- Oversupply concerns weigh on zinc prices

- SHFE warehouse stocks rise by 8.8% w-o-w

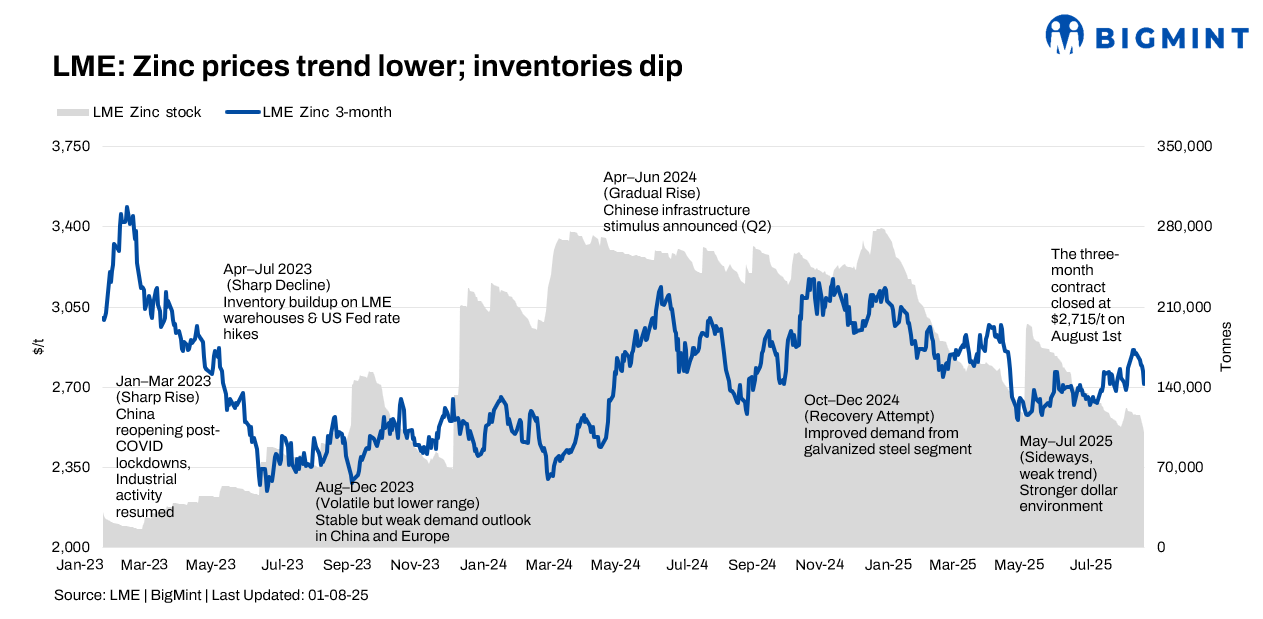

London Metal Exchange (LME) zinc prices experienced downward pressure throughout the week despite falling inventories. The downtrend was primarily influenced by persistent oversupply concerns and global macroeconomic uncertainties. While there were brief periods of stabilisation, overall market sentiment remained bearish.

LME prices trend lower, inventories dip

LME zinc cash-settlement prices trended downward. On 1 August, the cash-settlement price stood at $2,732.85/tonne (t), down 1.20% from the previous day and lower by 4% from $2,844.50/t on 25 July. The three-month contract also closed lower than the $2,847.00/t recorded on 25 July.

This decline reflects persistent bearish sentiment, fuelled by oversupply concerns and weak market fundamentals. Overall, zinc prices had been in decline for much of the first half of 2025, as primary supply increased and demand from the construction sector slumped.

The market was also influenced by a rebound in the US core personal consumption expenditure (PCE) inflation rate in June and weakening expectations for US Federal Reserve interest rate cuts, which boosted the US dollar and put downward pressure on LME zinc prices.

LME zinc inventories saw a decrease during the week. On 1 August, these inventories fell to 100,825 t from 115,775 t on 25 July, representing a 13% decline.

MCX zinc declines (28 July-1 August)

MCX zinc prices also experienced a decline w-o-w. On 1 August, zinc futures stood at INR 263.95/kg, down 0.6% from the previous day and lower than INR 269.05/kg on 25 July. This reflects a bearish trend in the Indian market, driven by factors such as reduced speculator exposure and slackened demand from consuming industries.

Analysts noted that the trimming of positions by participants, due to slackened demand from consuming industries in the physical market, mainly weighed on zinc prices.

The price also faced resistance around the INR 276/kg level, suggesting a cap on short-term gains without a strong breakout

SHFE zinc dips

Zinc prices remained under pressure due to US trade tensions and weak Chinese manufacturing, despite early July support from a softer US dollar. SHFE September zinc contracts stood at RMB 22,829/t (ZN2508) and RMB 22,833/t (ZN2509) on 1 August, down 0.52% and 0.49% w-o-w. SHFE zinc warehouse stocks rose 8.8% to 139,810 t, keeping the SHFE/LME ratio near 8.1 and imports unattractive.

Zinc producers — key updates

- Hindustan Zinc awarded an EPC contract to L&T for its Debari Smelter upgrade, following a 47% y-o-y profit surge in Q4FY’25 and maintaining a 77% market share in India.

- Vedanta Limited posted an 11.7% y-o-y drop in Q1FY’26 net profit, facing scrutiny over governance at Hindustan Zinc.

- Nyrstar cut Hobart’s smelter output by 25%, seeking approximately $45 million in government aid.

- Korea Zinc plans a non-ferrous smelter in the US.

Outlook

Zinc outlook remains cautious as weak Chinese demand and rising inventories offset earlier price gains, while global macroeconomic uncertainty continues to influence market direction and sentiment.

Leave a Reply