- Re-roller books 25,000-t HRCs from Japan

- SHFE HRC futures climb up by $2/t w-o-w

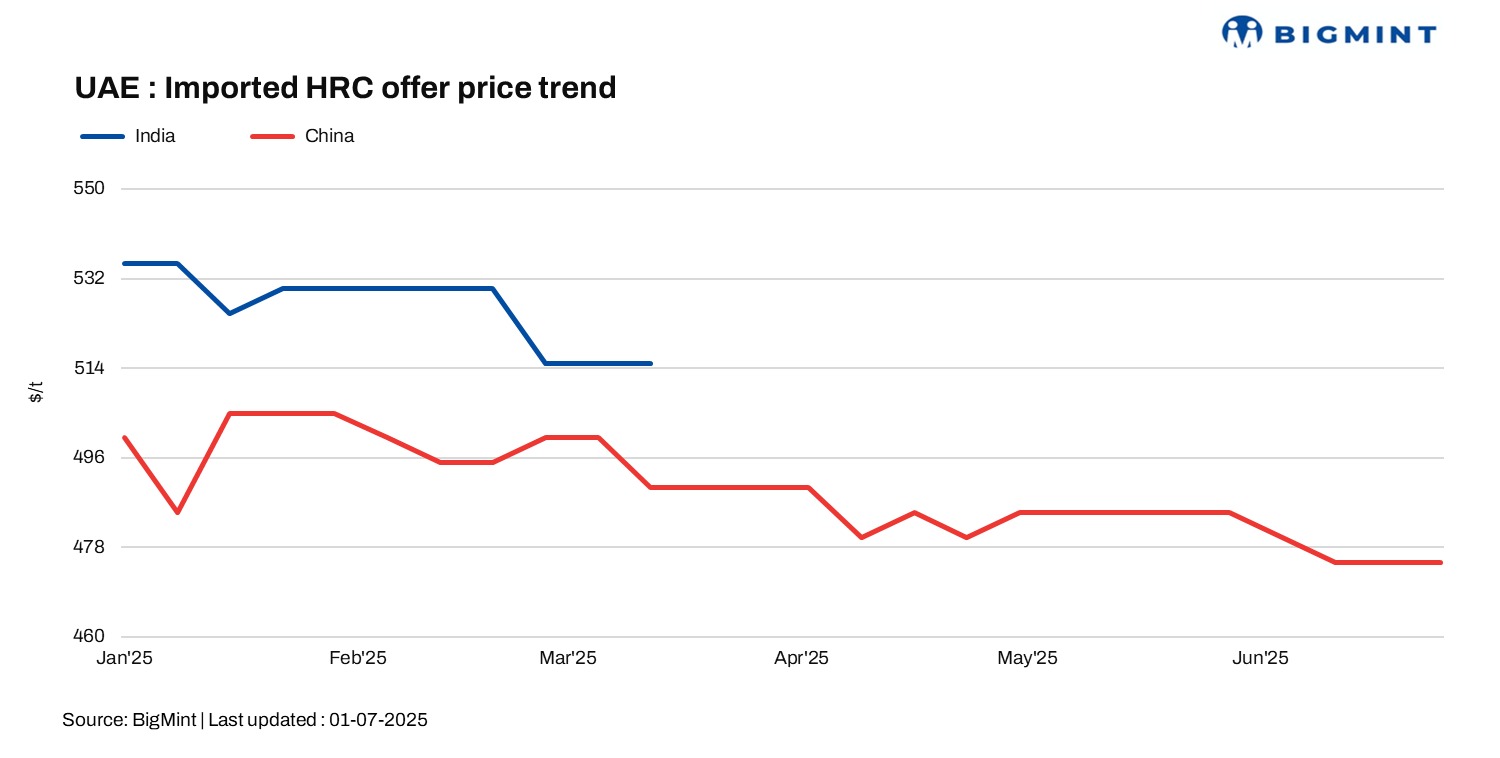

The Middle East’s imported hot-rolled coil (HRC) offers remained largely range-bound w-o-w. This stability in pricing could be attributed to buyers’ expectations of a further downtrend in HRC price tags, fuelled by competitive tendencies between exporters from China, Japan, and Russia. Notably, Indian mills are currently not extending offers to the Middle Eastern market.

Chinese HRC offers to the Middle East were steady w-o-w at $475/tonne (t) CFR UAE.

HRC futures on the Shanghai Futures Exchange (SHFE) for October 2025 increased by RMB 15/t ($2/t) w-o-w to RMB 3,121/t ($436/t) as compared to RMB 3,106/t ($434/t) a week ago. However, on a d-o-d basis, the same edged down by RMB 13/t ($2/t) from RMB 3,134/t ($438/t) a day ago.

Japanese offers were at around $490-495/t CFR UAE, range-bound w-o-w.

Despite an overall sluggish market, a notable deal for approximately 25,000 t of HRC from Japan was finalised by a re-roller at around $490-495/t CFR UAE for August-September shipments. Japan’s steel exports to the UAE in May stood at 46,916 t, down by 13,992 t as compared to 60,908 t in April. On a y-o-y basis, Japanese HRC exports to ME edged up by 1,505 t from 45,411 t a year ago.

Meanwhile, Russian offers were at $450-460/t CFR.

Indian mills are currently not actively offering flat steel to the UAE, primarily due to more competitive offers available from other regions. This led to a significant drop in Indian steel exports to the UAE in May, falling sharply by 28,721 t m-o-m to 4,714 t from 33,435 t in the previous month. This also represents a decline of 19,740 t compared to 24,454 t last year.

Outlook

The Middle East’s imported HRC market is expected to remain under downward price pressure in the near term. This outlook is driven by buyers’ firm expectation of further price declines, largely fuelled by consistently competitive offers from China, Japan, and Russia.

Leave a Reply