- Consumption continues to outpace production

- Import dependence to persist amid supply gap

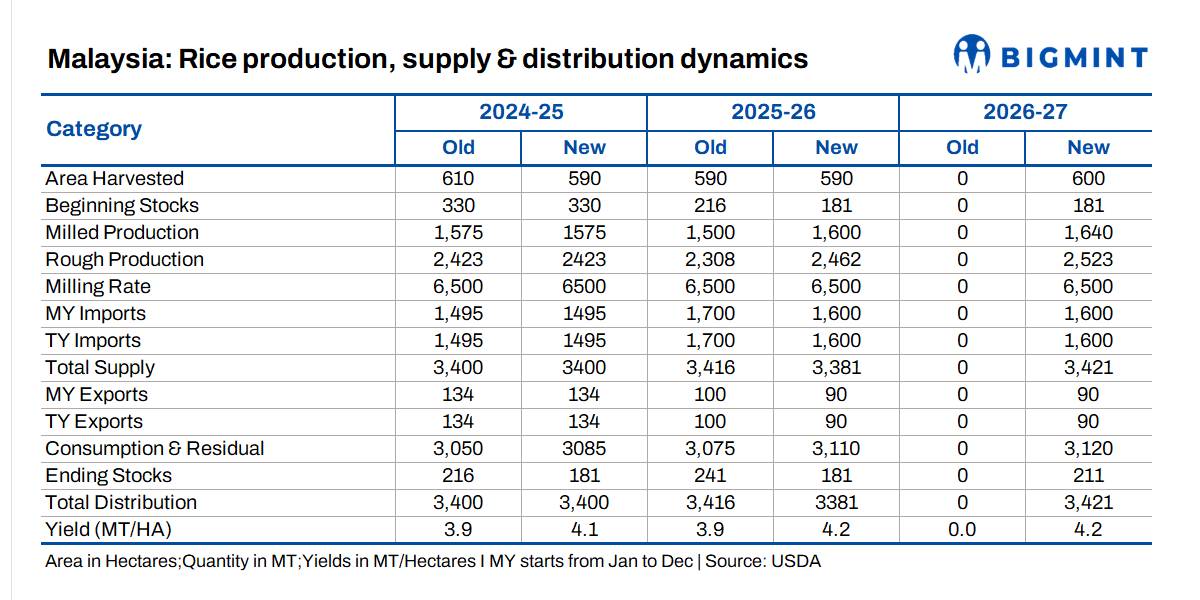

Malaysia’s rice production in MY 2026-27 is forecast at 1.64 million tonnes (mnt), up from an estimated 1.60 mnt in MY 2025-26, reflecting marginal growth driven primarily by yield improvements rather than expansion in harvested area. While yields are expected to improve modestly, structural challenges such as limited land availability, irrigation inefficiencies, and labour constraints continue to restrict significant output growth.

Consumption continues to outpace supply

Malaysia’s rice consumption is forecast at 3.12 mnt in MY 2026-27, significantly higher than domestic production of 1.64 mnt, creating a structural supply gap of nearly 1.5 mnt. This gap continues to anchor strong import dependence. Rice remains a staple in domestic diets, supported by government interventions such as price controls and subsidies.

Imports remain critical; India a key supplier

To bridge the supply gap, rice imports are forecast at 1.60 mnt in MY 2026-27, underscoring Malaysia’s continued reliance on global markets. India remains a key supplier, with import volumes showing notable growth in recent years. Imports from India rose from 0.37 mnt in CY’23 to 0.42 mnt in CY’24, and further to 0.47 mnt in CY’25 (calendar year basis). In January-February 2026, imports stood at 0.05 mnt.

Exports remain limited

Rice exports are forecast at 0.09 mnt in MY 2026-27, indicating that Malaysia remains a net importer with minimal participation in global export markets. Export activity is largely limited to small-scale or re-export volumes.

Stocks provide limited buffer

Ending stocks are forecast at 0.21 mnt in MY 2026-27, offering a modest buffer against supply disruptions. However, given the scale of the consumption gap, stock levels remain relatively tight, further underscoring the importance of steady import flows.

Outlook

Malaysia’s rice market will remain import-driven, with a supply gap of nearly 1.5 mnt keeping imports firm at around 1.6 mnt. Limited scope for production growth due to structural constraints will continue to cap domestic output. In the near term, steady demand will support consistent import flows, while in the medium term, reliance on key suppliers will keep the market sensitive to global price movements and supply dynamics.

Leave a Reply