- Premium coking coal supply remains structurally tight

- Indian buyers cautious but near-term demand intact

The global metallurgical raw materials complex entered February on a firm footing, with prices holding steady across most benchmarks despite uneven steel demand signals. Supply discipline from miners, tight availability of premium-quality material, and cautious restocking by steelmakers have prevented any meaningful downside, while upside momentum remains capped by resistance from end-users to elevated prices.

Metallurgical coal

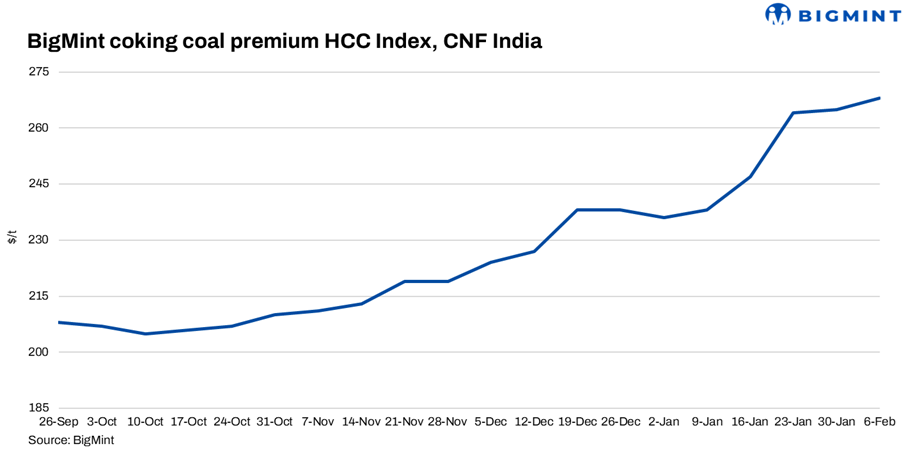

Pacific Basin: The Pacific market continues to be led by premium hard coking coal, where availability remains constrained. Australian premium low-vol material remains well supported, with miners reluctant to discount and spot liquidity thin. Market feedback increasingly suggests that semi-hard or secondary brands are being offered instead of premium products, reinforcing the perception that prompt PHCC supply is tight.

Support has also come from China’s futures market, where strength in coking coal contracts has helped stabilise forward sentiment. While spot buying remains selective, futures-led confidence is anchoring prices, particularly for Q2 delivery.

India: Indian steelmakers remain cautious but not disengaged. Large integrated mills are largely covered, while smaller and mid-sized buyers are expected to re-enter selectively once pricing clarity improves. High absolute prices continue to deter aggressive restocking, but inventories are not excessive, limiting downside risk. BigMint’s premium hard coking coal (PHCC) index was assessed at $268/tonne (t) CNF Paradip, India, on 6 February, up by $3/t against the previous assessment on 30 January last.

Improving margins in downstream segments such as sponge iron have helped stabilise sentiment across the broader coal complex, indirectly supporting expectations for metallurgical coal demand later in the quarter.

Metallurgical coke

Indonesian sellers continue to hold firm for forward-loading cargoes, reflecting comfortable order books and limited pressure to clear tonnage. Indian blast furnace (BF) and foundry grade metallurgical coke prices registered a w-o-w increase, as assessed on 4 February. The upward price movement was primarily driven by escalating raw material costs and the hike in imported met coke offers.

In eastern India, BF-grade metallurgical coke (25-90 mm) prices increased by INR 300/t w-o-w to INR 34,300/t ex-Jajpur. Similarly, prices in western India witnessed stability. BF-grade coke prices stood at INR 30,300/t ex-Gandhidham.

In India, coke buying remains highly price-sensitive. Buyers are covered in the near term and unwilling to absorb higher costs unless steel margins improve meaningfully. In China, production discipline and environmental controls are limiting export pressure, preventing downside despite muted demand.

PCI

The PCI market remains comparatively stable, anchored by China’s domestic pricing. Mills continue to monitor PCI versus coking coal economics closely, but no large-scale substitution shift has emerged. In India, PCI demand remains muted, reflecting conservative blast furnace utilisation and cautious inventory management, while suppliers show little urgency to discount.

Outlook

The metallurgical coal, coke and PCI markets are stable rather than in a downturn. Supply discipline is the dominant force, keeping prices supported despite uneven steel demand. Premium products remain structurally firmer, while secondary grades are more exposed to negotiation. Price movement will depend on steel demand recovery in India and China, and on whether miners maintain current supply restraint into Q2.

Leave a Reply