Chinese HRC (grades S235 and S275) export offers to Middle East (ME) decreased by around $5-10/t w-o-w this week. The current offers are hovering around $575-580/t CFR UAE, against $580-585/t CFR UAE a week ago, this decline is attributed to lower bids from buyers. Additionally, a deal of around 20,000 tonnes (t) was heard concluded at $565-570/t CFR UAE. Furthermore, another deal of similar quantity was heard concluded at $560-565/t CFR UAE. However, there are no competing imported offers from other origins like Japan and India.

Shanghai Futures Exchange (SHFE) HRC futures remained volatile, rising in early-May post-holidays. However, the same fell by RMB 82/t ($/t) w-o-w to RMB 3,789/t ($/t) as compared to RMB 3,871/t ($/t) a week ago. Moreover, on d-o-d basis the same declined by RMB 14/t ($/t) d-o-d on 13 May 2024.

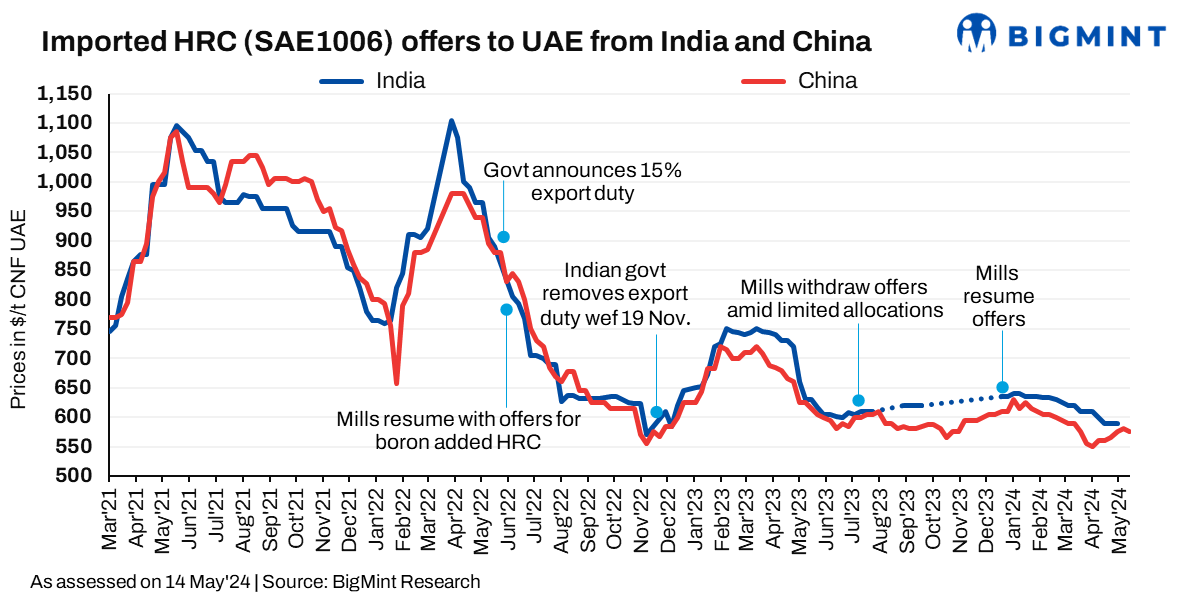

Indian mills have continued to hold HRC export offers due to limited export allocations and higher domestic realisation. The HRC export volumes from India to ME fell by 6,636 t m-o-m reaching 33,548 t in April 2024 against 40,184 t in March 2024.

The UAE steel market is experiencing steady growth, this growth is fuelled by rise in steel consumption for construction and infrastructure projects.

Outlook: While bad weather is on the horizon for the UAE, potentially impacting steel demand in the short term, construction and infrastructure projects are on the rise, suggesting an overall positive outlook for steel demand.