal output among the 247 mills nationwide under Mysteel’s tracking averaged 2.37 million tonnes/day during March 21-27, higher by 4.1% on month.

It was the healthier profit margins that sustained the production enthusiasm of mills when the steel demand recovery proved slower than expected, the report pointed out. Mysteel’s survey showed that over half of the 247 sampled mills were able to earn profits on steel sales throughout March.

While the demand for raw materials was strong last month, the upward momentum of ore prices was limited as supply also increased quickly after the disruptions to Western Australian ore shipments caused by adverse weather faded, the report explained.

For April, domestic steel demand is expected to continue recovering before the summer heat impacts outdoor construction activity. Indeed, over the past few weeks finished steel inventories held by Chinese trading houses have been steadily falling, reflecting active buying among end-users, as Mysteel Global has reported.

Consequently, hot metal output among integrated mills is forecast to rise further this month, but production is likely to peak quickly around the middle of the month, the report suggests. For one thing, few blast furnaces remain idled that can be reignited to add to the operating capacity, while for the other, some mills might start production cuts to align with the country’s goal of controlling crude steel output.

Although the demand for iron ore will be underpinned by the active production among steelmakers, ore prices will face downward pressure as the supply will continue to rise because of the significant rebound in iron ore shipments last month, the report said.

Mysteel’s tracking of global iron ore miners showed that their combined daily iron ore shipments averaged 4.39 million tonnes/day in March, rising by 647,000 t/d or 17.3% on month.

But given that mills will start replenishing the steelmaking material in late April to carry their production through the May Day holiday over May 1-5, iron ore prices might gather some strength late in the month, the report notes. The upside room will be small, however.

The average price of Mysteel SEADEX 62% Australian Fines index in April is seen hovering around $98/dmt CFR Qingdao, lower than the average of $102/dmt in March, the report predicts.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply