- Freight-driven cost resets are reshaping competitiveness

- China’s import mix is quietly re-diversifying

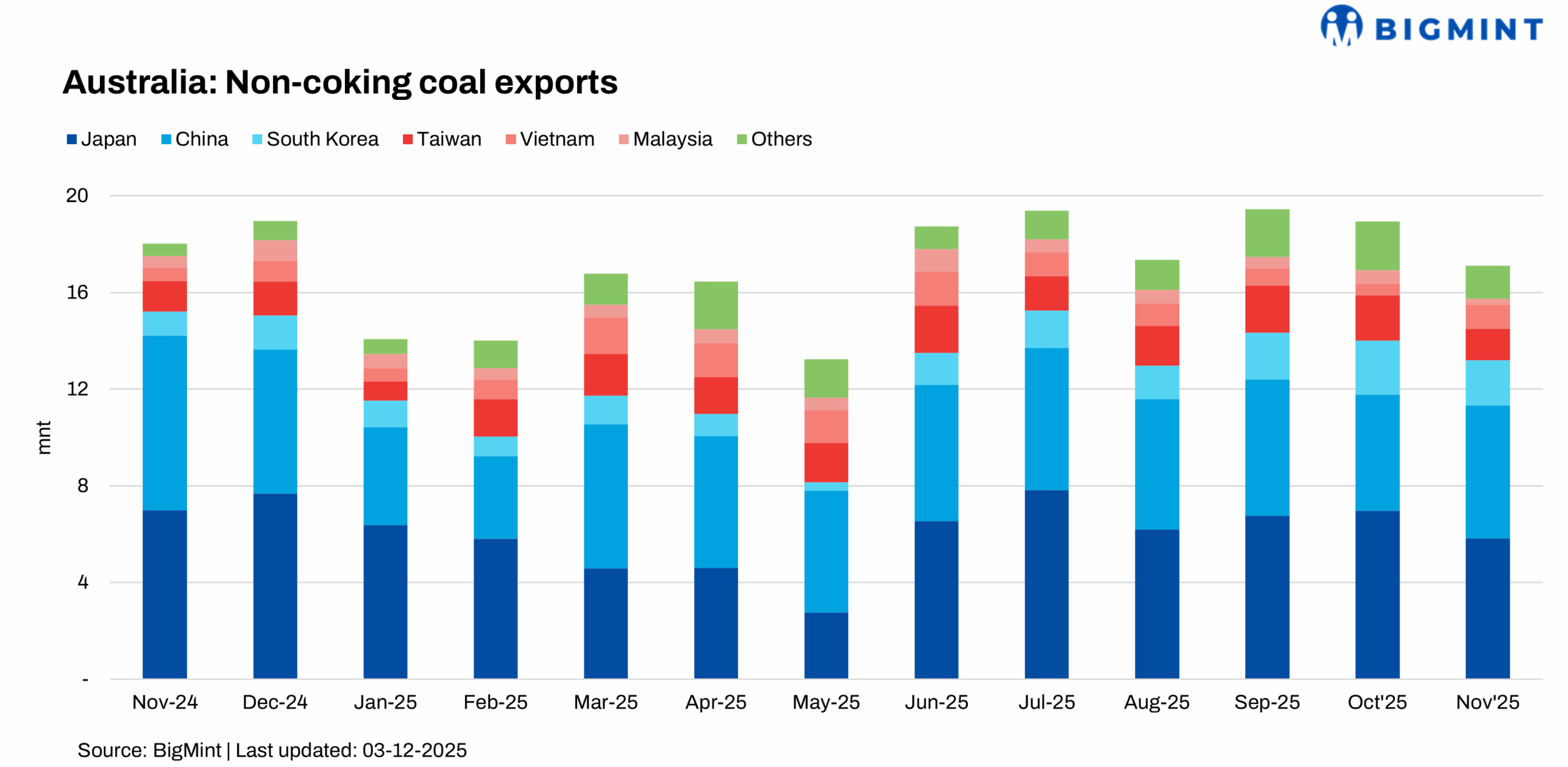

Australia’s thermal coal industry has historically faced sustained competitive pressure in the Chinese market from lower-cost Russian and Indonesian supplies, particularly for mid-CV grades. However, a recent and unexpected shift has brought Australian coal back into contention, not due to any meaningful improvement in underlying demand, but rather owing to a sharp realignment in cost dynamics.

A concurrent decline in FOB Newcastle 5,500 kcal/kg prices and a steep fall in global dry bulk freight rates has significantly reduced delivered costs into China, restoring the relative competitiveness of Australian cargoes after several months on the sidelines. The Baltic dry bulk index fell 3.8% to 2121 on 17 December.

Together, these dynamics have shifted the delivered-cost landscape so sharply that Australian coal regained competitiveness in China for the first time in months.

How the price correction sparked a comeback

NEWC 5500 plunged by several dollars, widening Australia’s delivered discount into China from $3.20/t to $7.60/t in a single week, while Russian coal, still the cheapest point of origin for non-coking coal, saw its delivered discount shrink from $30.95/t (mid-Nov) to $20.50/t, as freight fell and Chinese domestic prices slumped.

Indonesian 4200 GAR remained the most competitive for India, but into China its delivered advantage narrowed sharply, bringing coal from Australia into focus.

Freight: The hidden catalyst

Shipping rates have softened across all major coal trade routes, reinforcing the broader decline in delivered costs. Panamax freight on the Kalimantan-India West Coast route has fallen to around $9/mt, while Australia-China Panamax rates have eased by approximately $1/mt. At the larger end, Capesize freight has come under pronounced pressure, with Q1 forward contracts weakening sharply, reflecting subdued cargo demand and ample vessel availability.

These reductions amplified the price drop in FOB Newcastle 5500 , making Australian coal cost-competitive despite China’s tepid buying appetite. As of BigMint’s latest assessment on 17 December, FOB Newcastle 5500 coal prices stood at $ 76/t.

Why this matters strategically

Australia’s re-emergence in the Chinese thermal coal market carries implications that extend well beyond headline pricing. The shift helps diversify China’s import portfolio, easing its recent over-reliance on Russian supplies, while simultaneously providing Australian producers with much-needed export volumes during a period of subdued global demand.

At a regional level, the change reshapes arbitrage dynamics into India and Northeast Asia, as Australian cargoes regain relevance in delivered-cost comparisons. More broadly, it underscores how rapidly trade competitiveness can swing in a market where freight movements play a decisive role in shaping trade flows. In a market dominated by negative sentiment, Australia has found a surprising and entirely price-driven path back into China’s procurement radar.

Leave a Reply